by Jesse Felder, The Felder Report

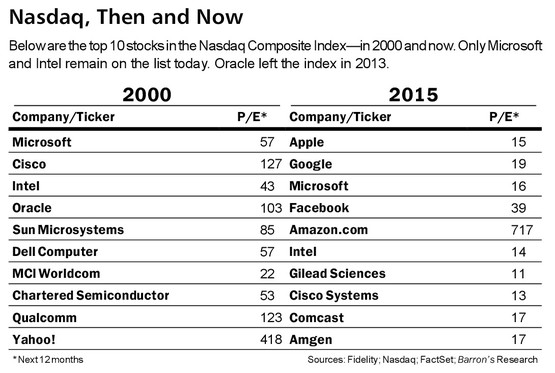

As the Nasdaq approaches its 2000 highs people are talking about the similarities and the differences between the market then and now. Most seem to be focusing on the differences, on how much more attractively-priced stocks are today than they were then. From Barron’s:

“What was propelling the Nasdaq in the year 2000 was a dream. What’s driving the Nasdaq today is reality,” says Gavin Baker, who runs the Nasdaq-focused Fidelity OTC Portfolio fund (FOCPX). “The current valuation is very well supported by earnings and cash flows and if those earnings and cash flows continue growing, the Nasdaq should continue going up.”

The article continues by predicting the index not only surpasses the 5,000 mark but surges as far as 7,000 in “coming years.” This is certainly possible but using the table above to make the case that the Nasdaq, or stocks generally, are cheaper today than they were then is just faulty.

The internet bubble was characterized by incredible euphoria and unbelievable valuations in just one group of companies. What investors fail to recall is that at the same time there were incredible values to be had in other sectors. The “old economy,” “bricks and mortar” companies had been left for dead as investors believed the internet revolution would put them out of business.

We don’t have a sector today that is nearly as overvalued at the tech/internet sector was in 2000 but we also don’t have any sector that is significantly undervalued:

Forward 12-month P/E ratio for $SPX Energy sector well above recent averages. http://t.co/4J1HDH1tTR pic.twitter.com/TTbMZiNuoE

— FactSet (@FactSet) February 20, 2015

In fact, virtually every sector is historically overvalued. This is why active managers and value investors are pulling their hair out right now:

"If the next 5 yrs are the same there won't be any active managers left." How the Fed's squeezed top managers of yore http://t.co/3qiCIfHN11

— Lisa Abramowicz (@LisaAbramowicz1) February 24, 2015

Rather than prove that stocks are cheaper today, that first chart above from Barron’s merely demonstrates why the stock market appeared to be more expensive back then even if it wasn’t. Because the indexes are market cap weighted, that relatively small number of incredibly overpriced companies in 2000 skewed the overall valuation of the market much higher than was true for the majority of stocks in the market and obscured the segments of the market that were actually cheap.

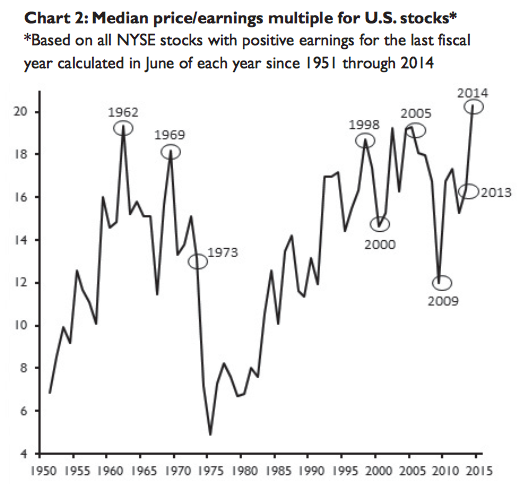

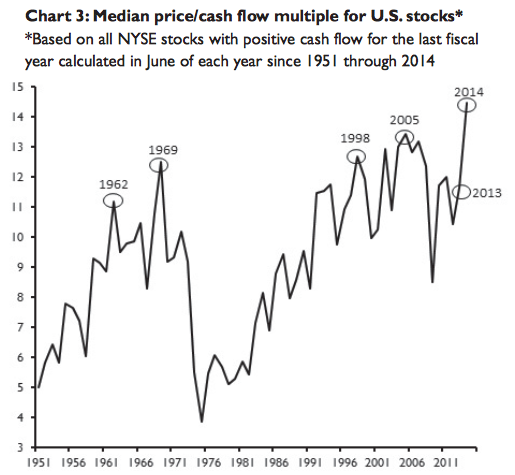

If we look at median valuations of the market then and now we see a completely different story. The median number, rather than the aggregate number, is a much better indicator of the valuation of the average stock in the market because it eliminates the bias of market cap weighting toward only the biggest companies. Whether you look at price-to-earnings or price-to-cash flow, the average stock in the market has never been more highly valued than it is today:

Charts via Wells Capital

Charts via Wells Capital

So don’t kid yourself. Stocks aren’t any cheaper today than they were at the height of the internet bubble. What’s truly “different this time” is that, rather than seeing incredible overvaluation confined to just one segment of the market, it is far more pervasive than it was back then. In my view, this also makes it far more insidious.

Copyright © The Felder Report