Stranded in NYC

by Jeffrey Saut, Chief Investment Strategist, Raymond James

March 9, 2015

The week began well enough as I arrived Sunday a week ago in Orlando for the 36th annual Raymond James Institutional Investors conference. As previously stated, there were more than 1,000 portfolio managers (PMs) and analysts there to listen to some 300 companies’ presentations. In addition to the PMs and their analysts, our analysts anchored the presentations by the CEOs and CFOs of those companies. The presentations I attended were packed, making it difficult to finds the ones that were lightly attended, which in the past has been an excellent indicator that those stocks should be bought (read: nobody has any interest, implying no one is left to sell). The one that really stands out was in March of 2009 when MarineMax (HZO/$25.64/Strong Buy) stock was trading under $2 per share, which was well below the value of its boat inventory. This year’s conference was the best yet, and our analysts have done a terrific job of capsulizing the highlights of those presentations (please contact your Raymond James salesperson). I personally saw a number of company management teams and met with numerous PMs from this country and abroad. Some of the more frequent questions were:

- Is the U.S. dollar going to stay strong? (I responded, “Yes.”)

- Is that going to hurt large cap companies? (yes, marginally)

- Are earnings estimates going to come down? (I think they have already over-reacted.)

- Are small/mid-caps better than large caps? (They are more expensive.)

- How about value vs. growth? (Value is less expensive than growth for small/mid/large-caps.)

- Have oil prices bottomed? (Yes)

- How about commodities? (I don’t have much interest, except with the Energy sector.)

And those, ladies and gents, were the most frequently asked questions, except for the ubiquitous question from the PMs, “What are individual investors doing?” My response here has often been chronicled in these missives. The individual investor, in aggregate, thinks the only reason stocks are up is because of the liquidity the Fed has supplied. As stated, they don’t consider earnings have improved dramatically since 2008 and that things are getting better. To be sure, the equity markets do not care about the absolutes of good or bad, but only if things are getting better or worse, and things are getting better. On that note, I left the conference early Wednesday morning to head to New York City for Arthur Cashin’s birthday party.

The party was held at my friend’s condo (Eric Kaufman) in the old J.P. Morgan building across the street from the New York Stock Exchange (NYSE). Eric is one of the founding members of Friend of Fermentation (FOF), a group that convenes at Bobby Van’s, which is caddie-corner to the entrance to the NYSE, every Thursday after the “close.” At the party were some of Wall Street’s “best and brightest,” including personalities like CNBC’s fair and brilliant Kelly Evans. The party was a smashing success and I was glad I was able to attend, having missed the FOF Christmas Party.

I awoke the next day to a blizzard and as the limo arrived to collect me for a TV appearance, I listened to the morning “squawk” on Bloomberg radio. One of the anchors said, “This is the worst winter since 1888!” That comment brought back thoughts of the “Great White Hurricane of 1888,” which I have written about numerous times. Around 9:30 a.m. I arrived at the “green room” to do Maria Bartiromo’s show and then returned to said “green room” following that “hit” to see if my flight to Tampa was going to be canceled. I waited for more than three hours as Delta kept saying everything was on time, even after their plane slid off the runway. The time was well spent, however, because I got to hug my friends Liz Claman and Liz MacDonald and catch up with them. Unexpectedly, Goldie Hawn was even there, which was a real treat! After more than three hours, Fox reported LaGuardia had been closed, so I trudged through the snow from 48th and 6th Avenue (Fox’s headquarters) to the Hilton at 53rd and 6th avenue to spend the night. Hereto, the extra time in NYC was not wasted because it gave me the chance to have dinner with Eric Kaufman and Joe Brusuelas, who is the Chief Economist for McGladrey. As always, the food at Mr. K’s was spectacular, but was WAY outdone by the conversation over dinner. I have talked with Joe many times before at various FOF confabs and always found him to have keen insights on the economy. Like me, Joe thinks a pickup in capital equipment spending is coming, which trumps just about everything else (read: improving economy). That stronger economy view came home in spades with Friday’s nonfarm payroll report, prompting our economist to write, “Another strong month. Market participants are likely to view this as bringing the Fed’s initial rate hike closer (June). Higher bond yields and a stronger dollar on the report.”

