by Cam Hui, Humble Student of the Markets

Despite my bullish stock market outlook (see my last post Enjoy the party, but watch for the police raid), a good investor always thinks about the risks to his forecasts. So it is in that spirit that I explore the scenario of what might trigger a bear market in 2015.

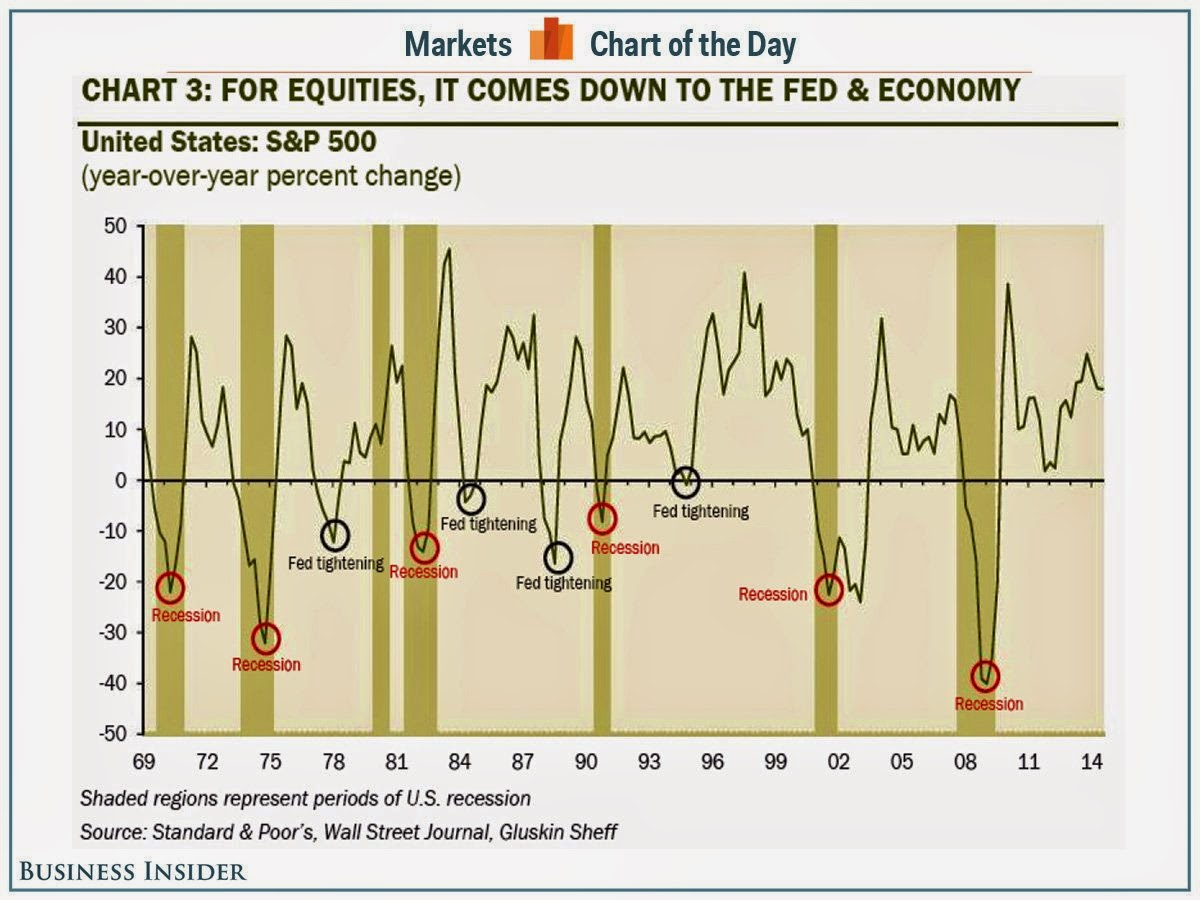

Rising rates don`t cause bear markets by themselves

Recently, David Rosenberg explained that bear markets are caused either by recessions or Fed tightening (I agree with 80% of that statement, but that`s another story, via Business Insider):

Right now, the market consensus is that the Fed will start to raise interest rates in mid-2015. But Fed tightening, by itself, will not cause equities to tank. That`s because the Fed is tightening in response to a rising growth and inflation outlook. Higher growth translate to higher earnings, which should push stock prices higher.

