Global Economic Outlook April 2016

by Carl R. Tannenbaum, Asha Bangalore, Victoria Marklew, Marshall Birkey, Ben Trinder, Brian Liebovich, Ankit Mital, Northern Trust

If you had somehow fallen asleep last New Year's Eve and awoken on March 31, you might not have realized that you'd slept through the first quarter. Economic prospects and market levels were little changed from point to point.

But that sense of stasis would be at odds with the tumult that characterized the first quarter of 2016. First came despair: the perception that policy makers had lost their edge sent forecasts and markets into a steep correction through the middle of February. Then came relief: a renewed sense of confidence returned to the outlook and allowed asset prices to recover.

While many are quite happy to signal an all-clear, a number of important uncertainties still bear close watching. Our central expectation continues to call for moderate global growth, but risks to the outlook will have to be carefully managed.

UNITED STATES

[Tweet "U.S. growth should rebound after a slow first quarter | Northern Trust"]

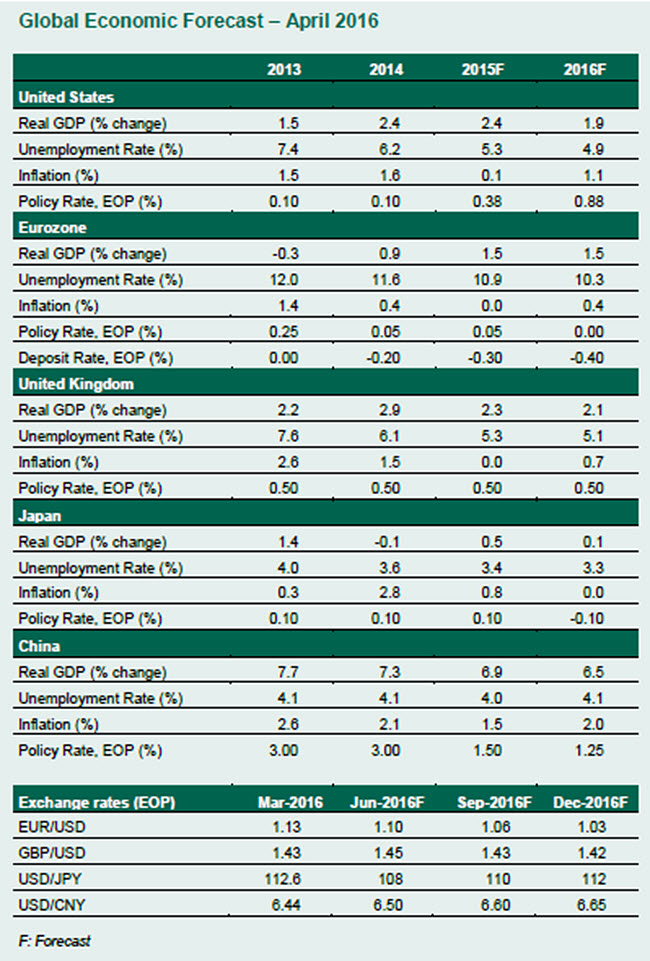

The United States experienced a soft economic patch in the first quarter, but the fundamentals are in place to support sustained growth in the rest of the year. Consumer spending and the housing sector are the drivers of growth. Business spending and exports are projected be a drag on economic activity, while government spending should add to growth. Core inflation, which excludes food and energy, is moving closer to the Federal Reserve's inflation target. Payroll employment continues to advance at an impressive clip and the unemployment rate is near the Fed's full employment mandate.

The United States experienced a soft economic patch in the first quarter, but the fundamentals are in place to support sustained growth in the rest of the year. Consumer spending and the housing sector are the drivers of growth. Business spending and exports are projected be a drag on economic activity, while government spending should add to growth. Core inflation, which excludes food and energy, is moving closer to the Federal Reserve's inflation target. Payroll employment continues to advance at an impressive clip and the unemployment rate is near the Fed's full employment mandate.

The Fed sees global economic and financial developments as a source of near-term risk, but these signals have improved since the Fed's last meeting. Continued forward momentum in the economy supports expectations of a higher policy rate at the June meeting. Recent Fed rhetoric echoes a similar view.

EUROZONE

[Tweet "recovery in eurozone growth continues to be steady, if unspectacular"]The recovery in eurozone growth continues to be steady, if unspectacular, with wide disparities in expansion levels between member states. Fiscal policy could potentially prove more expansionary this year, with more of a focus on structural deficits rather than headline levels. Domestic demand should support overall growth of 1.5%.

More eurozone employers expect an increase in employment than a decrease over the next 12 months, an encouraging sign. If the unemployment rate can continue its downward trajectory, it should average 10.3% this year. Again, rates will continue to vary among member states, with the French jobless rate likely remaining above that of the eurozone as a whole.

The inflation story remains fairly muted. The European Central Bank (ECB) expects price growth of just 0.1% this year and forward expectations in the marketplace are still well below the 2% target. However, a gradual upward trajectory in oil prices could raise the level a little higher. We predict a final yearly figure of 0.4%.

Credit condition surveys suggest that the ECB's current loose monetary policy stance is having a positive effect on the economy, albeit a small one. With this in mind, the ECB will likely stand pat this year to allow the full effect of its programs to take hold.

