by Lance Roberts of STA Wealth Management,

Today there is a great sense of relief that has swept the nation as news flowed through the media that the government shutdown had come to an end. After all, during the 16 days of the shutdown, there was great hardship inflicted on the average American as the stock market rose by 2.4%, government workers that were furloughed received a 2+ week paid vacation and interest rates fell from a peak of 2.65% on October 1st to 2.59% on October 17th. Outside of the financial markets, which were never concerned of a "default," the reality is that the government shutdown did likely clip up to 0.5% off of 4th quarter's GDP. While that clip to economic growth created by the government standoff is temporary - the ongoing persistant weakness of economic growth is another issue entirely. This is the focus of this discussion.

The most disturbing sentence uttered during the debt ceiling debate/government shut down, that should raise some concerns by both political parties, is:

"We must increase our debt limit so that we can pay our bills."

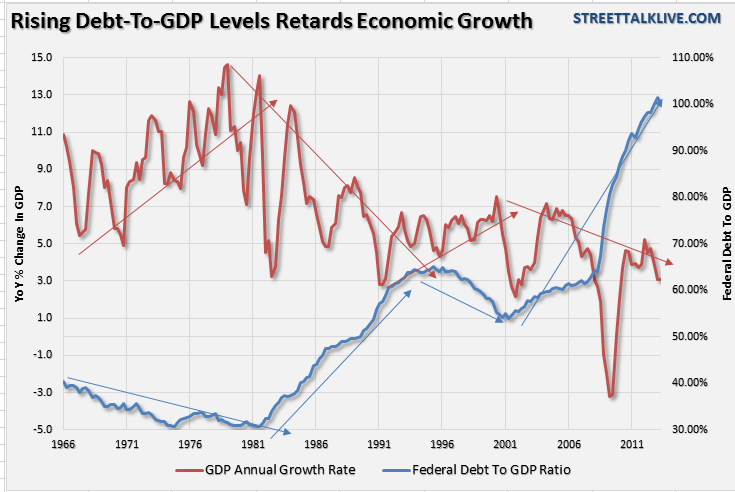

Think about that for a moment. The U.S. has become the single largest debtor nation on the planet as welfare dependency rises, government spending continues to increase and economic growth slows. However, what is ironic about this situation, is that it is the continuing increases in debt which is directly responsible for the decreases in economic growth. The chart below shows government debt as a percentage of GDP as compared to annualized rate of change in economic growth.

