by Russ Koesterich, Portfolio Manager, Blackrock

Russ explains why the post-election selloff in bonds may be a longer-term, not temporary, phenomenon.

The unexpected outcome and potential consequences of the U.S. presidential election continue to shake financial markets. Nowhere is this more so than the U.S. bond market.

Yields on the 10-year Treasury are up 50 basis points (bps, or 0.50%) since the election and nearly 100 bps from the July lows, as bonds sold off. This marks the fastest rise since the so-called “taper tantrum” in 2013, when expectations of an increase in interest rates by the Federal Reserve triggered a bond selloff.

After such a sharp selloff in bonds, we could arguably see markets settle down and prices stabilize for a bit. But over the long term, I would argue the selloff in bonds—and corresponding rise in yields—will continue for two basic reasons:

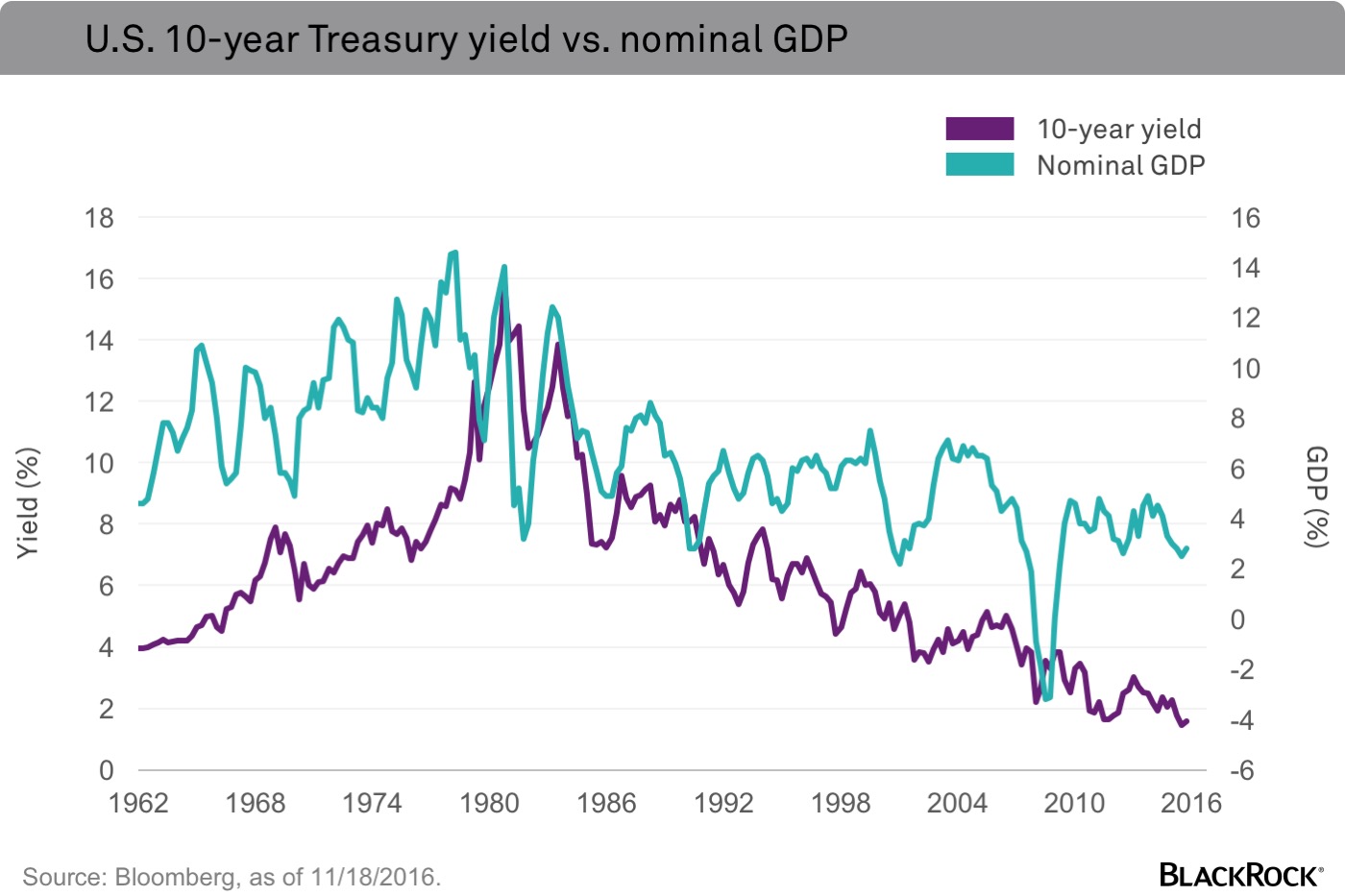

Higher nominal GDP growth going forward

Whether the new administration’s policies lead to faster economic real growth (after inflation) is an open question. But they are almost certain to lead to faster nominal growth, which includes inflation. This is important because over the long term it is nominal growth that drives rates. Going back to 1962, nominal growth has explained roughly 35% of the variation in U.S. 10-year Treasury yields (see the accompanying chart). Roughly speaking, 10-year yields increase 50 bps for every one percentage point increase in nominal growth.

Today, nominal growth is slightly under 3%. To put that number in perspective, prior to the 2008 financial crisis nominal growth averaged better than 7%, including during recessionary periods. A modest rebound back toward the upper end of the post-crisis range would thus suggest a rise in 10-year yields back to approximately 5%. While an increase that high is unlikely given structural headwinds (such as demographics and the deflationary impact of technology), it suggests yields still have further to rise.

More bonds to sell

In recent years, bond prices have been supported by a dearth of bonds coupled with strong demand from institutional investors. Banks, insurance companies and pension funds will continue to need long-dated fixed income instruments, but supply is starting to grow.

Both corporate and household debt are now rising at or near the fastest pace since the financial crisis. On the corporate side, the conservatism that marked most of the post-crisis environment has given way to a willingness to add to debt, often to fund buybacks and dividends. For U.S. households, although debt growth remains well below average, borrowing rose by 4.4% annualized in Q2, only the second time since the financial crisis that growth eclipsed 4%. And over the long term, federal borrowing is also likely to grow and deficits increase, absent entitlement reform. The Congressional Budget Office forecasts a baseline projection of an $814 billion deficit by 2021; and that does not include the potential impact of a large tax cut.

To be clear, relative to the 60+ year average of around 6%, 10-year Treasury yields are still likely to remain low. Nevertheless, in an environment of heightened duration, or volatility, the backup in yields will still cause considerable pain, unfortunately. I would continue to advocate that investors should underweight bonds and bond market proxies, such as utilities and consumer staples. Instead, faster nominal growth suggests more reliance on value stocks, which tends to perform best when growth is improving.

Russ Koesterich, CFA, is Head of Asset Allocation for BlackRock’s Global Allocation team and is a regular contributor to The Blog.

Copyright © Blackrock