by William Smead, Smead Capital Management

We returned recently from the Berkshire Hathaway Annual Shareholder Conference. The most exciting and profound comment to us was what Warren Buffett said about the unprecedented actions the last three years by the Federal Reserve Board. Buffett was asked about the risks of the Federal Reserve’s current plan to buy Treasuries to keep interest rates very low. Buffett said he has faith in Federal Reserve Board Chairman Ben Bernanke, but did acknowledge that it will be a “shot heard round the world” as soon as it looks like the Fed’s Treasury buying plan winds down. At Smead Capital Management, we have been thinking for over one year about the ramifications of the open market setting short-term interest rates and the Federal Reserve Board beginning to reverse their “quantitative easing”. We looked closely at the winners and losers from the current policy and it brought us to today’s key question. What if Yen weakness/Dollar strength is already the “shot heard around the world” and most market participants are missing this fact?

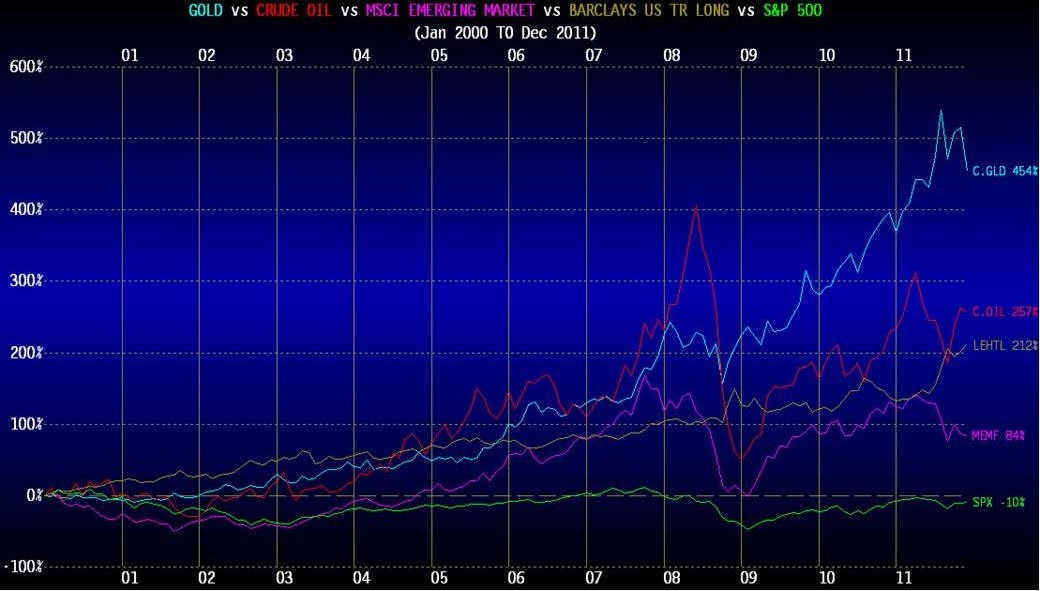

Interest is a cost of capital and is an opportunity cost. As short-term interest rates have declined since the year 2000, a host of industries, companies and countries have been major beneficiaries. On the other hand, companies with strong balance sheets and consistently high free cash flow create their own capital and have—at least to us— been severely undervalued in this era of near zero short-term interest rates. In our view, any capital intensive endeavor has been greatly enhanced by the cheapness of short-term debt. Look at the chart below which shows some of the investments which won or lost from the beginning of 2000 to the beginning of 2012:

Low interest rates funded capital intensive growth in industries like agriculture, mining, heavy industrial and basic materials. Fast growing emerging market nations build infrastructure, are huge absorbers of capital and heavy users of commodities. Led by China, a positive and virtuous circle developed in the first decade of the 2000’s. China pegged their currency against the US dollar, which effectively tied them to the Fed’s easy money policy. Instead of the dramatically higher Yuan that a boom would normally cause, the Chinese benefitted from the damaging affect that higher oil prices had on the US dollar and got away with extending their boom for three to five years longer than the economic history we have read would have indicated without the currency peg.

Emerging nations built infrastructure, using massive commodity quantities in the process. This caused huge growth in the industries and countries involved in producing commodity inputs. In turn, it caused those countries to boom and build their own additional infrastructure. Stock markets in emerging countries received a mother-lode of new money from US asset allocation firms and advisors. Currencies of countries who were the winners since 2000 bathed in affection from money flowing to them at the expense of the US consumer. Unfortunately for international investors and commodity bulls, this all changed on October 25th, 2012, when the Yen last traded at 80 per US Dollar. Borrowing cheaply in Japan and enjoying the appreciation of the Yen versus the US dollar was a bonanza for those chasing Asian emerging markets and the associated commodity boom. Look at the chart below to see how Yen weakness against the dollar turned things upside down:

The chart above is exactly the kind of asset-class performance our firm envisioned in the event that higher US short-term interest rates were allowed by the Fed. What we really underestimated was the incredible movement of capital which would occur when the carry trade (borrowing in yen) and investing in other asset classes ended. It has ended because, in our mind, nobody can withstand the currency devaluation to keep the cheap loans based in yen. You don’t have to wait for Ben Bernanke and Mr. Buffett’s shot, from our vantage point, the weak yen and dollar strength are doing the trick just fine.

In our capital appreciation strategy, we own no energy, basic materials and heavy industrial company shares. We have avoided companies which have enjoyed the benefit of China’s un-interrupted growth and stayed away from anything related to the countries which gain the most from the bull market in commodities (which China helped create). These are countries like Australia, Brazil, Russia, Indonesia and Canada. We believe that their currencies are inflated and their boom could become a bust when China lets the reality of business cycles catch up to them. Ironically, this bust in commodity prices could be the perfect stimulus to the slow and consistent recovery of the private sector economy in the US. For commodity importing countries like Japan and states like California and New York, lower oil and input prices are a Godsend.

Lastly, we have expected that higher short-term interest rates would damage the profit margins of US companies which are capital intensive and/or carriers of sizable debt loads. Therefore, we don’t want to own utility and telecom companies on top of not wanting to own the cyclical sectors we mentioned before. Also, there are serious concerns we have with indexing in a period which could have a significant bifurcation between the ten S&P 500 sectors. In our opinion, it would be a pity to get a solid understanding of what Warren Buffett talked about and then attempt to put it into practice the next ten years through passive indexes which over-own capital intensive and highly leveraged companies.

Best Wishes,

William Smead

The information contained in this missive represents SCM’s opinions, and should not be construed as personalized or individualized investment advice. Past performance is no guarantee of future results. It should not be assumed that investing in any securities mentioned above will or will not be profitable. A list of all recommendations made by Smead Capital Management within the past twelve month period is available upon request.

This Missive and others are available at smeadcap.com