Emerging Markets Radar (January 21, 2013)

Strengths

- China’s fourth-quarter GDP grew 7.9 percent, better than the 7.8 percent estimate and up from 7.4 percent for the third quarter. December industrial production grew 10.3 percent versus the consensus of 10.2 percent, and up from 10.1 percent in November. Retail sales were 15.2 percent versus the consensus of 15.1 percent, up from 14.9 percent in November and the highest in the last 10 months. Fixed asset investments in December rose 20.6 percent, versus the consensus of 20.7 percent. Finally, power output rose to 432.7 kilowatt hour in December, a four-month high. Those numbers confirmed China’s growth recovery has momentum coming into 2013.

- The Bank of Thailand, the central bank, revised its forecast for GDP growth this year to 4.9 percent from 4.6 percent, citing strong domestic demand, especially private investment. Infrastructure projects connecting within the country and with Myanmar and urbanization in northern Thailand are catalysts for developers and construction engineering and materials businesses.

- Chinese A-share defense names declined on Thursday, indicating Chinese investors expected no military clash with Japan over disputed islands in the East China Sea.

- The Philippines’ manufacturing production index grew 9.6 percent in November last year, with structural catalysts in fiscal spending and upbeat consumption.

- Citigroup expects China A- and H-shares to rise 15-20 percent more in the first half of 2013, while UBS expects A-shares to rally 20 percent in 2013.

- Turkey’s economy is clearly accelerating: the Purchasing Managers’ Index (PMI) reading is at 53, December industrial production was 11.3 percent higher than last year, and annualized credit growth is now around 20 percent.

Weaknesses

- China’s GDP grew 7.8 percent in 2012. It was the lowest in the last 13 years, though the highest growth rate in the world. Essentially, China is entering a modest high growth stage.

- China’s Ministry of Railway announced its 2013 railway infrastructure investment target of 520 billion renminbi (RMB), up 1 percent from 2012, slightly below the market expectation. Nevertheless, a large proportion of China’s infrastructure investments are still in highways and urban transit improvements.

- Jakarta was flooded this week with more than 200,000 people displaced from their homes and businesses halted, showing the need for infrastructure improvement.

- The Thai policy rate was expected to remain unchanged at 2.75 percent, though no inflation risk is expected.

- Smog in Beijing was so bad that people had to put on masks to walk in the street, but it also drove up environment-related stock prices.

Opportunities

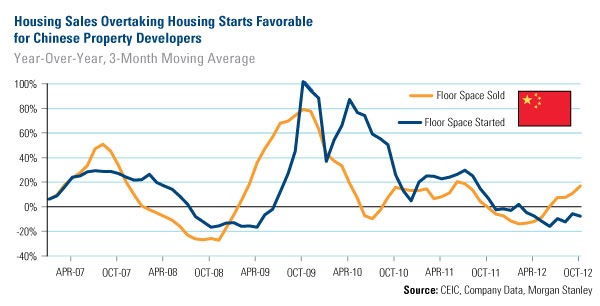

- The chart above shows that floor space sold has been leading floor space started since summer last year in China. With the running down of inventory and shrinking supply, demand and supply are reaching equilibrium, which will be supportive to housing sales and prices, and hence the stock price of H-share developers.

- China’s final consumption contributed 51.8 percent of GDP growth in 2012, while the contribution of net goods and services exports was negative 2.2 percent, according to China’s statistics, which showed progress in China’s transition to a consumption-driven economy.

- Historically, emerging markets dividend yields have largely been in line with the developed world. But dividend growth has cumulatively been stronger in emerging markets. The compound annual growth rate (CAGR) since 2004 was 8.3 percent in emerging markets and 4.8 percent in developed markets.

Threats

- Pollution in China, as demonstrated by Beijing’s smog this week, resulted in increased costs in health and economic growth. China may tighten pollution criteria, which is good for long-term development, but negative for auto and manufacturing sectors in the short term.

- Russian GDP has been decelerating since the second quarter of 2012. The December data out next week will likely present a picture similar to the previous month.

- Industrial production in Poland dropped 12.2 percent in December, another signal to ease policy. As in the U.K., most loans in Poland are not fixed rate but floating, which means banks will be hurt and not helped by lower interest rates.