by Steve Blumenthal, Capital Market Group

December 23, 2016

“Stay wary, alert and very, very nimble.”

– Art Cashin

Managing Director, UBS Financial Services

I read Art’s letter almost every day and, boy, do I enjoy his wit, his compassion and his brains. In the spirit of Christmas, his post this morning was fun.

‘Tis three days before Christmas

and at each brokerage house

The only thing stirring

was the click of a mouse

Down on the Exchange

the tape inches along

Brokers bargained and traded

as they hummed an old song

The Fed turned data dependent

or so they would claim

Yet they hiked in December

though the data looked tame

He touched on the Cubs, the Broncos and LeBron… my favorite part was:

Don’t let this year’s problems

impede Christmas Cheer

Resolve to be happy

throughout the New Year

And resist ye Grinch feelings

let joy never stop

Put the bad at the bottom

keep the good on the top

So count up your blessings

along with your worth

You’re still living here

in the best place on earth

And think ye of wonders

that light children’s eyes

And hope Santa will bring you

that Christmas surprise

With joy on our minds and hope in our hearts, let us step forward and not let the bond market tear us apart. Sorry about that… Art’s jingle is in my head.

I’m on record saying the low in bonds is IN. I continue to believe we are entering a phase of rising interest rates. In such environments, bonds perform poorly. It’s starting to get dicey globally and the evidence is showing up in the bond market. Let’s see what is going on that may or may not be fully “on your radar.” This from Wolf Richter, founder of Wolf Street:

“All kinds of things are now happening in the world of bonds that haven’t happened before. For example, authorities in China today halted trading for the first time ever in futures contracts of government bonds, after prices had swooned, with the 10-year yield hitting 3.4%. Trading didn’t resume until after the People’s Bank of China injected $22 billion into the short-term money market.

What does this turmoil have to do with US Treasurys? China has been dumping them to stave off problems in its own house….”

The move won’t be straight up though it has felt that way over the last few months. If you are long government bonds (including longer-dated municipals), my two cents is to use rallies (declines in interest rates) to shorten your maturity exposures.

The biggest bubble of all bubbles sits in the government bond market. Particularly in the developed world… here, there and everywhere. Governments’ choices? Inflate the problem away, raise taxes, and sell assets or default. Or all of the above. Right now it is inflate and seek growth. Currency gamesmanship or more pointedly “currency wars” steps into the fray. The imbalances are great.

I believe we will see a sovereign debt default first in Europe. The EU is improperly bolted together and protectionism is on the rise. Brexit is a sign. The U.S. election is a sign. The Italian Referendum is a sign. And we are seeing serious problems with government debt emerge outside of the U.S.

The European Central Bank now owns 15% of Germany’s national debt. Much of it at negative yields. The ECB remains on its bond buying spree though they are running out of positive yielding bonds to buy.

Further, the ECB is buying up the troubled debt from the books of the troubled banks and there appears to be a long way to go. Troubled isn’t just the higher risk junk bond corporate bets, trouble are the sovereign government bonds from Greece, Italy, Portugal and Spain. I can’t help but think we will one day look back and reflect on just how surreal, crazy, insane this period turned out to be.

Here in the U.S. the Fed now owns $2.4 trillion of the roughly $20 trillion in U.S. government debt. In Japan, retirees are no longer buying Japanese government bonds. When Abe came to power, the private sector held 177% of the debt-to-GDP. They now own approximately 75%. The citizens are selling. The BoJ steps in — print and buy… the Bank of Japan owns more of the debt than the private sector. Print and buy… the Japanese Central Bank owned 60% of the nation’s ETFs as of June 2016.

See Bloomberg’s The Bank of Japan’s Unstoppable Rise to Shareholder No. 1

In 2016, Japan joined Europe in the great experiment of modern monetary policy: negative interest rates to spur inflation. Will it work? In the short term, yes; in the long term, I don’t think so.

That’s the bet you and I are faced with. With rates still near 5,000-year lows, the risk reward makes zero sense to me. We are dependent on central bankers. I’m nervous.

