by Tiho Brkan, Short Side of Long

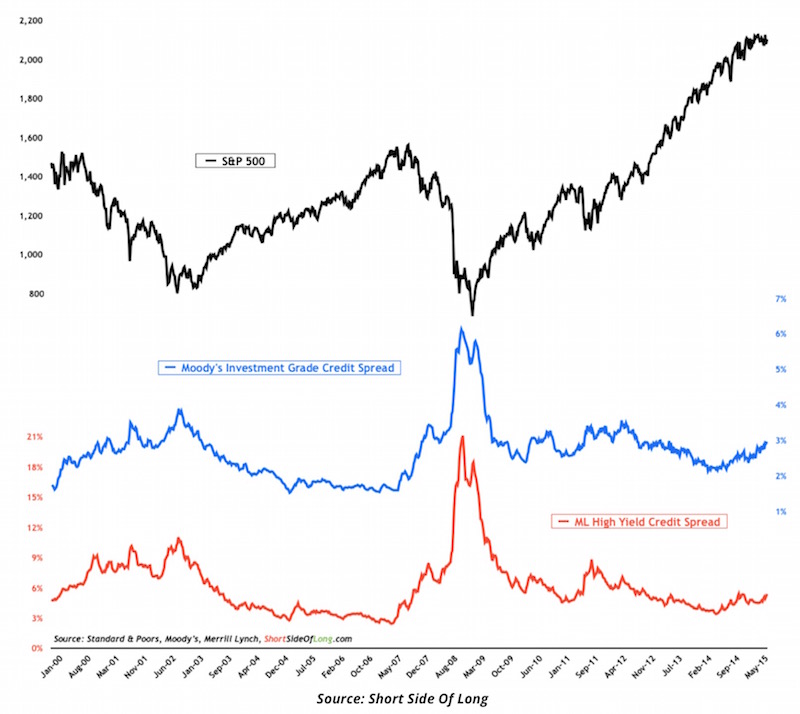

Chart Of The Day: High Yield and Investment Grade credit spreads keep rising

Source: Short Side Of Long

Looking at the S&P 500 (NYSE: SPY), one would come to a conclusion that the bull market is intact and global growth solid. However, this is far from the truth. With the rise of the US Dollar since middle of 2014, quite a lot of assets, as well as economies, have been affected. Eurozone, BRICs, Frontier markets and commodity producers are all feeling the pain. Raw materials (NYSE: RJI) are declining, emerging market currencies are under pressure and EU growth is very tepid. The picture isn’t all that rosy in the US either, as credit markets clearly show. High Yield (NYSE: HYG) and Investment Grade (NYSE: LQD) credit spreads continue to rise since middle of 2014.

Certain readers will state that, if we remove energy debt, credit spreads aren’t as high as the chart of the day shows. While this is true, readers should remember that prudent investor should not cherry pick any data, during any period. Crisis usually starts in a selected sector and spreads from there. In 2000, it was the Technology sector (NYSE: XLK). In 2006/07 it was the Financial sector (NYSE: XLF). Could the problem be linked to the commodity producers today? Energy and Materials (NYSE: XLE & XLB) continue to struggle, as already discussed in the previous post.