by Patrick O'Shaughnessy, CFA, Investor's Field Guide

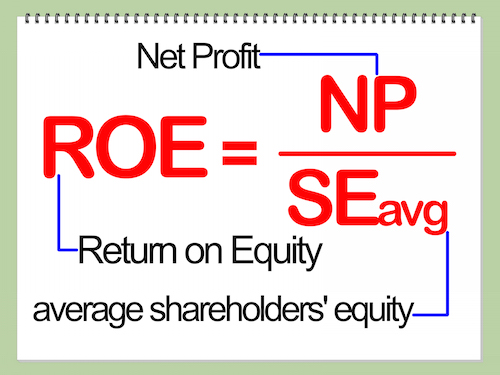

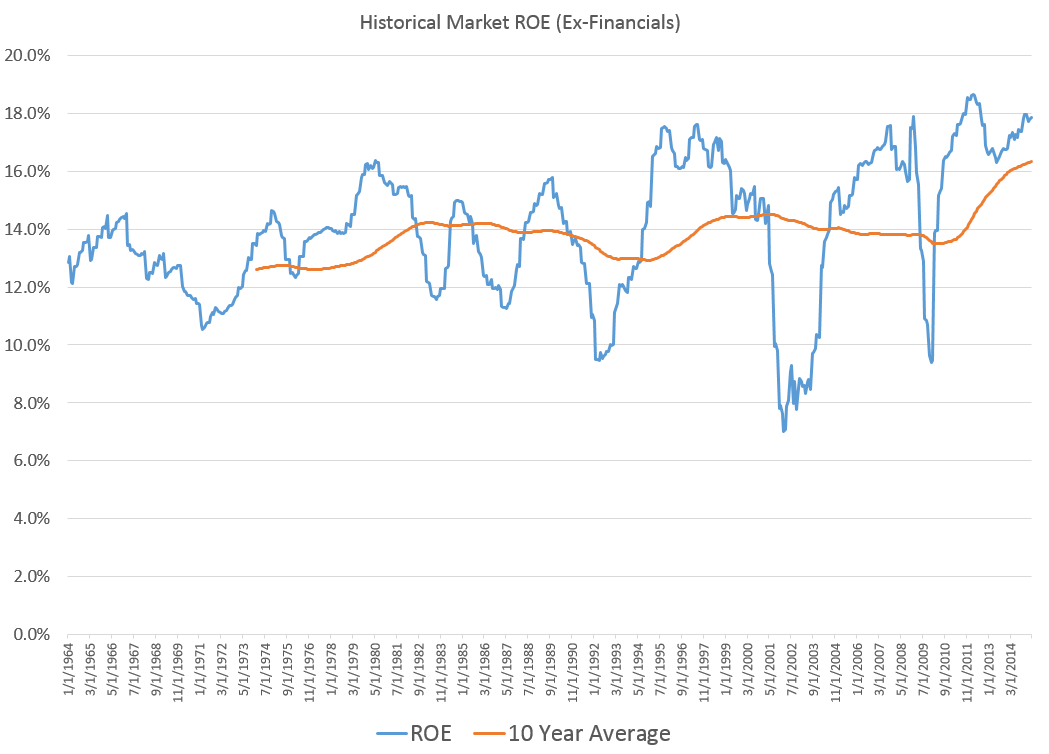

Non-financial firms are earning an impressive return on their collective equity value. As of April 30th, the U.S. markets return on equity was nearly 18%, well above the long term average of 14% for non-financial firms. Obviously, corporations like earning impressive returns on their equity. So what is driving today’s elevated rates, and what trends have mattered most for the trends in ROE? Here is the story, in chart form.First up, the market’s overall ROE, along with a smoother 10-year average. You can see its been pretty consistent, with a notable bump recently. The markets ROE is a function of three key ingredients: net profit margin, leverage (more leverage juices up ROE), and asset turnover (i.e. how many dollars of sales are companies producing for each dollar of assets–how productive are their assets). Here are the trends in those three factors.