OK… as depressing as that sounds, it need not be. There is an upside and it is this: I believe we are heading towards an investment opportunity of a lifetime. To get there, play more defense than offense. Look at valuation levels, look at the age of the bull market move. Have a plan in place to risk protect what you’ve got. I favor trend following and for now the equity market trend remains bullish.

Participate and protect and keep the great Sir John Templeton in the back of your mind. The single best advice I ever received was in 1985. Mr. Templeton told me (and of course many others many times since) that the secret to his success was he was able to: “[b]uy when everyone else was selling and sell when everyone else was buying.”

Watch out for over confidence, don’t follow the masses. This is a game of opposites. Don’t fall into the buy-and-hold forever trap. Most can’t do it. Put stop-losses in place. Use the 200-day moving average rule to stop-loss protect your equity exposure and/or buy 15% out-of-the money put options to hedge your exposure.

Further, watch what is going on in Europe. Watch China, watch Japan. Debt is the global issue. All are trying to grow out of the mess. Odds are rough. The U.S. is by no means healthy from a debt-to-GDP perspective, but we look to be the cleanest shirt in the laundry pile.

When confidence in governments is lost, the money will run to where it is treated best. That is likely to be U.S. stocks. A melt up in prices and valuations? Maybe. I hope so but I’m going to make sure I am risk minded along the way.

Heat up that coffee and find your favorite chair. I’ve included a Pension Fund Red Ink chart for you this week so you can see just how underfunded your particular state is (most recent available data). Also, keep what is happening in the U.S. Treasury bond market front of mind. You’ll find a great article (charts) to that end below.

Most importantly, celebrate your family, hug your kids and take an extra second to send some love to the world. Please know how grateful I am that you take time to read my commentary each week.

Merry Christmas and Happy Holidays to you and those you love most! I’m going to take the week off next week and recharge for the New Year. There will be no On My Radar next Friday.

♦ If you are not signed up to receive my weekly On My Radar e-newsletter, you can subscribe here. ♦

Included in this week’s On My Radar:

- Pension Fund Red Ink – Check Out Your State (Chart)

- Foreigners are Dumping Treasury Bonds at Record Rate

- The Year in Review

- Trade Signals – Strong Dollar, Weak Gold, Equity Trend Up, Bond Trend Down, Sentiment Remains Far Too Optimistic

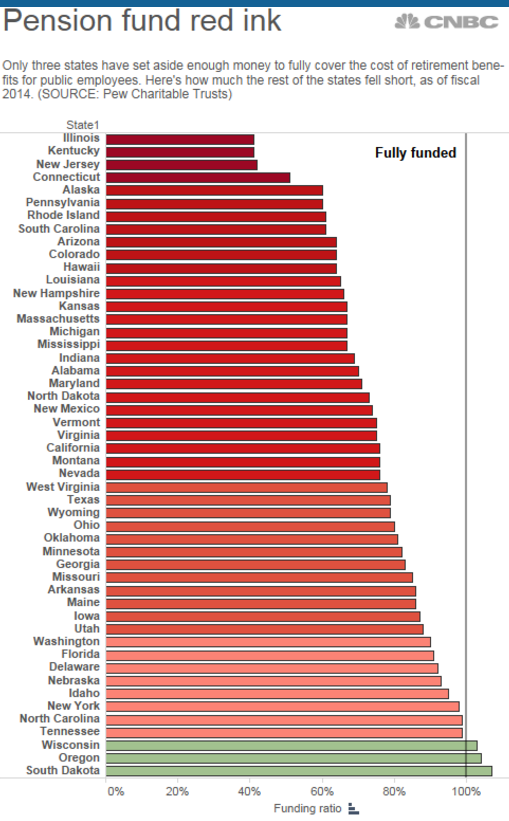

Pension Fund Red Ink

Last week I shared with you that the California Public Employees Retirement System, better known as CalPERS, stated that a 7.5% annual return is no longer realistic. To which I added, finally, amen, right on. The new actuarial target is 7%. That still seems high to me.

