Gold Loves Real Low Interest Rates

by Erik Swarts, Market Anthropology

- The prospects for precious metals remain attractive, as we believe the initial move lower in the dollar this year sets up a much larger breakdown headed into Q4 and 2017.

- Historically, the dollar still appears significantly stretched, which trended to a performance extreme last year as the Fed moved off ZIRP and as rate hike projections peaked.

- For the US dollar index, a break below 93 would begin the next phase of a large retracement move, which should coincide with lower real yields and higher precious metals prices.

For those patient and willing (there weren’t many), gold investors have done quite well this year, despite consensus expectations at the end of 2015 that a round trip drop beneath $1000 an ounce was inevitable.

- Prepare for gold prices to plunge...as low as $350 - 7/30/2015 CNNMoney

- Gold slump invokes predictions of doom - 7/31/2015 WSJ

- Gold falls to a 6-year low, but could fall another 25% - 11/27/2015 The Motley Fool

- No reason to hold gold in 2016; Prices to drop below $1000 - 12/03/2015 Kitco

- Gold to breach $1000 as Fed lifts rates in '16, SocGen says - 12/14/2015 Bloomberg

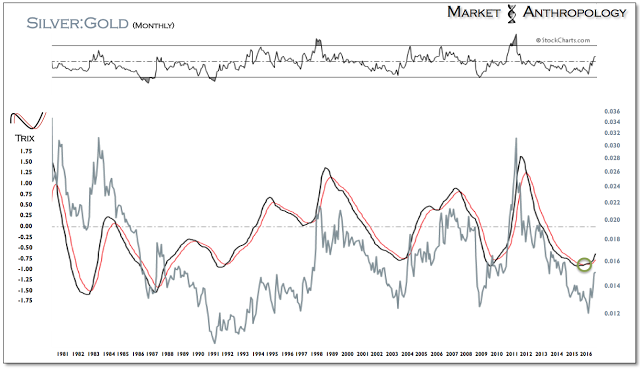

Yet even with a gain of nearly 30% this year, we suspect the current rally in gold will eventually break its cycle high (more than 40% away) of $1924 an ounce, achieved in September 2011. For silver bulls, the gains have been even more exceptional, tacking on more than 49% from last year’s close. With a cycle high of nearly $50 an ounce in the spring of 2011, the prospects for silver are proportionally much larger – albeit with greater volatility and risks.

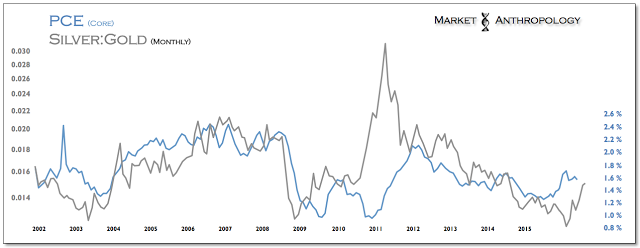

Generally speaking, the precious metals sector has performed as we had hoped this year, with gold leading the initial move in Q1 and with silver confirming the trend reversal and taking the performance pole position over gold in Q2. This bullish dynamic was presaged at the end of last year (see Here) by the rare positive momentum cross in the long-term silver:gold ratio, that strengthens when risk appetites build and broaden within the sector and that also typically leads a rising inflation trend.

