Emerging-Market Debt: Putting the Fiscal House in Order

by Shamaila Khan, Christian DiClementi, Emerging Market Debt, AllianceBernstein

With inflationary pressures under control and external balances improving, many emerging-market (EM) countries are working on the next item on their to-do lists: reining in fiscal deficits. That’s good news for emerging equities, dollar-denominated bonds and local-currency debt.

EM countries have been dogged by financial challenges over the past few years. The taper tantrum of 2013 was a major setback that scared off wary investors and triggered significant EM outflows. And already-shaky economic scenarios in many countries caused even more disarray.

Fiscal Adjustments: A Bitter, Necessary Pill

Fortunately, policymakers across the developing world aren’t standing pat. In many countries, they’ve been hard at work reigning in fiscal imbalances to win back the investors who fled. It’s a difficult but necessary rebalancing process that’s helping countries achieve better fiscal health. Steps we’ve seen governments take include overhauling tax structures, restricting spending, and reforming pensions and other social expenditure programs.

Here are a few examples of what countries have been doing to get their fiscal houses in order:

Brazil: Approved austerity measures that included a cap on public spending to help control the country’s burgeoning budget deficit; social security reform is also expected.

Colombia: Passed significant tax reform, including a higher value-added tax and a lower corporate tax, which should stimulate investment and growth. The country has also taken steps to crack down on tax evasion and improve tax collection.

India: On track to implement a goods-and-services tax—essentially a single tax that will replace local levies—making it easier to do business in the country.

Indonesia: Reduced fuel subsidies as part of promarket efforts to reform its economy.

Mexico: Initiated the gradual phaseout of fuel subsidies and pledged to achieve a primary budget surplus for the first time since 2008.

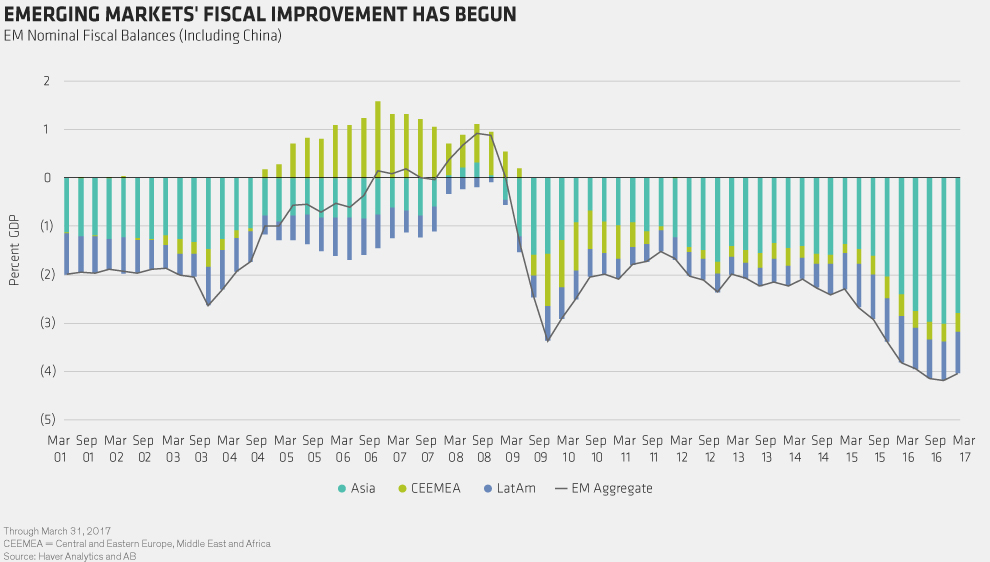

Thanks to these efforts, countries are beginning to see the proof in the pudding. Collectively, deficits are shrinking (Display), and that’s helping to set the foundation for long-term, sustainable economic growth.

The Appeal of Local-Currency Debt

So what does all of this mean for EM bonds? To start with, the shift toward tighter fiscal policies has helped to boost currency values in many emerging countries, and we see room for further appreciation, provided governments continue to tighten their belts. That makes local-currency-denominated bonds an attractive way to increase exposure.

Along with attractive currency valuations, these securities offer real—or inflation-adjusted—yields that are significantly higher than are those available on high-grade developed-market (DM) government debt. Real interest-rate differentials between emerging and developed bonds, meanwhile, are hovering near record highs.

What’s more, fiscal consolidation has helped cause inflation to peak or decline in many key emerging markets. As long as DM interest rates remain relatively low, increased exposure to select EM bonds makes a lot of sense.

Don’t Fear the Fed

Should investors worry about rising US interest rates? After all, the US is moving toward fiscal expansion, as are Japan and other developed countries. Won’t that push up interest rates in advanced economies?

To an extent, yes. We’ve already seen that happen, with the US Federal Reserve hiking rates twice since December. But it’s not likely to narrow real interest-rate differentials by much. Remember, rates are rising from record low levels and are likely to remain low by historical standards for some time. And a gradual rise in rates that’s accompanied by strong US growth is actually good news for emerging markets, since a stronger US economy will boost global economic activity and commodity prices.

Rolling Out the Welcome Mat

Many EM countries today are busy rolling out the welcome mat to investors. We see opportunities in several countries, including Brazil, Colombia, Indonesia and Mexico. In each case, we see promising developments: declining external imbalances, an improving growth outlook, political stability, room to ease monetary conditions, and stable or declining inflation.

As long as EM fundamentals continue to improve and DM interest rates remain relatively low, there will be a strong argument for investors to come knocking again.

The views expressed herein do not constitute research, investment advice or trade recommendations and do not necessarily represent the views of all AB portfolio-management teams.

Copyright © AllianceBernstein