Forward 10-year probable returns for equities are in the 3% to 4% range. Hussman is projecting negative 12-year coming returns. Jeremy Grantham and his team at GMO sees seven-year coming returns even lower. Note the -3% real returns for large cap stocks and -2.3% for small cap stocks (real means returns after inflation).

And with bonds yielding 2.5%? Bonds will get us 2.5% over the coming 10 years. Timber and Emerging Markets at 4.4%.

The headwind to that now 7% actuarial return target? High valuations and low yields. Unless the pension funds are the world’s greatest market timers, which they are not, 7% is not going to happen.

I believe 5% to 6% is doable. Smart beta and other factor-based ETFs. But hedge your equity exposure as a lot of the ammo in the central bank arsenal has been spent. The next recession, and it’s coming, will be more challenging that most. Too, the largest recession driven corrections occur when your starting point is one of excessively high valuations.

With valuations at the second highest in history, it is wise to play defense now and get more aggressive later. In the meantime… patience.

As I reread last week’s piece, I found myself upset with myself for not sharing this next chart.

To that end, I was curious about my state and you may be curious about yours. I’ll be talking to Susan about moving to Florida before Pennsylvania hikes the tax rate…

Here’s a look:

From CNBC:

After years of not setting aside enough money, state pension funds are looking at a $1 trillion shortfall in what they owe workers in benefits, according to a new analysis from The Pew Charitable Trusts.

Pennsylvania is sitting at approximately 68% funded. The sixth worst state in the Union. Illinois and Kentucky are near 45% funded.

This is a mess, my friend. And it is worse than the above chart reflects. Recall from last week’s piece that CalPERS lowered their return assumptions from 7.5% to 7%. The underfunded numbers above are using 2014 return assumptions. Lower the return assumptions and the underfunded problem grows worse.

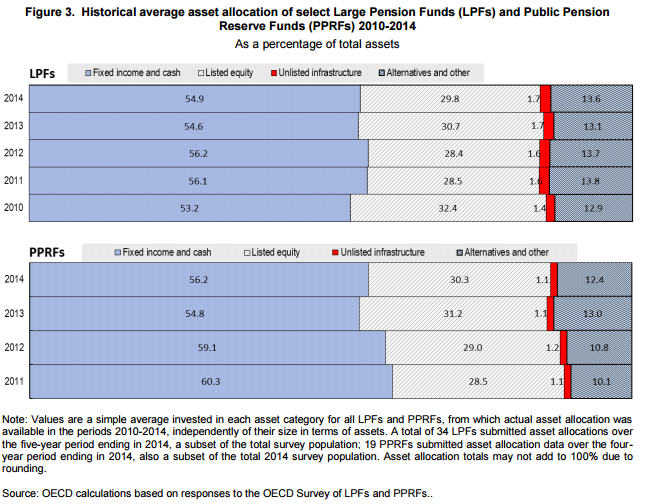

Note in the next chart that at the end of 2014, 54.9% in the fixed income and cash allocation bucket has not done so well YTD.

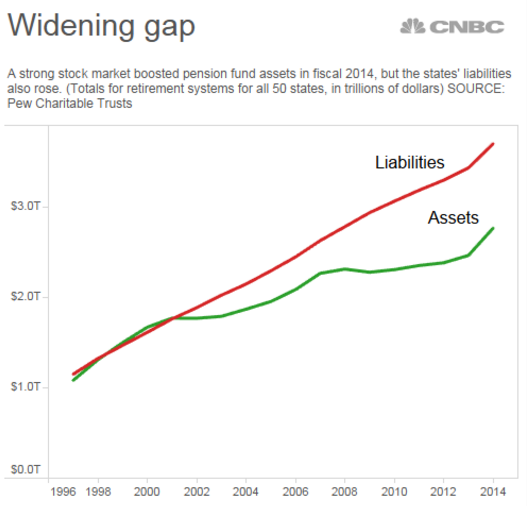

Widening gap: The data in the next chart is through fiscal year 2014. The funding gap is expected to top $1 trillion in fiscal 2015 (we’ll get that number soon). Further, with an estimated 55% in bonds, 30% in stocks and 15% in alts, my back of the napkin math looks like a 5% 2016 return year for pensions.