A HY bear attack?

What if the source of a bear market comes from somewhere else? I recently came upon the summary of the 2014 CFA Institute Fixed-Income Management Conference, where Martin Fridson called a wave of junk bond defaults to start in 2016:

Fridson, CIO at Lehmann Livian Fridson Advisors, has been a leading figure in the high-yield bond market since it was known as the “junk bond” market — and he sees as much as $1.6 trillion in high-yield defaults coming in a surge he expects to begin soon.

“And this is not based on an apocalyptic forecast,” he assured the audience.

High-yield bonds, typically issued with credit ratings at the bottom of the scale, tend to suffer default surges during troughs in the credit cycle. The first high-yield default surge occurred from 1989 to 1992, and encompassed the collapse of Drexel Burnham Lambert. The second surge ran from 1999 to 2003, following the bursting of the dot-com bubble, and the third happened in the midst of the global financial crisis, from 2008 to 2009.

Fridson suggests the next default surge will be larger than the last three combined. Each surge saw an average annual high-yield default rate above 7% (which, if extended over a multi-year period, can add up to real money).

Fridson currently projects that 1,155 issuers will default in the next wave. Over a four-year period that easily surpasses the 644 defaults in 1999–2003, the largest of the three prior default surges.

The trigger could be the Fed raising short rates:

One key assumption behind Fridson’s forecast is that the Fed ends its program of quantitative easing (QE) and allows interest rates to rise. QE may have ended, but Fed guidance calls for interest rates to remain low for a “considerable time.” Fridson was asked about QE and the persistence of low rates during Q+A after his presentation, and the answer left the audience murmuring.

“If we’re in this Fed rescue mode [in 2016–2019], then I think we’re in a lot of trouble. Very serious trouble.”

To be sure, Fridson had been forecasting a wave of junk bond defaults back in November, 2012 (via Bloomberg):

Almost $1.6 trillion of junk bonds globally will default between 2016 and 2020, according to Martin Fridson, chief executive officer of New York-based FridsonVision LLC, a research firm specializing in speculative-grade debt.

Steve Blumenthal also warned about rising default risk in July 2014 (emphasis added):

In my 20 years of managing high yield bond investments, I’ve never seen so many signals that scream caution. Desperate to find yield, investors have poured billions into high yield bond funds and ETFs driving the yield on the Barclays High Yield Bond Index to just 5.54% — the lowest level in history. Investors are positioning in a risk they may not fully understand.

Let’s look at what will lead to the next default wave and discuss a tactical strategy that may help you further participate in price gains and also protect your wealth during periods of significant price loss.

While 5.54% looks better than a 10-year Treasury at 2.46%, what is happening beneath the surface is concerning. A greater number of less credit worthy companies are finding funding and at terms unfavorable to investors. A default cycle is ahead.

Rising defaults + illiquid bond market = ???

Here is my bearish scenario. Could combination of Fed tightening, illiquid bond market cause a risk-off sell-off that spreads to other asset classes?

It is no secret that bond market liquidity has been shrinking because of higher capital requirements imposed on bond dealers (via Euromoney):

RBS recently surveyed 65 investors, including asset managers, hedge funds, insurance companies, private banks and others mainly based in Europe and the UK. Of these, the overwhelming majority (84%) sees lack of liquidity as a potential systemic risk for credit markets. Most say it is likely to get worse and while they are trying to manage liquidity risk, there is little consensus on how to do so.

Alberto Gallo, head of European macro credit research at RBS, argues: "Credit markets may have outgrown dealers’ capacity to trade risk. We have now nearly $7.7 trillion of credit in the US, versus $22 billion of inventories on trading desks, the lowest ratio in history.

"It is harder and more expensive to trade corporate bonds: liquidity is down roughly 70% since pre-crisis."

