A New Inflation-Expectations Monitor

by James Paulsen, Chief Investment Strategist, Wells Capital Management

*Note to readers: A substantial portion of this research note was first published in May 2010. Because the primary indicator recently signaled a change in inflation expectations, we have updated the information and offer some new thoughts surrounding implications for both the economy and the financial markets.

Inflation expectations are constantly monitored by both investors and economic policy officials. Stock and bond investors frequently fear potential inflationary or deflationary risks and the Federal Reserve always faces a decision either to lean toward growth or against inflation. Since the 2008 crisis, the primary concern has been the potential for deflation. However, for the first time since the last recovery, broader inflation concerns may be returning. There are many popular inflation-expectation gauges including those implied by TIP bond prices, yield curve movements, and inflation surveys. However, another has emerged in recent years (the correlation between the daily movements of the stock and bond markets), which is not widely followed nor fully understood, but which nonetheless seems importantly tied to perceptions of inflation, to the efficacy of economic policies, and to the impact of rising interest rates on the stock market. Investors and policy officials should monitor the message of the “stock/bond correlation!”

Stock/bond correlation

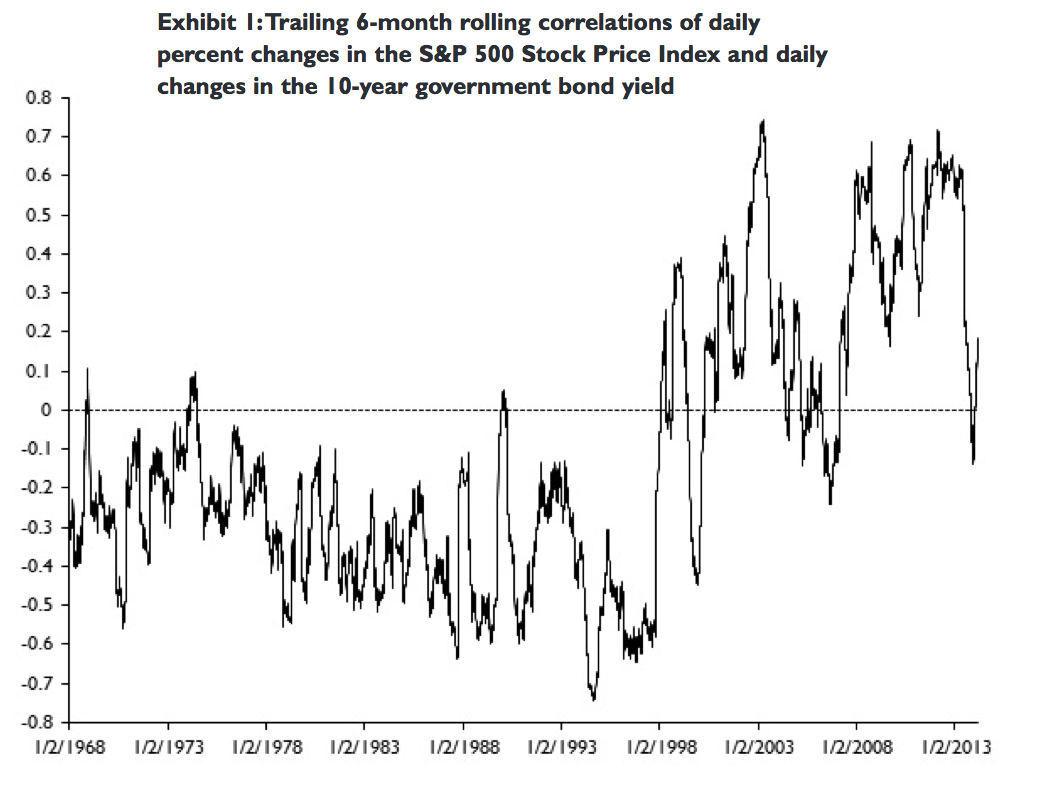

Exhibit 1 illustrates the trailing six-month rolling correlations since 1968 between the daily percent changes in the S&P 500 Stock Price Index and daily changes in the 10-year government bond yield. Correlation coefficients range between +1 (both variables move directly and perfectly together) and -1 (both variables move perfectly inversely to one another), and a coefficient near zero implies the variables mostly move independently. From 1968 until the late 1990s, the relationship between stock prices and bond yields was characterized by a persistent negative correlation. That is, higher interest rates were typically associated with lower stock prices. Since 1997, however, the correlation has typically been positive whereby rising interest rates are usually linked to gains in the stock market. What does the relationship between stocks and bonds signify and why did the correlation change so significantly since the late 1990s?

Read/Download the whole report below:

Copyright © Wells Capital Management