That bond portion of pension portfolios has been hit hard while the stock portion has gained approximately 10%. So take 55% of the 2.19% YTD return for “BND” (Vanguard Total Bond Market ETF), 30% of 9.77% for “SPY” (SPDR S&P 500 ETF) and 15% of 7% (a rough estimate for alternative investments) and you get roughly 5%.

All in, it’s a pretty safe guess that the funding shortfall is higher today than it was in 2014. The aging population and returns under the 7.5% actuarial targets are the culprits. Expect higher taxes in the more troubled states.

One last chart on the subject:

A ranking of the 50 states and Puerto Rico based on their fiscal solvency in five separate categories:

- Cash solvency. Does a state have enough cash on hand to cover its short-term bills?

- Budget solvency. Can a state cover its fiscal year spending with current revenues, or does it have a budget shortfall?

- Long-run solvency. Can a state meet its long-term spending commitments? Will there be enough money to cushion it from economic shocks or other long-term fiscal risks?

- Service-level solvency. How much “fiscal slack” does a state have to increase spending if citizens demand more services?

- Trust fund solvency. How much debt does a state have? How large are its unfunded pen-sion and healthcare liabilities?

Source: Mercatus Center at George Mason University

Everyone is Dumping Treasurys

All kinds of things are now happening in the world of bonds that haven’t happened before. For example, authorities in China today halted trading for the first time ever in futures contracts of government bonds, after prices had swooned, with the 10-year yield hitting 3.4%. Trading didn’t resume until after the People’s Bank of China injected $22 billion into the short-term money market.

What does this turmoil have to do with US Treasurys? China has been dumping them to stave off problems in its own house….

The US Treasury Department released its Treasury International Capital data for October, and what it said about the dynamics of Treasury securities is a doozy of historic proportions.

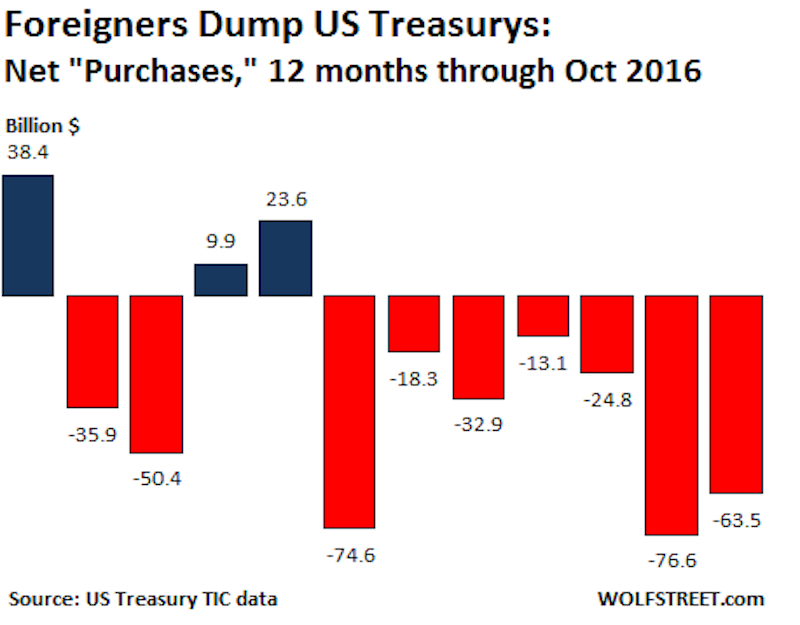

Net “acquisitions” of Treasury bonds and notes by “private” investors amounted to a negative $18.3 billion in October, according to the TIC data. In other words, “private” foreign investors sold $18.3 billion more than they bought. And “official” foreign investors, which include central banks, dumped a net $45.3 billion in Treasury bonds and notes. Combined, they unloaded $63.5 billion in October.

