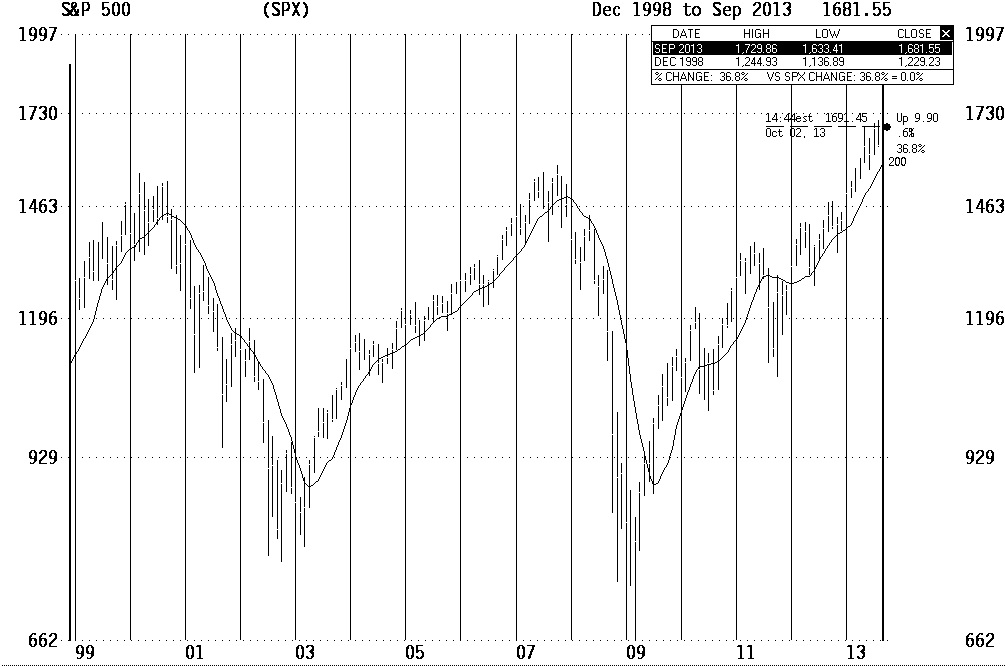

To understand where we are going and have confidence in the future, you have to understand where we’ve been. We thought it would be helpful to remind everyone where we’ve come from in the US stock market over the last 15 years. Below is the chart of the S&P 500 index from December 31, 1998 through the end of September:

Source: ThomsonReuters Baseline

The US stock market gained 452 points from 1229 at the start of 1999 to now. This gain of slightly more than 39% is less than a 3% annualized average gain and combined with dividend payments gave investors an average annual return of 4.09%. The stock market in the US has historically returned closer to 10% with dividends reinvested and for this reason, we contend, these recent returns have been very unattractive to both institutional and individual investors. What have we learned in these last 15 years which can help us to succeed going forward?

At the end of 1999, the S&P 500 was loaded with over-priced technology and telecom stocks. People were excited about the internet and how it would change our lives. The S&P 500 fell over 40% from March 10, 2000 to late October of 2002. If you had avoided those two popular sectors, you skipped the vast majority of the bear market. It can never be said often enough, it may be good to avoid buying that which is popular.

After the bear market in 2003, we believe it would have been very healthy for the US to have experienced a period of austerity, as a result of the stock market decline and recession caused by the tech-bubble break. Economies are like an oven: if you cook spicy foods in your oven and don’t clean it, the freshly-baked cookies taste like garlic and onions. Instead, we brought interest rates very low and quickly revived spending habits on the back of a real estate and emerging markets boom. Remember the first zero interest car loans? We couldn’t give Bin Laden the satisfaction of seeing us go through a prolonged cleansing, so we doubled down and caused a whopper of a cleansing later on. The lesson we learned is to not fear economic cleansing periods or occasional full-blown bear markets that accompany those adjustments.

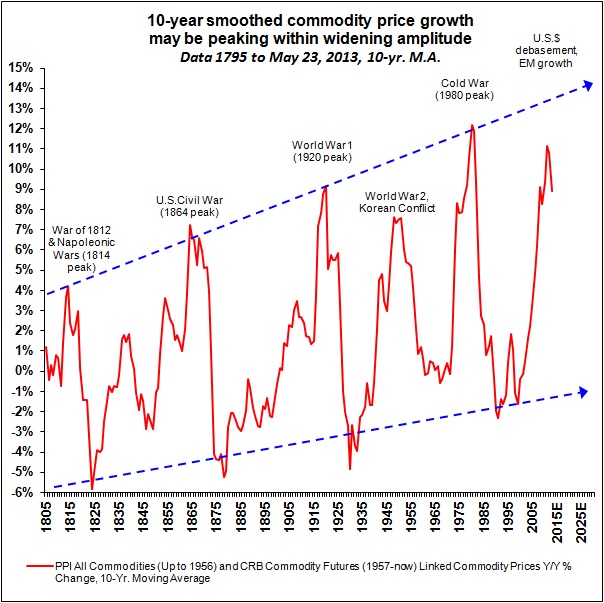

Some economic and stock market successes do not always travel well. Most of the gains from 2004 to 2007 in the US stock market were driven by success in commodity-based companies like oils and basic materials. They were suckling on the boom in China and emerging markets which triggered one of the greatest bull markets in commodity history.