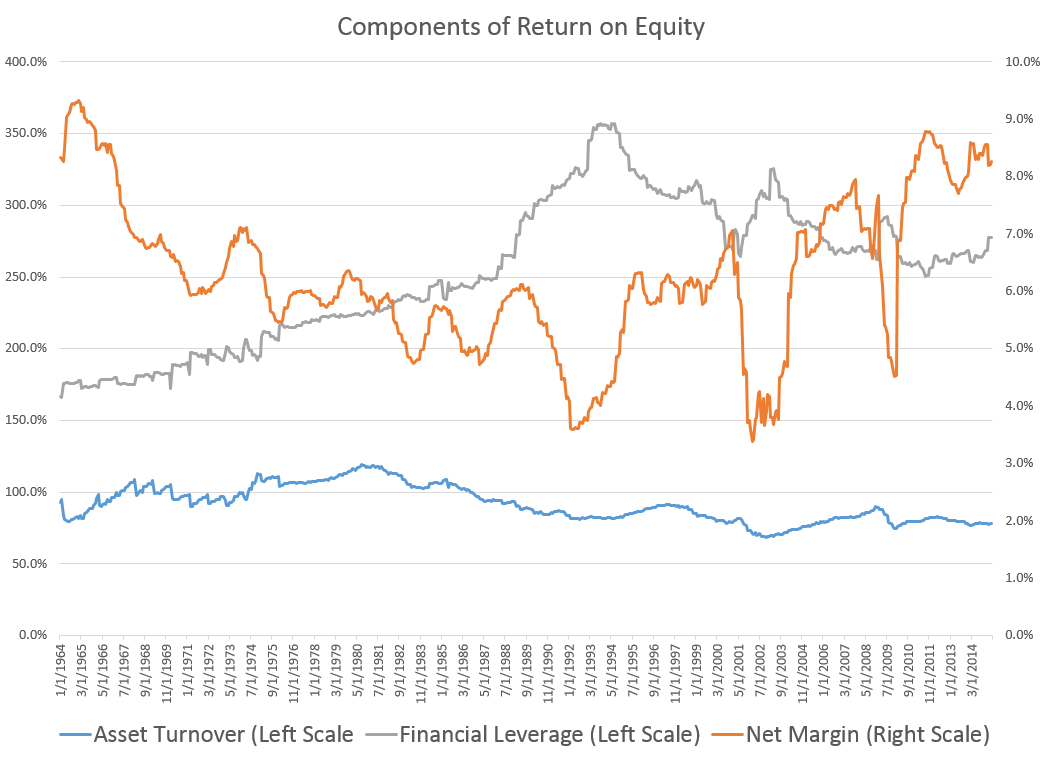

The markets ROE is a function of three key ingredients: net profit margin, leverage (more leverage juices up ROE), and asset turnover (i.e. how many dollars of sales are companies producing for each dollar of assets–how productive are their assets). Here are the trends in those three factors.

As Warren Buffett put it in a classic 1977 Fortune article,

As Warren Buffett put it in a classic 1977 Fortune article,

To raise that return on equity, corporations would need at least one of the following: (1) an increase in turnover, i.e., in the ratio between sales and total assets employed in the business; (2) cheaper leverage; (3) more leverage; (4) lower income taxes; (5) wider operating margins on sales.

The chart above shows that (1) asset turnover has been falling, and (3) financial leverage has been falling. So these two components are working against ROE.