In September, these foreign entities had already dumped a record $76.6 billion. They have now dumped Treasury paper for seven months in a row. Over the past 12 months through October, they unloaded $318.2 billion:

A 12-month selling spree of this magnitude has never occurred before. There have been a few months of timid net selling in 2012, and some in 2013, and a few in 2014, but no big deal because the Fed was buying under its QE programs. But then, with QE tapered out of the way, the selling picked up in 2015, and has sharply accelerated in 2016.

This chart (via Trading Economics), going back to the early 1980s, shows just how historic this wholesale dumping (circled in red) of US Treasury bonds and notes by foreign entities has been:

The chart is particularly telling: It shows in brutal clarity that foreign buyers funded the $1 trillion-and-over annual deficits during and after the Financial Crisis, with net purchases in several months exceeding $100 billion. The other big buyer was the Fed.

But since last year, the world has changed. China, once the largest holder of US Treasurys, has been busy trying to keep a lid on its own financial problems that are threatening to boil over. It’s trying to prop up the yuan. It’s trying furiously to stem rampant capital flight. It’s trying to keep its asset bubbles, particularly in the property sector, from getting bigger and from imploding – all at the same time. And in doing so, it has been selling foreign exchange reserves hand over fist.

According to the TIC data (market price adjusted), China was the largest seller in October, unloading $41 billion. Over the last six months, it unloaded $128 billion. This slashed its holdings of Treasury securities to $1.116 trillion, below the holdings of Japan. Japan, now the largest holder of Treasury securities, reduced its holdings by $4.5 billion in October to $1.132 trillion.

Japan and China are by far the largest two creditors of the US – the US still owes them $2.25 trillion – and they’re cutting back their lending.

But who’s buying this paper? For every seller, there must be a buyer. But when demand sags, sellers have to offer a better deal. So they have to cut the price – for buyers, it means that the yield rises and becomes more attractive. The yield of the 10-year Treasury has nearly doubled since July this year, settling today at 2.60%:

At this yield, Treasurys found buyers today. But the remaining buyers – now that the biggest holders have turned into sellers – may demand even higher yields in the future. This comes on top of a lot of new supply: Over the last 24 months, the US gross national debt has ballooned by $1.85 trillion, or by about $925 billion per 12-month period (using the two-year average eliminates the distortions of the debt ceiling fight). Soon, the US gross national debt will hit $20 trillion.

And given President-Elect Trump’s ambitious deficit-spending and tax-cut programs, a lot more debt may soon wash over the market. But this time, neither China nor Japan, nor the other major foreign entities may be willing and able to bail out the US, as they’ve done during and after the Financial Crisis. The bond market sees this too. Hence, the bloodletting in Treasurys, considered among the most conservative investments in the world.

Source: Business Insider. Read the original article on Wolf Street. Copyright 2016. Follow Wolf Street on Twitter.

The Year in Review — Choppy

In early November, the two-year return on the S&P 500 Index stood at just 3%. Then the election and the post Trump rally.

- Stocks gyrated much the year after selling off hard December 2015 through February 2016 before climbing to record highs this month, the dollar soared and bond prices fell.

- Recall the December 2015 Fed rate increase? That December 2015 Federal Reserve rate increase along with expected further hikes set fear in place that the U.S. would be headed into recession.

- January began with a panic. By February 11, the Dow Jones Industrials was down more than 10%, and New York oil futures fell to $26.21 a barrel.

- China was next to step center stage. Investors feared China faced a “hard landing” after years of rapid growth. China adjusted their currency and the market took note.

The fear receded by March after the ECB, Bank of Japan, China and the Fed met in Shanghai and arrived at a temporary “currency truce” understanding.

- Central bank policy makers spoke up and market calm returned.

- Japan joined Europe in the great experiment of modern monetary policy: negative interest rates to spur inflation.

- The Bank of Japan’s embrace of negative interest rates also signaled bad news for the global economy. Negative rates would later spread to much of Europe.

- Call it Keynesian craziness.

- The Brexit surprise followed on June 23.

- S. bond yields made what may be a 35-year low in early July. The 10-year hit 1.36% and sits at over 2.55% today. It is not your father’s bond market.

- Trump surprised in November. The people feel underserved and frankly fed up with government.