Source: Stifel Nicolaus Barry Bannister May 23, 2013

The pleasure for investors in those sectors came at a huge price to the rest of our economy and ultimately, the US stock market. History has shown that massive commodity and oil price hikes are closely correlated with deep recessions, think 1973-74 and 1980-82.

Broken manias can temporarily crush the economy. The residential real estate bubble which peaked in 2005-06 poisoned the US stock market. The ensuing unwinding of that bubble exposed severely under-capitalized banks and exposed consumer behavior way outside the means of the average US citizen. The massive liquidation and panic circumstances caused a downward spiral. Warren Buffett called it, “An Economic Pearl Harbor.” I remember conversations in late 2008 and early 2009 with long-time clients. They asked if they should sit in CDs until the storm blew over. I asked them where the deposit insurance backing CDs comes from. They said, “The Federal Government.” I asked where the Federal Government got their money to insure deposits at the bank. They said, “Tax revenues.” Lastly, I asked, “Who pays the most taxes to the government?” Once they understood that the answer was the companies whose stock they wanted to sell, they settled in nicely.

We think staring into the abyss in late 2008 and early 2009 created one of the few once-in-a-lifetime buying opportunities of our years in the business. Being “greedy when others are fearful” played out in spades. Believing that the US economy would cleanse itself and that there is a bright future for democratic capitalism has earned back the money lost from late 2007 to early 2009. John Templeton coined the phrase, “the point of maximum pessimism.” Trust the reverse psychology and recognize the bargains which are available due to pervasive pessimism.

The last fifteen years have included a very difficult adjustment for the economy and two historically-large bear markets in the US. We don’t believe a relatively negative period like this should dissuade the owner of quality large-cap US equities, which are well-selected and meet a strict series of criteria. Since we know where we’ve been, now we can look at where the pessimists see us going and where we see us going.

Vision of the Pessimists

It is our view that if you believe the brilliant pessimists who dominate the media and are the most read, you would believe the following: the world has too many people and there is no way to feed and transport any more people. The debt hanging over us at the federal government, mortgage, consumer installment and student-lending level will require a decade or longer to work off. This means avoiding the US consumer, who is seen as shackled by this debt overhang. Profit margins in the US will revert to the mean. These lower margins mean to the pessimists that stocks are at a peak and shouldn’t be purchased until margins have reverted. Returns have been so strong since the bottom in March of 2009 that they have to correct in a major way. Lastly, the only place in the world to find growth is in China and the emerging markets. In other words, the best days of America are in the past.

The Vision of Smead Capital Management

We believe:

- The developed market countries which grow their population via births and immigration will be great places to invest. The only one that we have confidence in on that score is the US. America has 86 million people between the ages of 18-37 which are at an average age of 28 years old. Women get married at an average age of 26.9 and men marry at 28.7 on average. This mean a slug of babies are coming as a by-product of these unions. The Bible says, “Be fruitful and multiply.” We see that as a key to economic growth.

- Commodities hit a five-standard deviation high in July of 2011. Over-planting and over-production will lead a decade-long bear market in commodities. The bear market in commodities will bottom at the cost of production, in our view. Most reports show oil has a $50 per barrel cost of production. Lower commodity prices are a huge stimulus to the US economy!

- The debt overhang works itself off over the next 15 years. Those waiting until then to benefit from the ownership of companies which fit our eight proprietary criteria for stock selection are making a mistake. The last time we had a big federal government debt overhang was after World War II. The Fed capped rates for 6 years and profit margins reached 10% of GDP, very similar to today. From 1952 to 1966, interest rates rose and profit margins reverted. However, the Dow Jones Industrial Average nearly quadrupled!

- Deflation is the primary problem from a debt overhang. Our “addicted customer base” companies are likely to gain market share and maintain prices better than their competition in a deflationary environment. In an inflationary situation, the “addicted” customer is at the mercy of the product or service seller.

- Economic recoveries in the US are historically led by housing and autos. Since housing and autos didn’t start to recover until 2012, the rebound from the abyss in 2009-2011 was not led by the recovery; it was led by a lack of sellers. The sellers exhausted themselves by following the advice of the “brilliant” pessimists who have underestimated the malleable nature of the US economy and citizens. This economic recovery could be very long lasting because it will include debt reduction and most recession’s correct debt-driven excesses.

- China’s economy must have a major recession/depression to cleanse itself of capital misallocation, fraud and graft. By pegging their currency to the dollar, China prevented the booming growth of the last twenty years to equate to a highly-valued currency. High currency values historically corrected booms by making exports expensive. Therefore, China imported our easy monetary policy via the Yuan/dollar peg. Eliminating our easy money policy will strengthen the dollar and the Yuan will rise with it. On top of those exporting problems, the Chinese banking system is loaded with loans which won’t be repaid (FITCH) and the four major government-owned banks could see their equity bases wiped out by admitting the un-repaid loans. As the fixed-asset investment driven model dies, commodity use in China will revert to the mean.

- Under-ownership of US large cap equities, as represented in the NACUBO study of college endowments, shows that major institutional investors have followed the advice of the “brilliant” pessimists. It will take five to ten years to rectify this misallocation.

- Slow, consistent economic growth is driven by four main factors. Relatively low interest rates, great demographics, immense housing affordability and record-setting technology-driven productivity. We see those factors providing a favorable environment for our companies and giving us great confidence in the future.

We are excited about the future and are pleased that our 27 companies have thousands of hard-working employees who get up every day to better themselves, their families, their company and us as shareholders. Thank you for the ongoing confidence and trust in our work at Smead Capital Management.