Bond market liquidity in both Treasury and corporates have been a problem for institutional investors:

"The Fed data suggest that the volume of corporate bond inventory the sell-side holds is about a fifth of what it was before the crisis," Nick Robinson, head of trading, fixed income at Schroders, tells Euromoney. "And the US corporate bond market has approximately doubled in size in that time.

"There have been lots of initiatives to try to address that. Many new agency brokers emerged very quickly – and subsequently disappeared – after Lehman collapsed. More recently, several crossing networks have sprung up, but to succeed they need a critical mass of clients while the market remains fragmented."

Another investor tells Euromoney: "Banks have very little inventory or balance-sheet capacity. At the moment there is a kind of spurious agency model with a bit of balance sheet behind it and a lot of smoke and mirrors."

Today, the HY bond market is not just the playground of institutional investors, but retail and fast-money hedge fund investors through ETFs. So what happens when default rates start to tick up and everyone tries to squeeze out a much smaller exit?

The worst-case scenario is that stresses from a HY induced risk-off sell-off cascades into a financial crisis in the banking system.

A 2015 problem

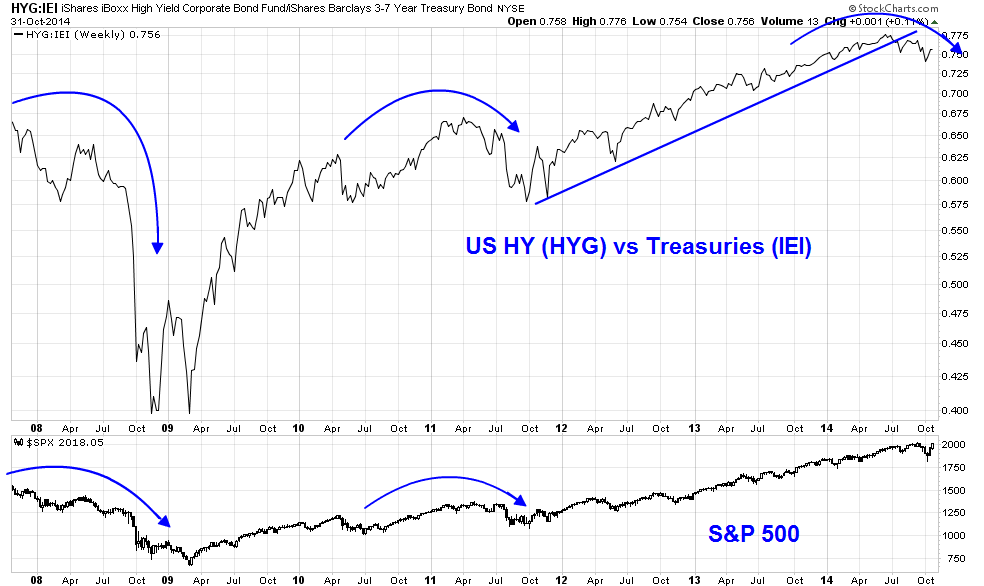

Today, junk bond market performance has started to roll over against equivalent duration Treasuries. Past episodes have led to stock market weakness, both in 2007 and 2011.

To be sure, the problem does not appear to be excessive today. Howard Marks isn't finding a high level of financial stress from rising defaults. He believes that the investment environment remains favorable for equity prices:

Speaking of the environment, since mid-2011, our investing mantra across Oaktree has been move forward but with caution. In the US, we see the economy getting stronger and asset prices getting higher although not generally in bubble territory. Economies elsewhere especially in Europe and certain emerging markets are weaker. We are respectful of the determination of central banks to stem economic weakness by keeping interest rates historically low and the appeal of riskier assets high.

More than five years into recovery as we are now, one would typically expect to see a pickup in defaults and other signs of distress. But of course nothing about this cycle has been typical so it isn’t surprising that defaults and distress remain in short supply.

In short, the potential stresses in the HY market is something to keep an eye on. For now, I remain cautiously bullish on risky assets. The risks in the junk bond market is a 2015 problem.

Copyright © Humble Student of the Markets