- The year closed with a party, as Wall Street bet a Donald Trump administration would end the era of ultralow interest rates and spark higher U.S. growth and inflation.

- Through the November election, it was a choppy, trendless and overall challenging for momentum-based trading. Post-election, a better trend environment appears to have returned.

Source: WSJ

As we move into 2017, keep Paul Tudor Jones’ sage advice in the back of your head, “The whole trick in investing is: “How do I keep from losing everything?”

Trade Signals – Strong Dollar, Weak Gold, Equity Trend Up, Bond Trend Down, Sentiment Remains Far Too Optimistic (posted 12-21-2016)

S&P 500 Index — 2,267 (12-21-16)

Posted each Wednesday, Trade Signals looks at several of my favorite stock, investor sentiment and bond market indicators. It is my weekly risk management dashboard, designed to keep me better in sync with the major technical trends. I hope you find the information helpful in your work.

Summary

Bullish investor sentiment for stocks recently peaked at 83%. That is a high reading and signals caution for stock investors. It was at 14% bullish on November 3, 2016. Readings below 41.5% indicate a high level of investor pessimism. Readings above 62.5% indicate a high level of investor optimism.

It looks something like this:

- Extreme Pessimism is short-term bullish for equities

- Extreme Optimism is short-term bearish for equities

(See the Investor Sentiment charts below)

Sentiment can help with timing your buying decisions. Overall trend based evidence can help you identify bull and bear market cycles. The trend for equities remains bullish. The trend for bonds bearish and the trend for gold remains bearish.

Today’s bullish sentiment suggests caution. I find myself in the “buy the Trump dip” mindset and advise to use the 200-day moving average line on equity positions to set stops losses. And/or diversify to a handful of go anywhere ETF trading strategies.

Valuations are high, yields are low. Risk remains high.

Click here for the most recent Trade Signals blog.

Personal Note

I had a wonderful dinner with a dear friend, Tom Giachetti, last evening and my new friend Josh. The food was outstanding. I met Tom in 1992 when my father Marv and I were looking to set up the business. Dad went to a conference and by coincidence sat next to Tom. Tom looked at Marv and told him to save his seat. A few seconds later, Tom stood on stage and addressed the crowd. A wannabe stand-up comedian who actually makes SEC compliance kind of fun. And that’s hard to do.

When Tom sat back down, Marv looked at him and said. “Tom, I think we need to talk.” Tom put us into business and we have worked closely ever since. On my way to the airport to pick up my son I couldn’t help but feel how grateful I am for Tom. Thank you, my friend. I appreciate our friendship far more than our business relationship but do know I sleep so much better at night because of you.

Call a friend and let him/her know you love him/her. You’ll feel good and so will they. An Italian dinner with my Italian friend. A good time.

Susan and I will be at home this Christmas. My only want for is our time together. A fire, a big dinner and all eight of us at the table – and a nice glass of red wine. Susan’s mother Pat is joining us for a few days next week. What a grandma! She is such great fun.

I’ll be in Colorado on January 8-11, at the Inside ETFs 2017 Conference in Hollywood, Florida on January 22-25 and in Utah in mid-February. At the Inside ETFs Conference, I will be presenting on gold (which is in a confirmed downtrend – I’ll share a few ideas on how to trade gold). If you are planning on attending, please let me know. I’d love to grab a coffee or better yet a good beer with you.

Wishing you an abundance of love, joy, health and wealth!

Merry Christmas and Happy Holidays to you and all those you love most.

There will be no On My Radar next Friday. The plan is to take it easy next week and regroup for the New Year. So Happy New Year to you as well…

If you find the On My Radar weekly research letter helpful, please tell a friend … also note the social media links below. I often share articles and charts via Twitter that I feel may be worth your time. You can follow me @SBlumenthalCMG.

♦ If you are not signed up to receive my weekly On My Radar e-newsletter, you can subscribe here. ♦

With kind regards,

Steve

Stephen B. Blumenthal

Executive Chairman & CIO

CMG Capital Management Group, Inc.

