The longer-term outlook for the U.S. stock market remains favorable, but moves in the NYSE advance/decline line suggest caution in the weeks and months ahead.

by Scott Minerd, Global CIO, Guggenheim Partners LLC

I hold a bullish long-term view of equities as an asset class, but it appears the stock market is in for a rough summer. One of my favorite indicators is the New York Stock Exchange advance/decline line (NYSE breadth) which is calculated by taking the difference between the number of advancing and declining stocks in the equity index. In the most recent equity market decline, NYSE breadth dropped more than equity prices, which can indicate a larger sell-off coming in the near- to medium-term. Although equities have recently rallied, mature markets often exhibit this type of behavior as they come closer to topping. The current outlook for equities has parallels with the trajectory of stocks in 2007.

In that year, breadth turned down by 17 percent in February, while the Dow Jones Industrial Average only declined 6 percent. Although equity prices then enjoyed a brief rally in the spring, the divergence foretold further downside risk, which materialized in July of that year when equity prices collapsed by nearly 10 percent. A similar pattern could be playing out today. The oversold position in the stock market last month and declining market breadth seems to indicate that, while equities are now enjoying a rally, investors should view it with caution. This is a rally to sell, not to buy. Given the deteriorating technical indicators and worrying signs in the global economy and particularly in China, it is likely that stocks will see more damage before the end of the summer.

Chart of the Week

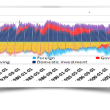

Deteriorating U.S. Earnings Expectations

The deterioration of earnings pre-announcements from U.S. companies highlights an increasing concern over the sustainability of the recent growth in corporate earnings. By June 30, 87 S&P 500 companies had issued negative second quarter earnings guidance, whereas only 21 companies had issued positive guidance, suggesting slower earnings growth ahead. The ratio of positive-to-negative guidance has declined to its lowest level since the start of the current bull market in March 2009.

In combination with a strong dollar and rising concerns over a slowdown in China, this suggests corporate profits could be disappointing. During the second quarter, companies with the highest exposure to China significantly underperformed. If China’s economic growth continues to slow, the sell-off in U.S. equities could significantly increase.

S&P 500 NEGATIVE AND POSITIVE EARNINGS PRE-ANNOUNCEMENTS

Source: Bloomberg, Guggenheim Investments. Data as of 6/30/2013.

Economic Data Releases

Retail Sales Weaken While Prices Rise on Energy

- Retail sales grew less than forecast in June at 0.4%, with sales excluding autos and gas down 0.1%.

- Industrial production rebounded in June by 0.3% after falling in April and May.

- The Empire manufacturing index for July increased to 9.46, a six-month high.

- Housing starts dropped 9.9% in June to an annualized pace of 836,000, the slowest in 10 months.

- The NAHB housing market index rose to 57 in July, the highest level since January 2006.

- Initial jobless claims rose by 14,000 to 360,000 for the week ended July 6th, the highest since the beginning of May.

- University of Michigan consumer confidence ticked down for a second month in July to 83.9.

- The June CPI increased more than expected, up 0.5% for a year-over-year reading of 1.8%, the highest since February.

- The PPI jumped to 2.5% on a year-over-year basis in June, the highest since March 2012.

Euro Zone Production Contracts, China’s Growth Cools

- Euro zone industrial production fell 0.3% in May, breaking a three-month streak of increases.

- The ZEW survey of economic sentiment in Germany unexpectedly decreased in July to 36.3.

- China’s second quarter GDP expanded 7.5% year-over-year, in-line with estimates and the second consecutive decrease in growth.

- China’s industrial production growth was below expectations at 8.9% year-over-year, falling for a second straight month.

- June retail sales in China grew 13.3% in from a year earlier, the fastest pace since December.

Copyright © Guggenheim Partners LLC