Will Mortgage Bonds Be the Next Disaster—Again?

by Gershon Distenfeld, Michael S. Canter, AllianceBernstein

September 27, 2016

For some investors, any mention of US mortgages takes them back to the dark days of 2008. But today’s mortgage bonds aren’t the devils some market participants make them out to be.

We understand why the topic provokes anxiety. In the 2000s, rapidly rising home prices prompted lenders to make risky loans, often without verifying a borrower’s income or requiring a down payment. Many of those borrowers defaulted when US housing prices started to fall.

Because the loans were bundled into residential mortgage-backed securities (RMBS), the poison was able to spread through the global financial system. The result: what might have been a simple US housing correction became a global crisis.

Today’s Nontoxic Loans

By now, the story is well-known, thanks to countless books and the critically acclaimed film The Big Short. But just before that film’s credits start to roll, an on-screen warning darkly implies that nothing much has changed. This gives the impression that Wall Street is again busy stuffing toxic loans into a new breed of mortgage-backed securities, setting the stage for another crisis.

We disagree. The majority of today’s loans aren’t toxic. Tight lending standards mean only high-quality borrowers are getting loans. Several credit metrics, including average FICO scores and borrower debt-to-income and loan-to-value ratios, are at or near their best levels since 2006.

In other words, if there were ever a time to take on mortgage credit risk, it’s now. That’s one reason why we think new credit risk–transfer securities (CRTs) from government-sponsored housing agencies Freddie Mac and Fannie Mae offer an attractive opportunity.

Beyond having mortgages as underlying collateral, CRTs have very little in common with traditional agency debt or the precrisis non-agency RMBS that banks issued. That’s partly because these new securities have less risk layering than did their precrisis counterparts.

There is less risk because CRTs contain fewer loans to borrowers with multiple red flags. For instance, nearly 11% of the loans in the securities Freddie issued in 2006 went to borrowers with low FICO scores (weak credit) and high debt-to-income ratios. For the 2016 CRTs, only 0.7% did.

Sharing Risk, Reaping Rewards

CRTs are different from traditional agency debt in another important way: they have no government guarantee. Before the crisis, investors assumed interest-rate and prepayment (unscheduled early return of principal) risk, but Fannie and Freddie guaranteed coupon and principal payment, even when the underlying loans would default.

With CRTs—also known as credit risk–sharing transactions—private investors absorb a share of the losses if a large number of loans default. Freddie and Fannie began using these securities to off-load some of their credit risk and to take US taxpayers off the hook for bailing out private investors.

To compensate investors for assuming more credit risk, CRTs tend to yield more than do traditional agency RMBS. In some cases, yields are in line with the ones high-yield corporates offer.

This risk may sound scary. But it shouldn’t. In our view, the strong credit fundamentals of the underlying mortgages make the risk/reward trade-off an attractive one.

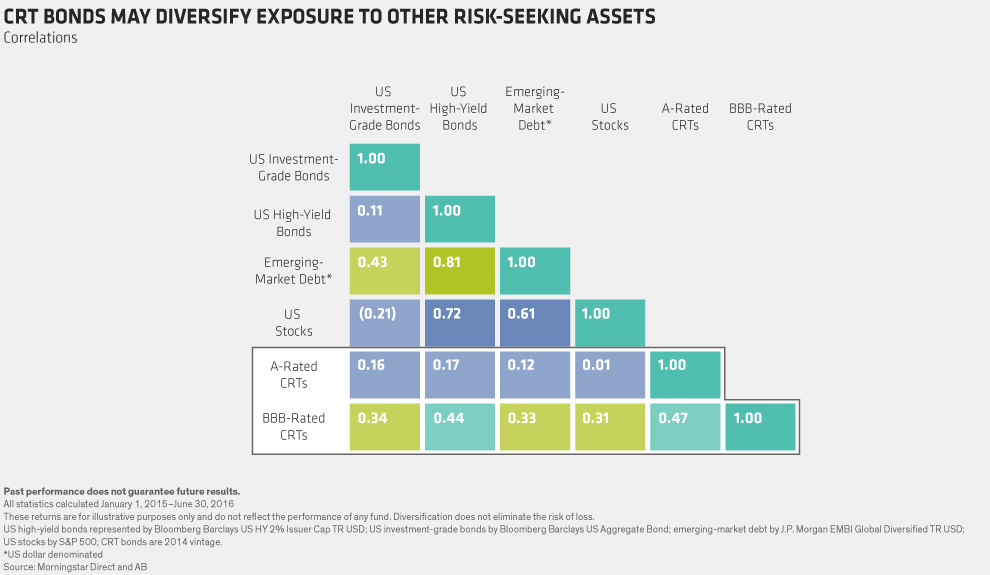

CRTs don’t have a long track record (Freddie and Fannie began issuing them in 2013). But so far, they have delivered returns in line with or better than other assets’—and they’ve done it with less volatility. What’s more, their low correlation to other parts of the bond market make them an attractive way to diversify exposure to high-yield and other risk-seeking assets (Display).

A Blueprint for the Future

Credit risk–sharing transactions may represent the future of mortgage investing in the US. If Freddie and Fannie keep issuing at their current pace, outstanding CRTs could hit $100 billion over the next four years, compared to $27.9 billion through June.

Non-agency RMBS, meanwhile, are losing market share. According to our calculations, outstanding debt shrunk to $550 billion through August, from $720 billion at the end of 2014.

Of course, growing pains are inevitable in new markets, and CRTs are no exception. Because many investors have yet to discover the market, liquidity is limited.

Also, performance among existing CRTs is highly correlated, though that should change as new loans and issuers come to market. We wouldn’t be surprised to see banks and private investors one day start to use this risk-sharing template.

We understand why investors are anxious about RMBS—especially those who got burned during the crisis. But the mortgage market has changed, and we think investors who don’t change their view of it may be missing a great opportunity.

The views expressed herein do not constitute research, investment advice or trade recommendations and do not necessarily represent the views of all AB portfolio-management teams.

Copyright © AllianceBernstein