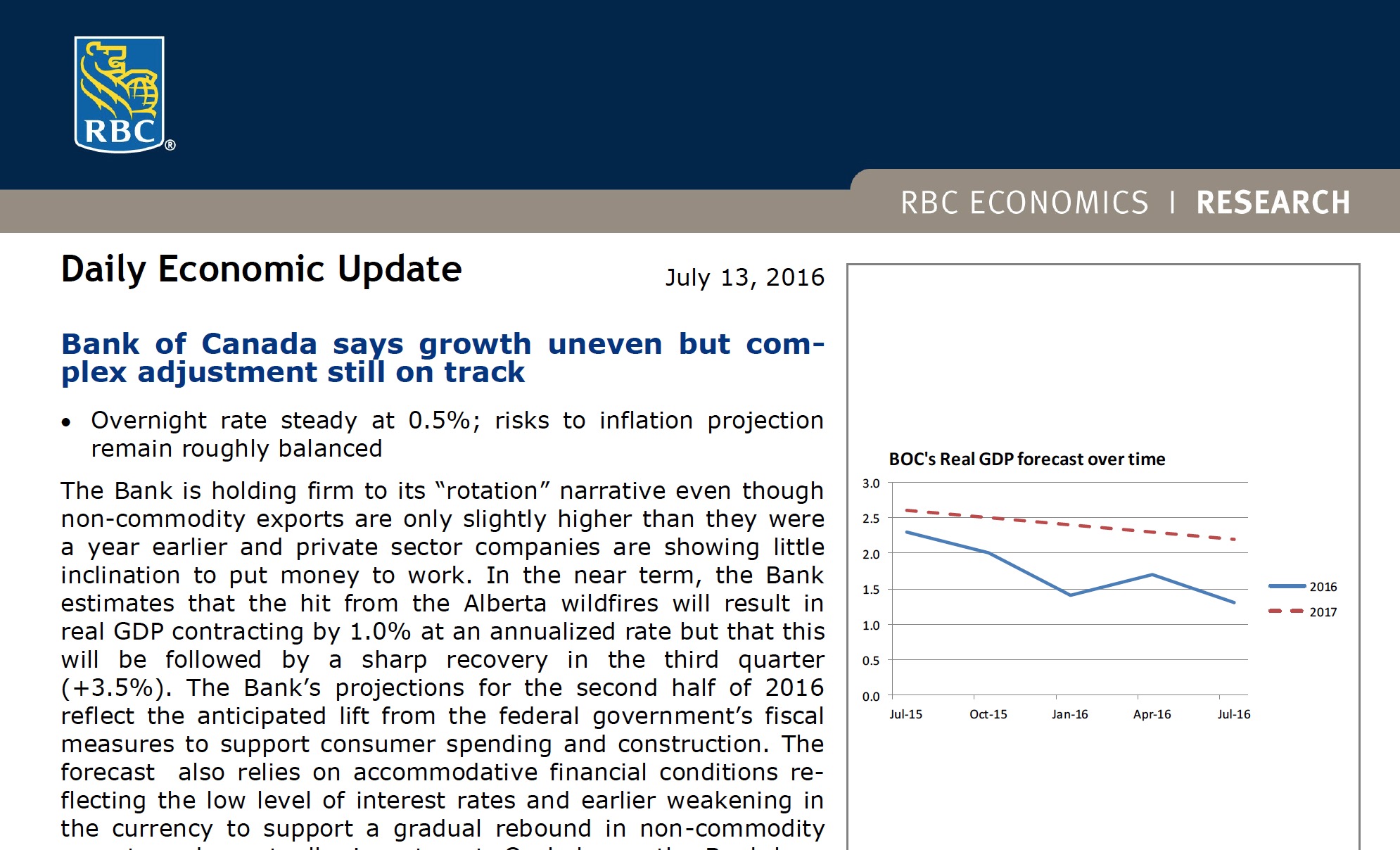

5 Common IRA Misconceptions

by Commonwealth Financial Network

Although some IRA planning and investment strategies appear simple, they can become expensive and time consuming if implementation errors are made. Your clients could pay unexpected taxes or penalties, their IRAs could lose tax-exempt status, or their beneficiaries could experience difficulties when inheriting IRA funds. To help your clients avoid these issues, here are five common IRA misconceptions to keep in mind.

Although some IRA planning and investment strategies appear simple, they can become expensive and time consuming if implementation errors are made. Your clients could pay unexpected taxes or penalties, their IRAs could lose tax-exempt status, or their beneficiaries could experience difficulties when inheriting IRA funds. To help your clients avoid these issues, here are five common IRA misconceptions to keep in mind.

It’s true that naming a beneficiary is among the easiest tasks when opening an IRA. But if your client fails to review beneficiary information regularly or plan ahead, it can lead to problems.

Spouse named as the IRA’s primary beneficiary. This provides many options when the beneficiary inherits the funds. But when a client divorces or a spouse dies, the client must update the beneficiary information. Otherwise, if the client passes away, a former spouse could be entitled to the decedent’s assets, causing legal headaches for the intended IRA beneficiaries.