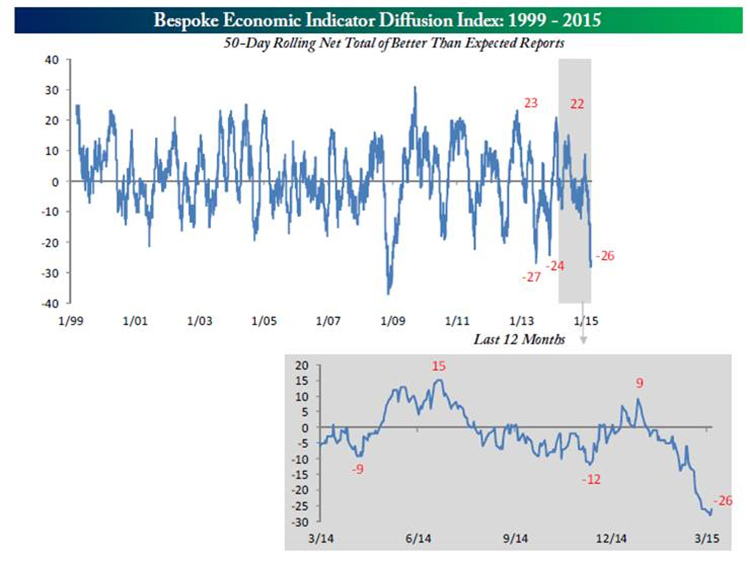

Plainly, the NFP report was strong, but in totaling the economic reports for last week shows of the 28 reports, 13 were weaker than expected, eight were stronger, and the rest were neutral. That’s okay, but it should not have been strong enough to cause a 300-point Dow Dump. Moreover it is pretty clear; yes, Ms. Yellen is going to raise interest rates, but it is going to be slowly. Further, if she is really “data dependent,” she should look at Bespoke’s Economic Diffusion Index that is near the lows recorded during the Financial Crisis (See chart 1 on page 3).

For me the two biggest events of last week were interest rates and crude oil. The rate ratchet left the 2-year T’note trading within 1 basis point of its highest yield in four years (@ 0.73%), while the 10-year T’note now changes hands at 2.24%, up ~36% from what we termed a “double bottom” at 1.65% five weeks ago. As for crude, it rallied following an inventory report that should have been bearish. Hereto, I think oil has bottomed. Recall it took four months, following the 66% price decline in 1985 – 1986, to form a bottom, and three months to make a base following the 1996 – 1997 50% decline. We like the energy sector here and would point you to the favorably rated names in our research universe.

Speaking to sectors, of the 10 S&P macro sectors only the Utility space is oversold. All the rest have either a neutral or overbought configuration. Looking at the 100 or so industries shows that many of them are out-performing the broad stock market. Those include technology, retail, restaurants, rails, industrials, healthcare, consumer staples, credit cards, biotech, autos, airlines, and asset managers. Asset managers are particularly interesting because a mere 1% increase in interest rates has a huge impact on bottom line earnings. This is likely why the NYSE ARCA Securities Broker Dealer Index (XBD/$184.84) tagged a new reaction high on Friday before settling back to close on the flat line. I continue to tilt portfolios accordingly.

The call for this week: So, to celebrate its sixth bull market birthday, the S&P 500 (SPX/2071.26) took-out its 2080 – 2100 support levels on Friday’s Flop and now has “eyes” for 2050 – 2060. Obviously, the large buildup of internal energy I have been discussing is being released on the downside, which is somewhat surprising, but not totally unexpected given the divergences highlighted in these reports. For example, in the past when the D-J Transports have failed to confirm the D-J Industrials new highs within six weeks, it has led to pullbacks of 8% to 10%. Moreover, early last week I talked about the S&P 500’s Bollinger Bands being at their narrowest since late 2007. That is typically a precursor to a decent move in the equity markets. The problem is, much like my internal energy indicator, it does not tell you which way the move is going to come. All it “says” is a pretty decent move is coming. So far the SPX has lost a mere 2.4% from its intraday high (~2118) of February 24th to its intraday low (~2067) last Friday. Given the Bollinger Bands, and the internal energy readings, that hardly seems like enough downside. The near-term positive is the McClellan Oscillator is as oversold as it was at the October 15, 2014 “selling climax” low. Longer-term, it is very positive that both the normal Advance/Decline Line, and the Operating Company Only Advance/Decline Line, made new highs last week. And, if past is prelude, the SPX has years left to run after emerging in 2013 from the range-bound parallel channel it was in from 2000 to 2013 (see chart 2). This morning the preopening futures are flat awaiting the commencement of Draghi’s QE program.

Copyright © Raymond James