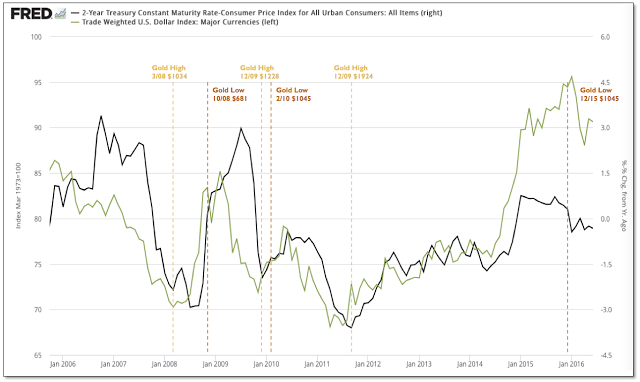

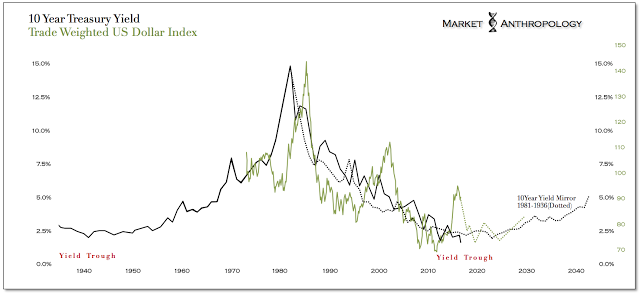

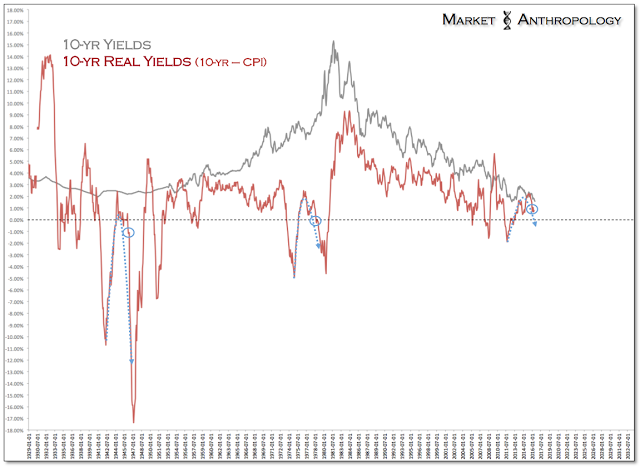

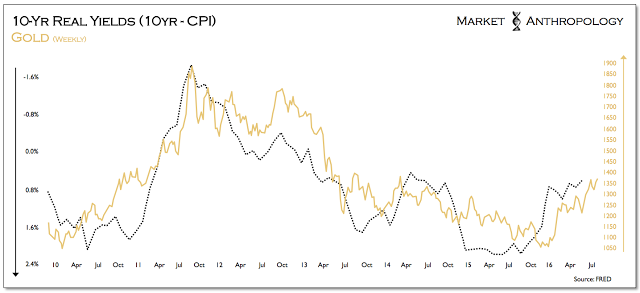

The bottom line is despite healthy gains in precious metals this year, we believe significant returns lie ahead as a weaker US dollar and declining real yields target their respective lows from 2011. Over the past decade, the dollar and US real yields have trended closely together, as the dollar strongly influences inflation and as the reach of nominal yields has largely remained under pressure.

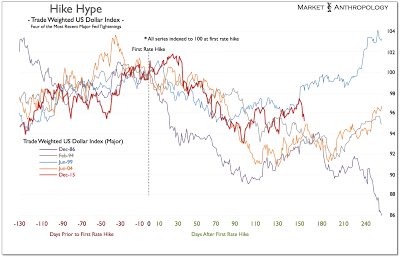

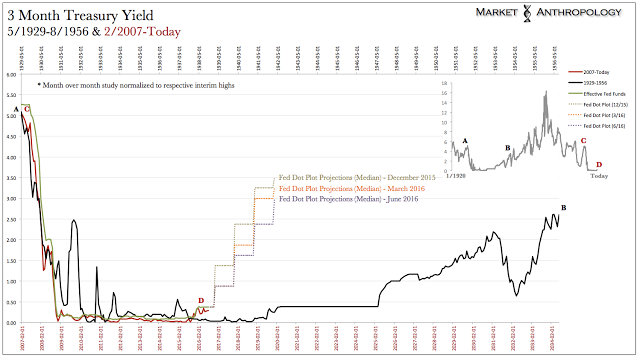

As we were looking for coming into the year, a buy the rumor/sell the news reaction in the dollar manifested after the Fed moved modestly off ZIRP – and as expectations of further rate hikes peaked and have gradually drifted lower. And while the Fed’s dot-plots have consistently trended down over the course of this year, they still have a ways to go in aligning expectations with historic precedence within the long-term yield cycle (see here); a multi-generational force – that as the Fed and participants have learned, is influenced less by policy and perhaps more by proportion.