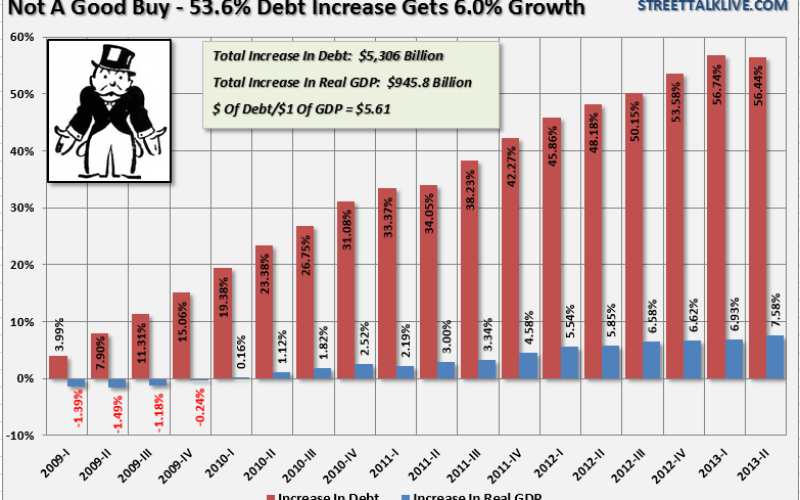

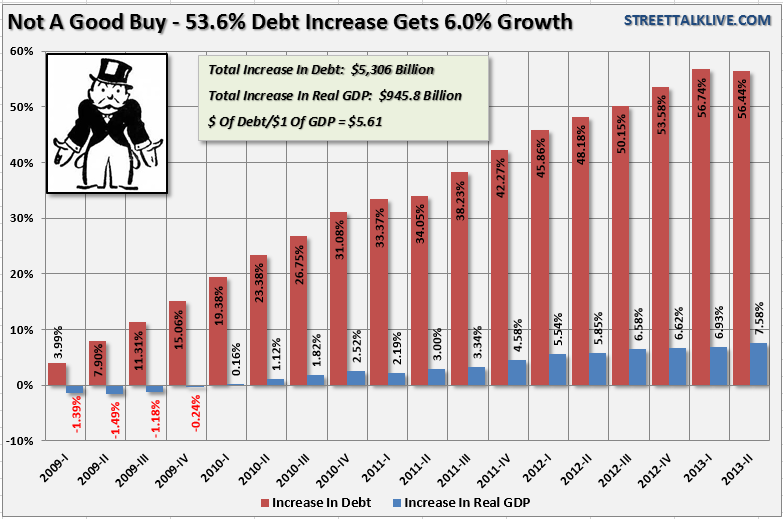

Since the beginning of 2009 very little of the increases in government debt, which was used to fill the gap created by excess expenditures, returned very little in terms of economic growth. In fact, as of the second quarter of 2013, it required $5.61 of debt to create just $1 of economic growth.

As I discussed recently in "The Long Game Of Hiking The Debt Ceiling:"

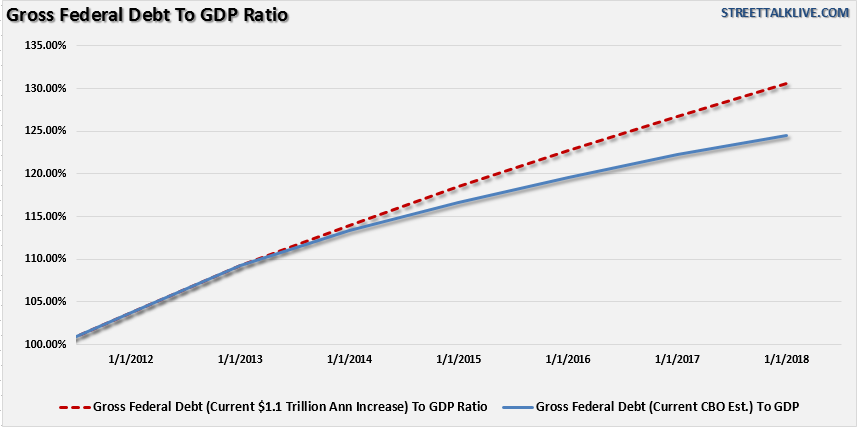

"The chart below shows the current projected rates of debt to real GDP through 2018 according to the CBO estimates versus the current annual run rate of $1.1 trillion."

"At the current rate of debt increase the U.S. will pushing 130% of debt to real GDP by 2018. This is, of course, not including the funding needs that will ultimately be required to support the increased costs of the entitlement programs of Social Security, Medicare and now the Affordable Care Act (ACA). The reality is that debt needs will substantially increase as entitlement programs continue to consume ever larger chunks of the current budget. By 2020 the current welfare programs alone are expected to require 75% of all federal revenues and this does not include the impact of the ACA. This, of course, is unsustainable."

President Obama was very correct in his speech, following the resolution of the government shut down, by stating that one of the three things that the government should focus on in the short term is budget reform. The current pace of increase in the participation of social welfare programs from food stamps and disability claims to social security and Medicare is creating an ever increasing consumption of current revenues. The implementation of another social welfare program will only create an additional drag on the revenue/expense equation.

While the President did note that the deficit was indeed shrinking; this is due to the massive surge in tax revenue created by the fears over the fiscal cliff. With the final tax filing and payment date, October 15th, now behind us we will begin to see the deficit once again widen. This is simply due to the fact that ordinary tax revenue trails government expenditures by a wide margin.

So, while the government shutdown is now temporarily behind us, at least for the next 90 days, the real battle lies ahead. Unfortunately, there is little desire to truly reform spending or the budget. It requires sacrifices that no one is willing to make. However, the wakeup call really should be the fact that we are making the statement that "we have to increase our debt simply to pay our bills."

Copyright © Lance Roberts, STA Wealth Management