UNITED KINGDOM

[Tweet "The Brexit referendum looms large for and UK and the rest of Europe"] Our outlook for the United Kingdom is based on the assumption that voters will opt to remain in the European Union (EU) on June 23, the date of the Brexit referendum.

Our outlook for the United Kingdom is based on the assumption that voters will opt to remain in the European Union (EU) on June 23, the date of the Brexit referendum.

Real gross domestic product (GDP) growth continues to be dominated by the service sector and domestic demand remains healthy. Consumer spending has been strong, thanks to growing levels of real disposable income, supported by the low oil prices. This is expected to continue, although at a slightly moderated pace, leading to a forecasted expansion of 2.1% this year, among the strongest in the G7.

Unemployment is close to the best estimate of the natural rate, so the pace of improvement is expected to slow (indeed, latest figures show a small uptick in the number of unemployed); thus we expect a level of 5.1% for 2016. Recent increases in inflation were mostly seasonal, but for the first time surveys are pointing to consumers expecting prices to rise more quickly than recently observed. The Bank of England is not expected to move until 2017 at the earliest, given risks surrounding Brexit and ongoing global caution.

A clear downside risk to the forecast is the EU referendum. The first signs of uncertainty are starting to feed into the marketplace some businesses have reported delaying investment and hiring decisions. However, given a vote to stay, we would expect a catch up effect in the third and fourth quarters.

JAPAN

The much-vaunted Abenomics policy of trying to reflate the economy has run into some serious headwinds recently, causing us to downgrade our outlook for real GDP growth and inflation for this year. Prime Minister Abe and Bank of Japan (BoJ) Governor Kuroda have lobbied hard for corporations to award substantial pay increases in a bid to spur demand-pull inflation. But the combination of a strengthening yen and global uncertainty has kept the corporations concerned about future profitability, and less inclined to be generous with pay. The first quarter Tankan business confidence survey showed faltering confidence, softer investment intentions and expectations that corporate profits will decline across the board this year.

The much-vaunted Abenomics policy of trying to reflate the economy has run into some serious headwinds recently, causing us to downgrade our outlook for real GDP growth and inflation for this year. Prime Minister Abe and Bank of Japan (BoJ) Governor Kuroda have lobbied hard for corporations to award substantial pay increases in a bid to spur demand-pull inflation. But the combination of a strengthening yen and global uncertainty has kept the corporations concerned about future profitability, and less inclined to be generous with pay. The first quarter Tankan business confidence survey showed faltering confidence, softer investment intentions and expectations that corporate profits will decline across the board this year.

Meanwhile, household inflation expectations have been sliding in recent weeks and the BoJ has once again delayed its target date for getting the annual rate of inflation back up to 2.0%. Finally, the recent round of earthquakes and aftershocks on the southernmost island of Kyushu have disrupted manufacturing supply chains and will likely curb second quarter economic growth. All told, real GDP will struggle to expand at all this year and inflation will at best remain flat.

The BoJ has all but admitted that it is running out of options, with Kuroda reiterating that monetary policy alone cannot do all the heavy lifting. The BoJ's shift to a negative deposit rate in January has not been popular with the voters, and the positive effects of quantitative easing appear to be tapering off. Fiscal stimulus will likely come back to the fore in the coming weeks, particularly in the wake of the destruction on Kyushu. We also suspect that Abe will decide not to raise the nationwide sales tax from 8% to 10% in April 2017 as planned.

CHINA

A combination of regulatory measures to curb capital outflows and fiscal stimulus to spur domestic investment has helped ease the fears of many investors that the yuan would suffer a marked devaluation this year, or the economy a hard landing. Real GDP growth in the first quarter did ease back from the 6.9% recorded for 2015, but the year-over-year rate of 6.7% suggested there will be no nasty surprises as the government tries to rebalance the economy. Global commodity markets have duly stabilized in recent weeks, and export levels across the wider APAC region seem to have stopped falling.

However, a closer look at China's first quarter GDP data is less sanguine. The better-than-expected growth was largely the result of a massive increase in credit for housing, manufacturing and state-owned enterprises in general. Housing investment in particular picked up, but corporate investment weakened further. This recent real estate recovery is unlikely to be sustained through the rest of the year, given the stock of unsold housing inventory outside the largest cities.

However, a closer look at China's first quarter GDP data is less sanguine. The better-than-expected growth was largely the result of a massive increase in credit for housing, manufacturing and state-owned enterprises in general. Housing investment in particular picked up, but corporate investment weakened further. This recent real estate recovery is unlikely to be sustained through the rest of the year, given the stock of unsold housing inventory outside the largest cities.

The authorities have vowed to curb excess capacity in certain sectors and to steer the economy away from a reliance on debt-fueled production for exports and toward domestic consumption. However, they also seem unwilling to countenance the short-term economic pain that such a rebalancing implies. We can therefore expect to see continued fiscal stimulus measures through the year, as the economy heads toward the official growth target of 6.5%. This will be the slowest annual pace since 1990, but arguably still too fast for an economy that is trying to rebalance.

Copyright Northern Trust