When Is a “7% Return” Not a 7% Return? Answer: Most of the Time

by Gregg S. Fisher, GersteinFisher

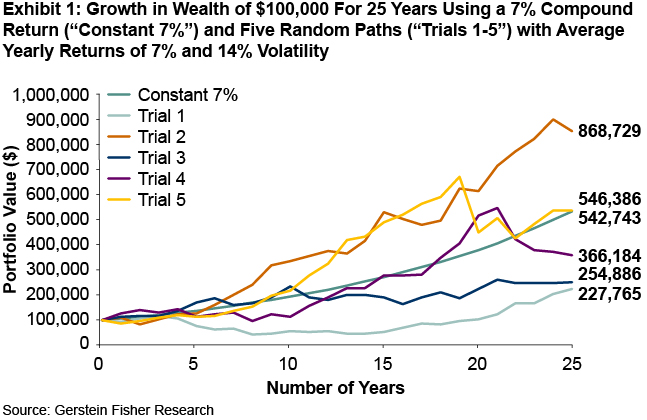

Let’s say you make a $100,000 investment in stocks that compounds at 7% per year (which is not far from what US equities have historically returned), and you hold onto that portfolio for 25 years without adding or withdrawing funds. For the sake of argument, let’s assume the return is constant, never deviating from 7% every year. As the Constant 7% line in Exhibit 1 demonstrates, at the end of a quarter-century holding period, the value of that $100,000 sum would have more than quintupled to $542,700. For most investors, this would be a very satisfying outcome.

The catch, of course, is that the assumptions we have made above are unrealistic. Aside from certain cash equivalents, no investment will grow at exactly the same rate every year, and the riskier the asset (e.g., stocks), the greater the volatility. To simulate the real world, we ran five randomized trials (all depicted in Exhibit 1), all with an “average return” of 7% a year, but now adding the additional element of 14% per year volatility, or standard deviation, which is also close to the historical experience for a stock proxy such as the S&P 500 Index. Since 14% volatility, or risk, can manifest itself in many different patterns, that “average 7% return” can take vastly different paths with entirely different outcomes. Allow me to explain what I mean.

Terminal Value of $900,000, $500,000, or $200,000?

How can the ending portfolio value after 25 years vary from a little more than $200,000 to almost $900,000? It’s because volatility can be the investor’s friend or foe, depending on when, and how many, losses and gains occur. For instance, if large losses are encountered early in an investment’s lifecycle (as in Trial 1, where the ending value is just $228,000), they pull down the amount of funds available for growth in later years. This scenario reminds me, in a slightly different context, of a retiree led to believe that there’s little risk in the sustainability of a 4% portfolio withdrawal rate in retirement. If the investment portfolio suffers significant losses in his first few years of retirement, then he’s behind the eight ball if he intends to keep pulling out 4% of initial portfolio value (adjusted for inflation) each year to meet his cost of living.

On the other hand, if large gains build up early on, there’s that much more money to compound and to absorb future losses. Trial 2 shows such a case, with a final portfolio value of $869,000 that significantly outperforms the 7% compound return. In the three other trials, two outcomes significantly underperformed the 7% compound return (Trials 3 and 4), and one (Trial 5), despite some wicked cycles, ended with almost identical wealth. The point is that the total amount of an investor’s gains and losses can vary widely since that 14% volatility, which can dramatically affect the compounding rate, can move returns either up or down (remember, in theory volatility can work in an investor’s favor every year, just as it can also work against you). Thus, a “7% average annual return” doesn’t mean much when it comes to measuring actual long-term investment returns. Harry Markowitz, a Nobel Prize winner who’s considered the father of modern portfolio theory, suggested a rule-of-thumb method to evaluate the relationship between average performance and compound return: compound returns equal the average return minus half of the variance, and that increasing the variance of returns without increasing the average return will hurt investment performance.

How Much Risk Can You Tolerate?

Let’s shift gears now and apply the implications of the math that I’ve just described to real-life investment portfolios. I have worked with investors now for nearly a quarter of a century. From that vantage point, I can say that there are some investors out there who would be comfortable with a portfolio comprised entirely of high-risk assets, hoping for that $900,000 outcome described in Trial 2. But I can also state that such intrepid investors are relatively few. For the great majority of our clients at Gerstein Fisher, fear of a dismal outcome overwhelms the hope for a spectacular one. Most would be content with a smooth ride that achieves the constant 7% result, rather than reaching for the $900,000 outcome fraught with risk. We understand and respect this mindset, which is why we make risk mitigation front and center for most of the portfolios that we manage.

Probably the most important such strategy—a classic—is diversification. Since many different asset classes tend to move up and down at different times, holding a collection of them tends to smooth the ride for a portfolio (i.e., reduces volatility). That’s why for most investors it’s an advantage to own both stocks and bonds, both US and international stocks, both bargain-priced “value” stocks and high-flying “growth” stocks, as well as some alternative asset classes such as REITs (we prefer both domestic and foreign ones), and perhaps some gold and commodity futures. The market movements in 2016 are a case in point. For example, year-to-date through May 2, while both domestic and international large growth stocks were down nearly 1%, value stocks and bonds were up, and global REITs and gold jumped 8% and 21%, respectively.

Of course, there’s a limit to how far you should take diversification, since if you owned every investable asset on earth, the returns would probably cancel one another out and you’d be left with zero. But few investors have to worry about excessive diversification; in our experience, most are not diversified enough.

How much diversification you should strive for, and with what assets, very much depends on your individual financial goals (both long- and short-term), time horizon, and ability to live through trying investment times without being tempted to bail out of the markets. If you work with an investment advisor such as Gerstein Fisher, we can help you construct such an individually tailored, diversified portfolio, and coach you through the inevitable market cycles.

Conclusion

Long-term portfolios with the same average annual return can produce astonishingly different final wealth sums due to volatility and differing patterns of gains and losses along the way. A well-diversified global portfolio can help to reduce volatility levels and make for a smoother ride for investors.

Copyright © GersteinFisher