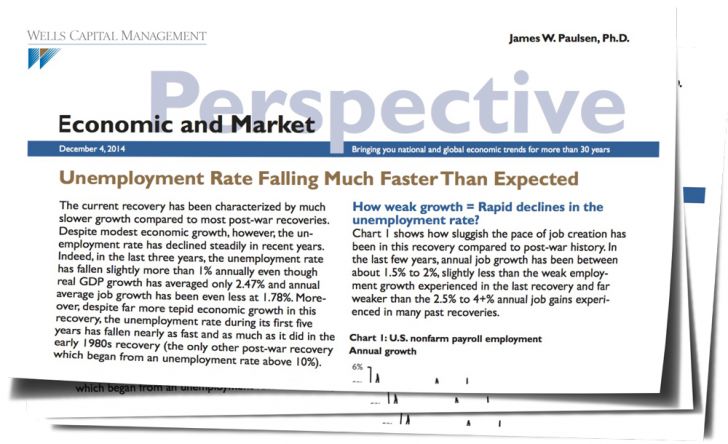

Promises, Over-Reach, and Mistaken Remedies

by Guy Haselmann, Director, Capital Markets Strategy, Scotiabank GBM

• Fed: Factors continue to line up for the Fed to raise rates at the March meeting. If the Fed were truly data dependent, a March hike would have become conventional market thinking, particularly given recently robust data. (UR 5.8%, PCE steady at 1.5%, ISM 58, Auto sales at 11 year high….). Markets must have no idea what the Fed means by being “data dependent” or maybe investors are focusing more on the relentless pessimistic rhetoric of FOMC members. If investors were looking at the data, I believe they would have shifted from the “lower for longer” mentality to my “sooner but slower” expectation.

• Nevertheless, as the economy continues to improve and now has the added benefit (for the most part) of lower oil, the Fed’s continued fear mongering about labor slack, soft wages, and deflationary potential is becoming outdated. The Fed should acknowledge that lower oil will filter into headline CPI, lifting real wages. How the Fed chooses to frame this discussion will be interesting.

• The Fed’s continual airing of concerns has misguidedly dampened business and consumer confidence. Therefore, isn’t it possible that an early hike could actually give a boost to confidence?

• Furthermore, I am confident that the economy could withstand ‘lift-off’. Few consumers are likely to change spending habits due to such a modest hike and they account for two-thirds of GDP. On the other hand, the impact that a hike would have on bubble-like financial markets are another matter. The longer the Fed waits, the worse the ultimate fallout is likely to be. If markets surprise and end up taking a hike without fanfare, then the Fed could raise rates again in June (a result that markets are unlikely to take as well the second time around).

• I suspect that, barring no ‘event risk’- type shock, the FOMC meeting on December 17th will be hawkish and followed by a more aggressive warning at the January meeting and ultimately a hike in March. I expect the watered-down-to-the-point-of-being Julia watchingmeaningless forward guidance language will be removed at the next meeting and include several acknowledgments of the improving economy. The yield curve in this scenario is likely to flatten materially.

• Here are some reasons why conditions today are ideal for a March hike.

1) Risks to financial stability. It is impossible for the Fed or anyone to know just how bad those risks have gotten. The Fed has a terrible history of causing ‘boom to bust’ cycles and is now purposefully trying to create asset price inflation. There is a weak correlation between equity market prices and GDP growth. However, it should be concerning that global growth forecasts continue to be lowered (as they have for the last several years) and yet global equity and credit markets continue to power to new highs. It has been QE and CB promises that has fueled rampant speculation. Furthermore, if printing were the cure-all elixir than the Zimbabwean economy would have had a better outcome.

2) The Fed is “close enough” to its dual mandate objective – and is highly accommodative.

3) Policies are fueling inequality which can have disastrous consequences.

4) Financial repression is bad long-run policy for any country.

5) The 35% decline in oil will boost the disposable income of consumers.

• BOJ: The bank is determined to drive inflation up to 2% because it is convinced a deflationary mindset is responsible for weak consumption and capital expenditures. This diagnosis appears incomplete. Japan seems to be in denial that its real problem is sinking population levels and a quickly aging workforce. Where is the 3rd arrow?

• It should not have been a surprise that Japan’s Q2 and Q3 annualized GDP were -7.2% and -1.6%. The Japanese people have come to expect a reduction in nominal wages. As the BoJ embarked on a plan to push inflation to 2%, the consumer is confronted with a further decline in their expected real wages. On top of that, the government then hits them with a consumption tax. Therefore, rather than being surprised, a retrenching consumer should have been widely anticipated by officials.

• The sinking yen is beginning to have far-reaching consequences, which will likely trigger counter-active policy responses from some countries in the region.

• ECB: Dragging out promises of broad-based QE or “doing whatever it takes” has had an enormous impact on financial markets over the last several years. Eventually, the impact from promises erodes over time. Some disappointment arose today as “move without delay” was pushed off until 2015. I guess Draghi was unable to secure the necessary votes for more action.

• The policy of ‘buying time’ to allow the complex political web to make progress used to work in the EU’s favor. However, time is now working against Europe. The people will only take no growth and high unemployment for so long. Protests and unrest have been containable, but there is quickly growing support for Anti-EU political parties. Important elections are looming in the next few years, beginning in 2015.

Central Bank Overview - Detrimental and Inadequate Tools

• The investment game is becoming more suspect and dangerous as asset price levels continue to ignore economic weakness and the lack of necessary political reform. Instead, many investors (not just in the EU) have become conditioned like B.F. Skinner rats to bid up financial risk assets whenever a central banker makes a promise about accommodation or further stimulus; this even occurs when data disappoints, because investors expect ‘the promise’ to soon follow.

• Fear of missing the upside and under-performing peers and benchmarks is what makes this reflexivity work. This is actually a sad state of affairs and an ever-more dangerous and epic game of chicken. This conditional response pattern is unsustainable. Indebtedness and market speculation continue to soar. In the end, printing is a not a solution, but a source of long-term harm to markets and national economies.

~ “History has not dealt kindly with the aftermath of protracted periods of low risk premiums” – Alan Greenspan

Regards,

Guy

Guy Haselmann | Director, Capital Markets Strategy

▬▬▬▬▬▬▬▬▬▬▬▬▬▬▬▬▬▬▬▬▬▬▬▬▬▬▬

Scotiabank | Global Banking and Markets

250 Vesey Street | New York, NY 10281

T-212.225.6686 | C-917-325-5816

guy.haselmann[at]scotiabank.com

Scotiabank is a business name used by The Bank of Nova Scotia

Read/download Guy Haselmann's Macro note below:

Copyright © Scotiabank GBM