by Sober Look

The Eurozone banks' longer-term borrowings from the central banking system continue to decline, a trend that many economists view as a form of "passive" tightening in the area's monetary conditions.

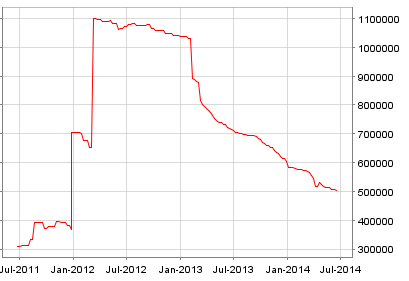

|

| LTRO balance outstanding (source: ECB) |

As discussed earlier (see post), the ECB will attempt to replace some €400bn of the lost balances with a new program dubbed TLTRO ("targeted" LTRO). Here is the official description:

The ECB: - Counterparties will be entitled to an initial TLTRO borrowing allowance (initial allowance) equal to 7% of the total amount of their loans to the euro area non-financial private sector, excluding loans to households for house purchase, outstanding on 30 April 2014. In two successive TLTROs to be conducted in September and December 2014, counterparties will be able to borrow an amount that cumulatively does not exceed this initial allowance.

During the period from March 2015 to June 2016, all counterparties will be able to borrow additional amounts in a series of TLTROs conducted quarterly. These additional amounts can cumulatively reach up to three times each counterparty’s net lending to the euro area non-financial private sector, excluding loans to households for house purchase, provided between 30 April 2014 and the respective allotment reference date in excess of a specified benchmark. The benchmark will be determined by taking into account each counterparty’s net lending to the euro area non-financial private sector, excluding loans to households for house purchase, recorded in the 12-month period up to 30 April 2014. All TLTROs will mature in September 2018.

The interest rate on the TLTROs will be fixed over the life of each operation at the rate on the Eurosystem’s main refinancing operations (MROs) prevailing at the time of take-up, plus a fixed spread of 10 basis points. Interest will be paid in arrears when the borrowing is repaid.

Starting 24 months after each TLTRO, counterparties will have the option to repay any part of the amounts they were allotted in that TLTRO at a six-monthly frequency.

Counterparties that have borrowed under the TLTROs and whose net lending to the euro area non-financial private sector, excluding loans to households for house purchase, in the period from 1 May 2014 to 30 April 2016 is below the benchmark will be required to pay back borrowings in September 2016.

The goal here is not just to pump up the Eurosystem's balance sheet, but, more importantly, to stem the relentless declines in corporate and household credit growth. The rationale for excluding mortgages apparently stems from fears of igniting another property bubble.

The portion in blue is particularly important. The ECB is "waiving a carrot" in front of the banking system: "do more lending over the next year and we will reward you with cheap funding."

Some argue that the TLTRO offering is useless because there is no demand for credit in the euro area. That's simply not true. The private sector credit supply/demand imbalance has widened significantly over the past year. Given the tepid growth in the Eurozone, the availability of credit is vital to maintaining the recovery. The ECB has finally given up on the notion of "creditless expansion" (see post).

|

| Source: Credit Suisse |

The biggest hurtle for the TLTRO program is the banks' unwillingness to grow private credit. The area's banks' ability to borrow based on their "loans to the euro area non-financial private sector" does not mean that they plow the new funds into the private sector. In fact analysts expect banks to borrow at 0.25% fixed for 4 years from the central bank and use a good portion of the proceeds to buy government paper that yields significantly more. Even at 0.37%, Spanish 1-year notes would be profitable for banks as a "carry trade".

|

| Spanish 1-y government bond yield (source: Investing.com) |

Part of the reason for this concern is the constant pressure to deleverage and tougher capital requirements under the new Basel rules. Short-term sovereign paper meets both, the minimal additional capital requirements as well as the liquidity criteria that banks are looking for. Why bother with personnel-heavy loan underwriting, high capital charges and illiquidity when there is easy money to be made. Government paper is in effect crowding out private credit.

Reuters: - Many analysts believe that, while bonds yields have narrowed substantially since the last LTRO, there is still an appealing carry compared with the 0.25% the ECB is charging for the funds. Sovereign debt carry trades will be doubly appealing because banks do not have to hold additional capital against such positions - but do against corporate bonds, loans to businesses and other assets.

"Carry trade yields have come down, but there is still money to be made," said Jon Peace, a bank analyst at Nomura. "With the zero risk-weighting on sovereign bonds, the carry trade will continue to appeal."

The carry trade will make the banking system the largest beneficiary of this program - as was the case in the previous 3-year LTRO offering. European bank shares are up some 60% over the past couple of years. Yet over the same period, private sector loans outstanding have been steadily declining. Some point to this program as being another example of central banks helping bank shareholders and irresponsible governments without significant benefits to the overall economy.

The argument from the ECB would be that only banks with large loan portfolios will be "rewarded" with this cheap financing, providing some level of incentives (particularly compared to the previous LTRO program). Furthermore, the improved bank profitability resulting from TLTRO is expected to help with the deleveraging process, which should result in a stronger banking system.

However, with all the easy money to be made in government bonds, the impact of the program on private sector credit expansion remains unknown.

Copyright © Sober Look