Just Say No! to Excessive Debt and Leverage

By Frank Holmes, CEO and Chief Investment Officer, U.S. Global Investors

Just when you think it’s over, a bailout comes again. It’s expected that Ireland will receive an estimated $110 billion rescue package and IMF officials have already swooped in to begin auditing the books of the troubled country’s banks.

Ireland’s economy is in disarray. The Globe and Mail reports that approximately one-fifth of the country’s population is facing mortgage default, unemployment is above 13 percent and the government’s budget deficit has climbed to 30 percent of Ireland’s GDP.

Ireland’s Central Bank has already kicked in $50 billion to recapitalize the banks but it wasn’t enough to prevent Irish banks from insolvency. Fiscally-troubled Portugal and Spain have been instructed by the European Central Bank to tighten the screws to prevent contagion across Europe. Ireland’s crisis has caused volatility in worldwide financial markets, reminiscent of the botched Greece bailout earlier this year.

The mismanagement of debt by governments directly and indirectly in Europe seems like déjà vu to what we saw in Latin America in the 1980s and Indonesia and Thailand in the 1990s. Once again, it is government policy that allowed banks and governmental agencies to overleverage their balance sheets.

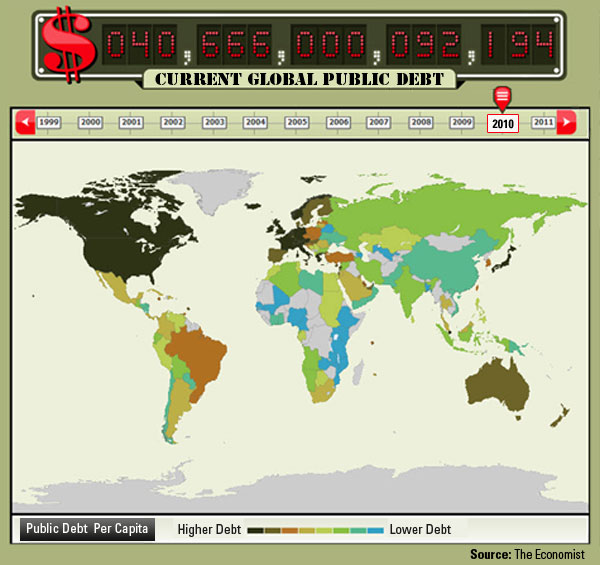

This isn’t specific to Europe. Globally, governments have run up a $40 trillion tab of public debt. You can see on this map from The Economist that the worst offenders are those in the developed world such as the U.S., Canada, Western Europe and Japan.

The question is how will these debts be reduced?

Some argue for austerity programs but when France moved to increase the official retirement age from 60 to 62 in an effort to get the country’s spiraling public finances under control, there were riots in the streets. Others argue for more regulation but that will only require the government to hire more workers at higher salaries, such as legions of attorneys to write and enforce more rules.

The answer to how debt will be reduced is we must cure governments and corporations from their addiction to debt and leverage. We must say no to feelings of entitlement. With less debt, hard work and less entitlement, governments around the world can return to a path of stable growth and fiscal responsibility.

This will require a substantial shift in government policies and the change will likely be a long, arduous process as governments work to shed that extra debt they’ve loaded up on.

Asked whether an aid package for Ireland from the European Union and the International Monetary Fund could be the last bailout needed, Treasury Secretary Geithner said he thought it was possible. "It is within the capacity of the Irish Government and the European authorities to achieve, and I believe they will achieve that because this government, Ireland, has demonstrated that they are willing to do some very, very difficult, very, very hard things to dig their way out of this mess," he said.

I hope this hard work and the luck of the Irish leads them back to the path to prosperity.