Submitted by Charles Hugh-Smith of OfTwoMinds blog,

Wages, private-sector employment and labor's share of the economy have all declined: no wonder the risk-on recovery is rolling over.

Did anyone seriously believe the global economy was expanding so robustly that corporate profits would loft ever higher? Based on what data? Laughably bogus data from China, where warehouses are bulging with stockpiles of aluminum and copper, and a diminishing-return housing/credit bubble is the only "engine of growth"?

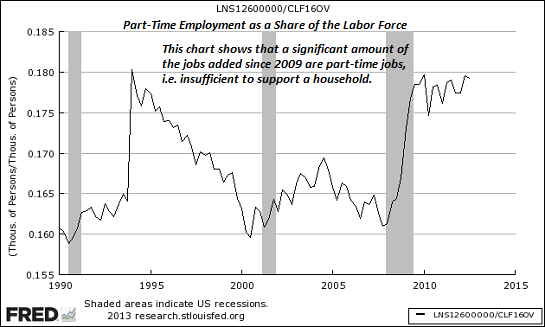

Or was it the equally bogus unemployment rate in the U.S. that inspired such confidence? Did money managers really not notice that most of those new jobs are part-time, and that the rate is only low because millions of people have statistically been disappeared from the workforce by central planners?

It's like the old Soviet propaganda trick of airbrushing out the comrades who fell from favor or who'd been given a "tenner" in the gulag. Millions of American workers have been airbrushed out of the picture, and presto-magico, the unemployment rate is a mere 7.6%.

Did anyone seriously believe the risk-on trade, driven entirely by central bank intervention and currency wars, was sustainable? Didn't anyone notice that beneath the veneer of forward earnings growth and other happy-talk, the real driver of the stock, bond, real estate, bat guano, etc. markets was all intervention, all the time?

Did anyone seriously believe fundamentals no longer mattered? Or did everyone just do the Chuck Prince tango, where you keep dancing until the liquidity-financial repression music suddenly stops?

It was all bogus and doomed to roll over, because the only fundamentals that count are not the levers the Federal Reserve pulls but employment and wages. Pulling the interest rate lever, the liquidity lever, the bail-out-the-banks lever, the buy a trillion dollars of fetid stinking mortgages lever, the buy SPX futures contracts via proxies lever, the POMO lever--they've all failed to move the needle on the only fundamental that counts, full-time private-sector employment.

Pushing the risk-on trade rewarded the 5% who own enough stocks to matter, and the top 1/10th of 1% who reaped the trading profits, but it didn't do diddly-squat for the bottom 95%.

Take a look at these charts. (all charts courtesy of frequent contributor B.C.)

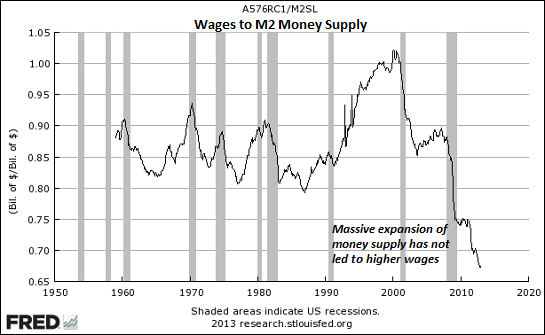

Ramping up money supply did not lead to higher wages--unless you count the bonuses on Wall Street, of course.

The Fed pulled all its levers to maximum, and the economy created a few million part-time jobs.

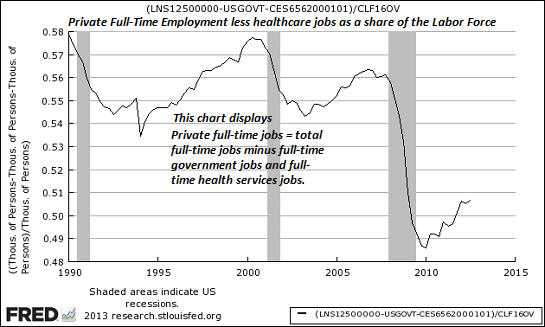

Subtract government employment and sickcare-cartel jobs, and private-sector employment is at multi-decade lows.

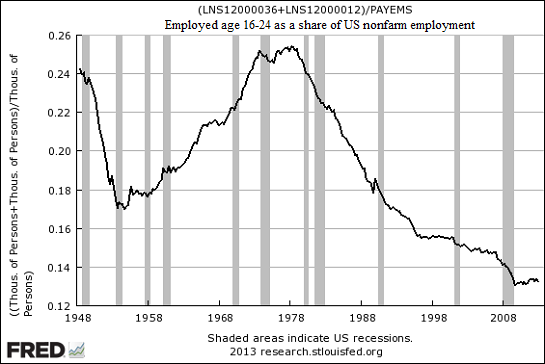

Employment for people ages 16 - 24 is abysmal.

Here is the Bureau of Labor Statistics on the labor participation trend for the 16-24 age cohort:

From 1948, when the series began, to 1989, the July labor force participation rate for young men showed no clear trend, ranging from 81 to 86 percent. Since 1989, however, their July participation rate has trended down, falling by about 20 percentage points. The July labor force participation rate for young women peaked in 1989 at 72.4 percent, following a long-term upward trend. The participation rate of young women has fallen by about 15 percentage points since 1989.

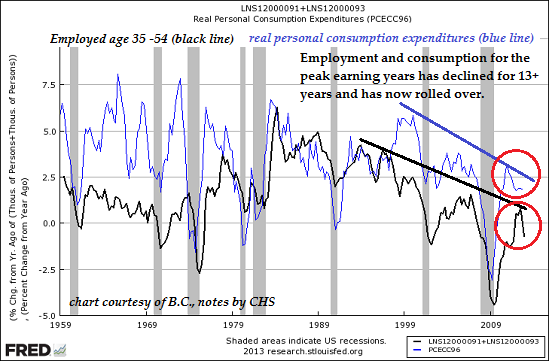

The most important labor cohort is ages 35-54, when workers' earnings peak. Both employment and personal consumption have been declining for well over a decade, and both have rolled over:

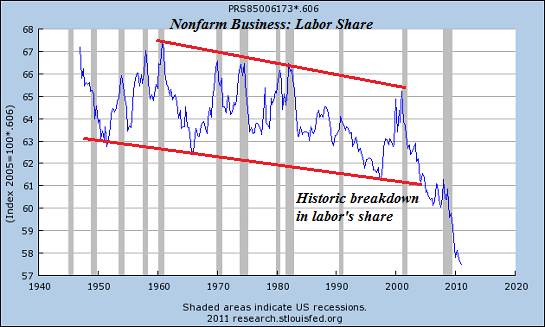

Labor's share of the economy has plummeted: what color lipstick would you like on your risk-on pig?

Wages, private-sector employment and labor's share of the economy have all declined: no wonder the risk-on recovery is rolling over.

Copyright © http://www.oftwominds.com