Estate named as the primary beneficiary. Generally, the intention here is to let the will or trust document decide how assets will be distributed, but it can prove costly. An estate beneficiary has no age or life expectancy, leading to fewer distribution options. For example, beneficiaries determined by the estate could be forced to deplete IRA assets within five years or take distributions over the decedent’s life expectancy because they couldn’t use their own. This would result in larger distributions and potentially higher taxes. Plus, if your client leaves assets to the estate, the probate court would include the estate in the decedent’s total assets—opening the door to creditors’ claims.

The informed choice. Help your clients understand the pros and cons of their options, and reconfirm beneficiary information in their annual reviews. In addition, whenever there is a major life event, remind clients to make any necessary changes to beneficiary designations.

Loans are not permitted from IRAs, although clients may take advantage of the 60-day rollover rule.

Under IRS regulations, clients may withdraw assets from an IRA and roll over all or a portion of that withdrawal back into the IRA within 60 days. This is allowed once during a 12-month period. Straightforward, right? In reality, the 60-day rule has caused issues for countless clients who didn’t execute the rollover properly:

- Clients complete the rollover after the deadline. The rollover into the IRA must be completed 60 calendar days after clients receive the distribution. Holidays and weekends count among the 60 days, a fact overlooked by many who consequently miss their deadline.

- Clients violate the once-per-year rule. The IRS counts the number of distributions taken within the 12-month period, not the number of contributions into the IRA. Sometimes, clients take two separate distributions and roll over both into the IRA as one payment, thinking the IRS will count this as one 60-day rollover.

- Clients break the same-property rule. When a client takes the distribution of a stock or bond, for example, he or she must roll the same asset back into the IRA. It’s not uncommon for clients to withdraw a bond, sell it, and roll over the proceeds from the sale of the bond into the IRA instead of the bond itself.

The informed choice. Clients should exhaust all external options before borrowing from an IRA. If they decide on a 60-day rollover, be sure that they understand the process, including the taxes and penalties on failed rollovers.

To contribute to a Roth IRA, a client’s modified adjusted gross income cannot exceed specific income thresholds. To work around this, advisors sometimes recommend that clients fund a Roth with a backdoor conversion. This involves making a nondeductible, post-tax contribution to a traditional IRA and immediately converting the amount to a Roth IRA because there are no income limits for this conversion. If your client has no other IRAs, this strategy is worth considering.

But what if your client has an IRA rolled over from a previous employer? Can he or she isolate the contribution to the traditional IRA and convert it to a Roth? No! When assessing Roth conversions, the IRS requires all IRA assets to be aggregated and treated as one account. This means that your client’s pre- and post-tax IRA assets will be lumped together, and only a certain percentage of the recent conversion would be tax-free.

The informed choice. Clients should review all aggregate IRA assets before considering the backdoor option. If your client is in a high tax bracket, this strategy may not be the best option.

Another commonly considered strategy is the “rollover as business start-up” (ROBS), which invests IRA assets to back a new venture.

To fund a start-up, an individual establishes a C corporation. The corporation then sets up a retirement plan, which offers employees the option to purchase company stock. The owner rolls his or her IRA or 401(k) from a previous employer into the new retirement plan and uses these assets to purchase the start-up’s stock. The business now has the capital to operate.

Although each step is generally acceptable, ROBS has been garnering increased IRS scrutiny and may potentially be viewed as a prohibited activity. Why?

- The business owner pays him- or herself a salary, even though he or she is among the disqualified persons whom the IRS says cannot benefit from ROBS in specific ways. The IRS may see the salary as a transfer of plan assets for the employer’s benefit, which is prohibited.

- The purchase of company stock is available only to the employer. With a C corporation, the option to purchase company stock must be available to all employees.

- The valuation of the employer’s IRA assets at the time of purchase is inaccurate. This could affect clients who are taking required minimum distributions (RMDs). An inaccurate valuation of the purchase could lead to taking less than the correct RMD amount.

- Promoter fees are part of the deal. Some franchisors hire promoters to reel in potential ROBS candidates, such as your client. If the promoter is a fiduciary, the payment of promoter fees from plan assets could be considered a prohibited transaction.

The informed choice. Help your clients reconsider this strategy. The violations could lead to hefty IRS taxes and penalties for your client, and it could significantly deplete your client’s retirement assets.

An IRA owner has multiple options for investing account assets, including buying mutual funds, individual stocks, and bonds. One risky investment strategy is purchasing real estate within a self-directed IRA. Although the potential to generate income from rent and capital gains on the property is attractive, numerous prohibited transactions could result. Here’s what your client should know if considering such an investment:

- The property cannot be used by disqualified people—including any fiduciary to the plan, the IRA owner, and direct family members.

- Expenses directly related to the real estate must be paid with the IRA’s assets.

- Management and maintenance of the real estate must be handled by the account’s custodian.

- IRA assets must be valued and reported to the IRS annually. Real estate investments are generally illiquid, and their value can’t readily be assessed, which could lead to inaccurate reporting to the IRS.

The informed choice. Unless your client fully understands the rules and has the wherewithal to abide by them, purchasing real estate in an IRA may be trouble. It could result in the disqualification of your client’s IRA, meaning that it could even lose tax-exempt status.

Do you find your clients hold other misconceptions regarding IRAs? Do you think the backdoor conversion is a sound financial strategy? Please share your thoughts with us below.

Commonwealth Financial Network is the nation’s largest privately held independent broker/dealer-RIA. This post originally appeared on Commonwealth Independent Advisor, the firm’s corporate blog.

Copyright © Commonwealth Financial Network