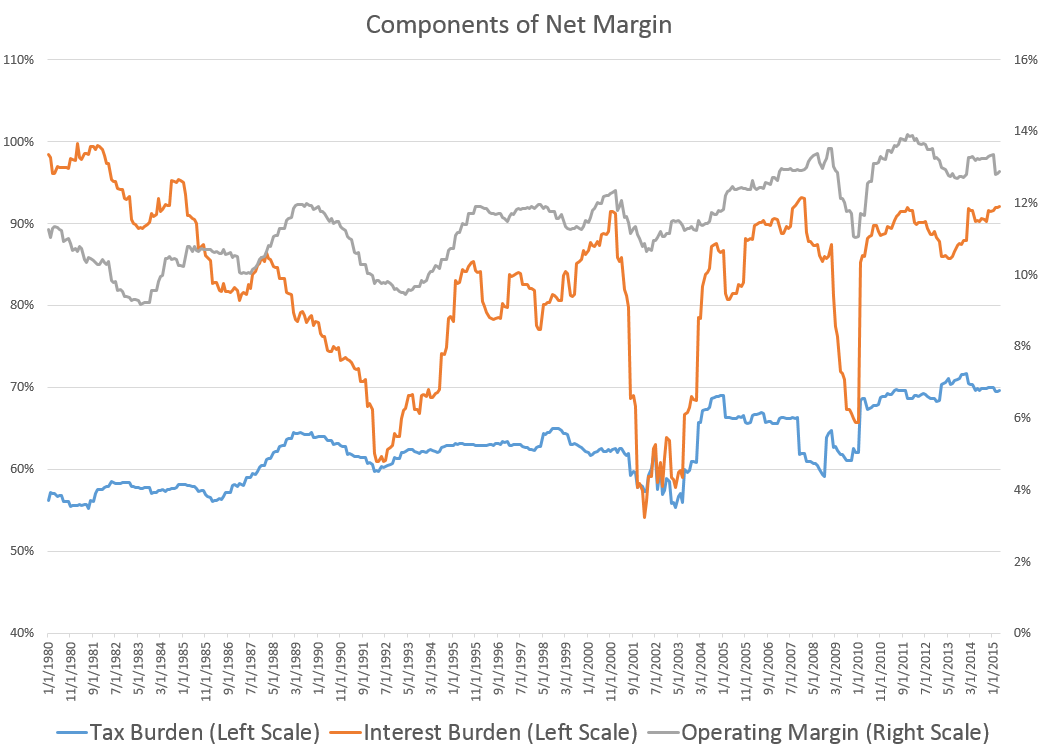

So the story must be in net margin–and to reach net margin we simply combine numbers (2), (4), and (5) from Buffett’s simple explanation above. These are, respectively:

- The rate of interest being paid (known as interest burden, this is the percent of operating earnings retained after paying interest on debt)

- The effective tax rate (known as tax burden, this is the percent of pre-tax profits that remain after paying taxes)

- And the operating margin

Multiply all three together, and you have net margin. It is simple: pay a lower tax rate, spend less on interest, and earn a higher margin on sales and margins go up. Here are the more recent trends (1980 on) in these components:

You can see that interest and tax measures are near highs, which companies like because it means they are losing less of their profits to interest and tax. This flows through to higher net margins, and therefore to higher ROEs. Operating margins are also strong, sitting about 1% lower than all time highs.

You can see that interest and tax measures are near highs, which companies like because it means they are losing less of their profits to interest and tax. This flows through to higher net margins, and therefore to higher ROEs. Operating margins are also strong, sitting about 1% lower than all time highs.

What do you think are the trends most likely to change or reverse?

***

About Patrick O’Shaughnessy, CFA

I am a reader, a writer, and a portfolio manager at O’Shaughnessy Asset Management. I love learning with an audience and connecting with curious people. I fell in love with the stock market after studying philosophy and psychology at the University of Notre Dame (markets are just people after all). I started in finance at the worst possible time, but have loved it ever since.

I am a reader, a writer, and a portfolio manager at O’Shaughnessy Asset Management. I love learning with an audience and connecting with curious people. I fell in love with the stock market after studying philosophy and psychology at the University of Notre Dame (markets are just people after all). I started in finance at the worst possible time, but have loved it ever since.

Copyright © Investor's Field Guide