by David Fabian, FMD Capital Management

I’m breaking from my traditional analysis of a specific segment of the market to focus on a more comprehensive overview using several charts. Sometimes it’s nice to step away from individual sectors to monitor “big picture” trends along with some possible outcomes. Also, see my March 2015 Chart Review video for further analysis.

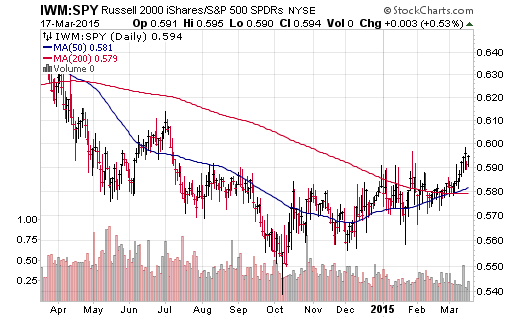

Small Caps Taking The Lead

The chart below shows the relationship between the iShares Russell 200 ETF (IWM) and SPDR S&P 500 ETF (SPY). More specifically, the big rounded bottom that you see is an indication small caps are starting to outperform their larger peers.

We saw the exact opposite of this behavior last year, which may be indicating that portfolio managers are seeing value in under covered small companies. There is also some chatter that smaller companies may be less susceptible to a strengthening U.S. dollar because they don’t have the global footprint that many multi-national large caps do.

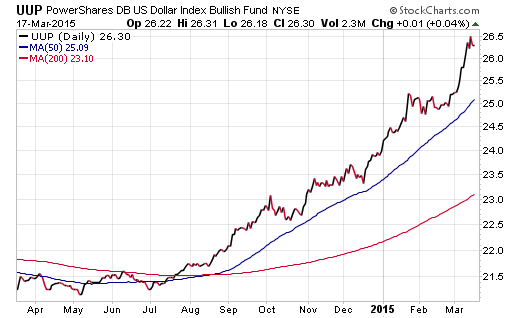

The Move In International Is All About Currencies

All you have to do is take a look at a chart of the PowerShares U.S. Dollar Bullish Index Fund (UUP) to see why international stocks continue to experience headwinds. Unless you are positioned in a currency-hedged ETF, the persistent upward momentum in the dollar is working against Europe, Japan, and emerging markets.

There are obviously a lot of factors at play here that include momentum, sentiment, central bank policy, and relative value. While it is natural to want to get bullish on this trend, I think that the vertical nature of the chart warrants some concern about jumping headlong into the dollar at this stage.

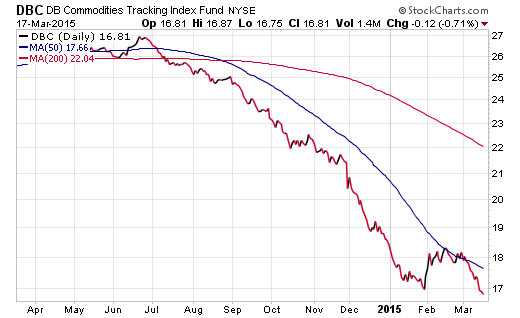

No Bottom In Sight For Commodities

A broad-based basket of commodities as measured by the PowerShares DB Commodity Index Tracking Fund (DBC) has continued to be an absolute disaster. Oil prices just hit new 52-week lows and gold bullion doesn’t seem to be all that far behind. Even base metals such as aluminum, copper, and zinc have continued to consistently bleed lower.

There is no denying that price is the ultimate arbiter of reality and commodities should be avoided until we see evidence of a long-term trend change. Many investors get sucked into the fundamental story of owning this asset class as an inflation hedge, but we are just not in that environment right now.

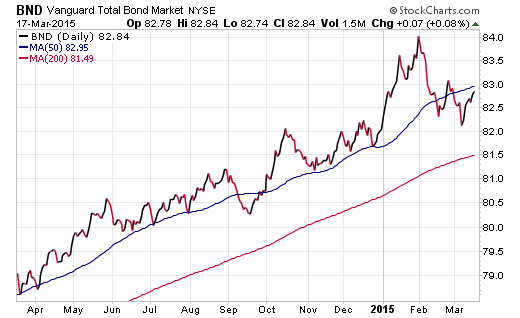

No Fear Of Rising Rates

Many investors are mentally preparing for a change in the interest rate environment, but the bond market isn’t convinced that rising rates are a threat quite yet. A look at a chart of the Vanguard Total Bond Market (BND) shows a mild hiccup in February as stocks soared, but overall stable price action that isn’t factoring in a major systemic shock.

U.S. bonds continue to be a “go to” hiding spot for foreign investors experiencing negative yields overseas along with a wide degree of support from the Federal Reserve. This will change at some point, but it’s far too early to call for the death of bonds like so many have in the past.

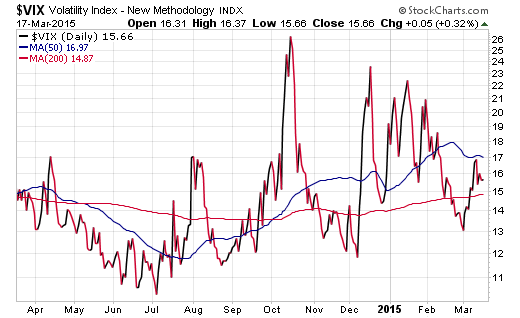

Volatility May Be Here To Stay

Note the last six months of volatility in the CBOE VIX Volatility Index (VIX). We are seeing more consistent up and down price action in stocks that leads to brief bouts of fear and greed. The end result is that we have made mostly sideways progress in the stock markets this year.

That sort of choppy price action may be here for a spell and makes things difficult for those with intermediate to long-term time horizons. The thing to remember is that patience will serve you well during this sideways trending market. You don’t necessarily have to be doing something all the time in order to have a successful outcome.

Those that prefer to be more active should focus on making strategic adjustments to your asset allocation to ensure your portfolio is aligned with your objectives and risk tolerance. You can also refine your watch list and start considering under what circumstances you would make changes to your holdings as market conditions evolves.

Copyright © FMD Capital Management