by David Templeton, Horan Capital Advisors

Quite a bit of discussion has occurred over the past several days regarding the fact value stocks are outperforming growth stocks. This outperformance has taken place since the beginning of March as can be seen in the below chart.

In looking at a longer view of the value growth cycle, growth had been the outperforming style since April of last year.

The importance of this fact has to do with the performance of these two styles relative to the economic or business cycle. As noted in a white paper, Forecasting Performance Cycles of Value and Growth Stocks in Global Equity Markets, written by David Kovacs, CFA of Turner Investment Partners,

"Following periods when short-term rates ease, lending activity and subsequently business development typically accelerate. During these periods value stocks, led by financial and industrial companies, begin to outperform. As the global economy begins to expand, demand for basic materials, such as metals, and energy related commodities, such as oil and natural gas, rises. That leads to an increase in the price of these commodities which in turn has historically led to the outperformance of the stocks of commodity producers and processors."

"As in the case of an economic slowdown, the monetary response to economic expansion is also typically delayed until sustained signs of acceleration in inflation are apparent. In response, central banks begin to hike short-term interest rates to the point where the interest rate yield curve is flat or inverted, i.e. short-term rates are either equal to or higher than long-term rates. Lending activity to businesses then typically slows significantly, profits of financial institutions decline, and financial stock prices begin to lag the market averages. Economic activity moderates, and once again those stocks that can grow their earnings at the fastest pace, namely, growth stocks, typically resume a period of multi-year outperformance."

In short, as the economy begins to accelerate, value companies begin to outperform. Conversely, when the economy begins to slow, those companies that can grow their earnings in spite of the slowing environment (growth stocks) will begin to outperform.

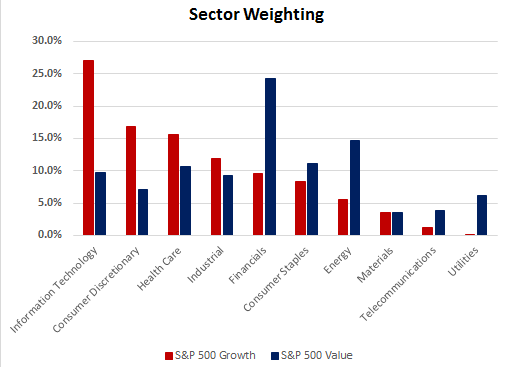

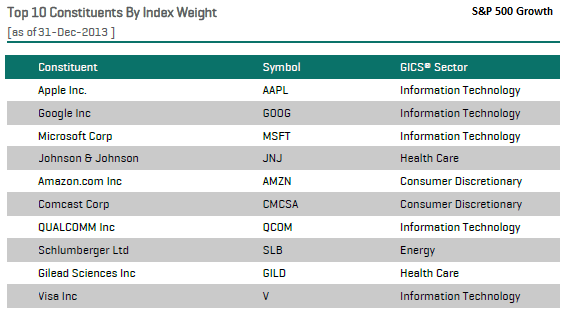

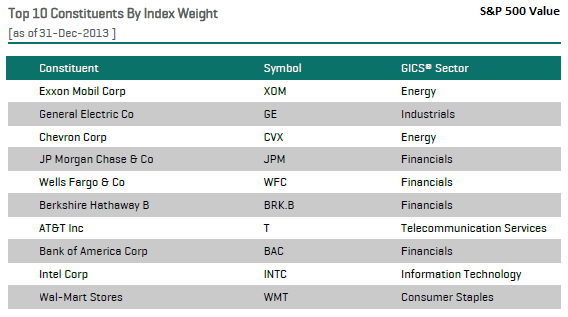

Below is a chart comparing the sector weightings for the S&P 500 Growth Index to that of the S&P 500 Value Index. Additionally, the last two charts show the top holdings for each of these indexes.

Source: S&P Dow Jones Indices

The stock market does tend to be a pretty good weighing machine on future economic activity. If the value style is in fact beginning to assume market leadership on a sustained basis, maybe economic activity is improving. We noted this fact in our post last week highlighting a few economic variables that would be indicative of a strengthening economic environment, Economic Data Continues To Support A Stronger Equity Market. For investors, looking at value stocks that have lagged the market advance that occurred in the second half of 2013 could provide some rewarding investment opportunities.

Copyright © Horan Capital Advisors