by Benjamin Streed, Fixed Income, Raymond James

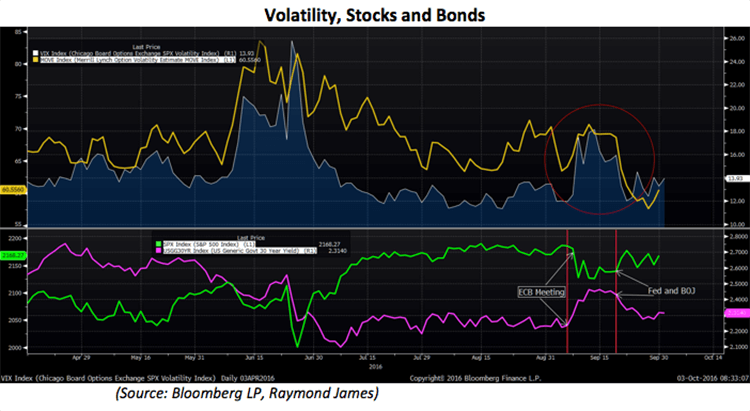

October begins with a volatile, but ultimately unchanged, month of September in the rearview mirror while many look ahead to the uncertainty surrounding the US presidential elections next month. Many had expected volatility to pick up at the end of the summertime, having seen both equity and bond market volatility hit multi-year lows beginning in June and culminating in late August. Although many expected an increase in volatility, September was choppier than nearly anyone had expected thanks in large part to global central banks overseas including both the European Central Bank (ECB) and the Bank of Japan (BOJ) in addition to the US Federal Reserve (Fed). The playbook went something like this (see the chart below): the ECB met on September 8th and indicated that they would refrain from further easing, pushing yields across the world sharply higher. This led many to speculate that the BOJ and Fed would follow suit and also turn more “hawkish” (in favor of tightening monetary policy), including a possible rate hike here in the US. For the next two weeks markets would continue to be volatile, pushing equities lower (bottom chart, green line) and yields higher (purple). The volatility for bonds (top chart, yellow) followed equity volatility lower (blue) as most markets could’ve been described as “sleepy”. Shortly after the Fed confirmed it would remain on hold the markets returned to “business as usual” with lower volatility, higher equity prices and lower yields. If you ever needed convincing that the markets are heavily influenced by the central banks this was the proof.

Although the Fed was on hold, it was a very different tone this time around as the hawkish sentiment was blatantly obvious with three “nay” votes, the first time this has happened since December of 2014, with the first hiking coming in 2015. One of the sticking points for the Fed is that it wants to see inflation closer to 2.00% before a second hike is justified. Interestingly, the committee doesn’t see that level being reached until 2018 and have also decreased their GDP growth estimate to 1.80% from 2.00%. For reference, the post-crisis GDP estimate has steadily declined from 2.65% to the current 1.80%. Fed Chair Yellen noted that, “we are generally pleased with how the US economy is doing”, despite their estimates consistently being revised downward and/or stretched further out. For now, it appears the “hawkish hold” is one that continues to encourage data dependency and will be patient in both the timing and frequency of any future rate hikes. Of course, with the election slated for November, many are expecting any move from the Fed to be in December at the earliest with an approximately 59% chance of a rate hike according to Bloomberg estimates. September came, September went and seemingly not a whole lot changed overall.

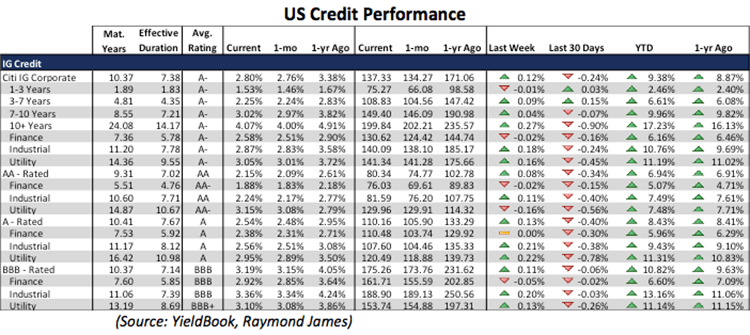

Meanwhile, although the Treasury market continues to garner strong focus from both investment professionals and the media, it would be apt to remind readers how the credit markets are faring. US domestic corporate credit continues its strong performance with impressive year-to-date gains, more than making up for September’s back-and-forth. For those interested in seeing more details broken down by industry, credit rating and maturity you can see our Weekly Index Monitor here. Spreads are roughly in line month over month and remain significantly lower than their levels from a year ago. Much of the performance in bonds is attributed to the duration effect (longer-dated bonds have outperformed shorter-dated) with the remainder due to the decline in overall credit spreads.

Copyright © Raymond James