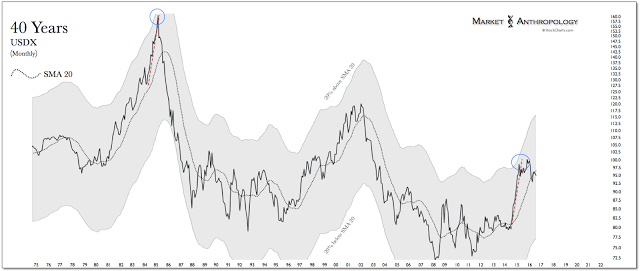

From our perspective, the prolonged nature of the Fed’s expectation phase in the face of multiple large easing initiatives around the world, allowed participants an abnormally large and fertile window to build positions and faulty assumptions in the dollar – regardless that the Fed would likely never achieve the same reach as they had in more recent tightenings and that were postured to the market in the Fed's dot-plot projections. The net effect was a high achieved in the dollar last year – arguably as stretched as the performance extreme in 1985, that we suspect will be further retraced as policy expectations continue to diverge from more contemporary tightenings and as markets and economies make their way across the transitional divide to the next secular growth cycle; a condition that eventually will be capable of carrying and sustaining the weight of a stronger US dollar and higher nominal and real yields. Until the growth cues of stabilizing and strengthening nominal yields materialize for a considerable period, the notion of a more secular continuation of a stronger US dollar is as irrational as the dot-plot projections have been towards rate expectations.

Currently, the lower rail support of the broad top carved over the past two years in the US dollar index sits just ~ 2 percent lower around 93. From our point of view, it’s more likely that the retracement rally that began in May has exhausted and that the index will break down below this key support in the coming weeks – ushering in the next phase of the move and supporting assets like precious metals and commodities that benefit from a weaker dollar.

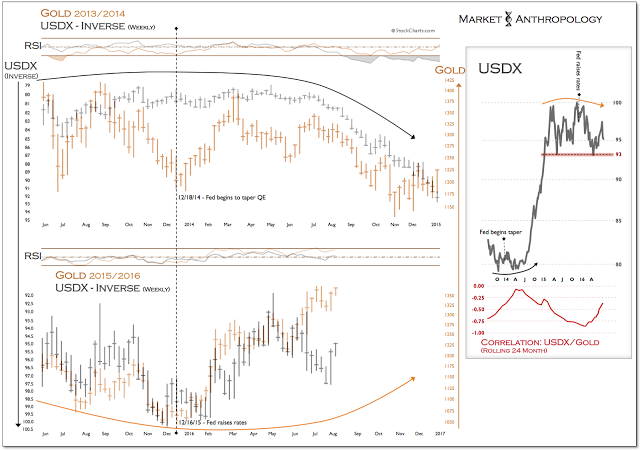

As we noted earlier in the year (see here, here, here), gold traded out of its post rate hike low, akin to the taper low in December 2014. And unlike gold’s Q1 2014 rally that coincided as the US dollar was basing, but failed in Q2 as the dollar broke out – gold moved out of the low in Q1 as the dollar exhausted from its relative performance extreme and hasn’t looked back as the dollar now flirts with a potential breakdown from its range over the past two years.

Considering that gold already trades close to $1400 an ounce while the dollar remains historically stretched, the prospects for precious metals continue to appear attractive to us as the markets catalytic converter for lower real yields has much further room to fall. Moreover, from a historic cyclical perspective, the broad top potential in the dollar now aligns structurally with the explosive and final retracement declines in real yields around 1978 and 1946, respectively. Should history repeat, we would expect new highs for both gold and silver as real yields plum the cycle low.

Copyright © Market Anthropology