Stephen Blumenthal founded CMG Capital Management Group in 1992 and serves today as its Executive Chairman and CIO. Steve authors a free weekly e-letter entitled, “On My Radar.” Steve shares his views on macroeconomic research, valuations, portfolio construction, asset allocation and risk management.

The objective of the letter is to provide our investment advisors clients and professional investment managers with unique and relevant information that can be incorporated into their investment process to enhance performance and client communication.

Click here to receive his free weekly e-letter.

Social Media Links:

CMG is committed to setting a high standard for ETF strategists. And we’re passionate about educating advisors and investors about tactical investing. We launched CMG AdvisorCentral a year ago to share our knowledge of tactical investing and managing a successful advisory practice.

You can sign up for weekly updates to AdvisorCentral here. If you’re looking for the CMG white paper, “Understanding Tactical Investment Strategies,” you can find that here.

AdvisorCentral is being updated with new educational resources we look forward to sharing with you. You can always connect with CMG on Twitter at @askcmg and follow our LinkedIn Showcase page devoted to tactical investing.

A Note on Investment Process:

From an investment management perspective, I’ve followed, managed and written about trend following and investor sentiment for many years. I find that reviewing various sentiment, trend and other historically valuable rules-based indicators each week helps me to stay balanced and disciplined in allocating to the various risk sets that are included within a broadly diversified total portfolio solution.

My objective is to position in line with the equity and fixed income market’s primary trends. I believe risk management is paramount in a long-term investment process. When to hedge, when to become more aggressive, etc.

IMPORTANT DISCLOSURE INFORMATION

Investing involves risk. Past performance does not guarantee or indicate future results. Different types of investments involve varying degrees of risk. Therefore, it should not be assumed that future performance of any specific investment or investment strategy (including the investments and/or investment strategies recommended and/or undertaken by CMG Capital Management Group, Inc. or any of its related entities (collectively “CMG”) will be profitable, equal any historical performance level(s), be suitable for your portfolio or individual situation, or prove successful. No portion of the content should be construed as an offer or solicitation for the purchase or sale of any security. References to specific securities, investment programs or funds are for illustrative purposes only and are not intended to be, and should not be interpreted as recommendations to purchase or sell such securities.

Certain portions of the content may contain a discussion of, and/or provide access to, opinions and/or recommendations of CMG (and those of other investment and non-investment professionals) as of a specific prior date. Due to various factors, including changing market conditions, such discussion may no longer be reflective of current recommendations or opinions. Derivatives and options strategies are not suitable for every investor, may involve a high degree of risk, and may be appropriate investments only for sophisticated investors who are capable of understanding and assuming the risks involved. Moreover, you should not assume that any discussion or information contained herein serves as the receipt of, or as a substitute for, personalized investment advice from CMG or the professional advisors of your choosing. To the extent that a reader has any questions regarding the applicability of any specific issue discussed above to his/her individual situation, he/she is encouraged to consult with the professional advisors of his/her choosing. CMG is neither a law firm nor a certified public accounting firm and no portion of the newsletter content should be construed as legal or accounting advice.

This presentation does not discuss, directly or indirectly, the amount of the profits or losses, realized or unrealized, by any CMG client from any specific funds or securities. Please note: In the event that CMG references performance results for an actual CMG portfolio, the results are reported net of advisory fees and inclusive of dividends. The performance referenced is that as determined and/or provided directly by the referenced funds and/or publishers, have not been independently verified, and do not reflect the performance of any specific CMG client. CMG clients may have experienced materially different performance based upon various factors during the corresponding time periods.

The CMG Tactical Fixed Income Index and CMG Tactical All Asset Index are rules-based indexes that reflect the theoretical performance an investor would have obtained had it invested in the manner shown and do not represent actual returns, as investors cannot invest directly in the Indexes. The CMG Tactical Fixed Income Index and CMG Tactical All Asset Index returns represented do not reflect the actual trading of any client account. No representation is being made that any client will or is likely to achieve results similar to those presented herein. The CMG Tactical Fixed Income Index performance results are presented net of a 2.50% maximum annual fee deducted from the account balance quarterly, in arrears.

Any financial product based on the CMG Tactical Fixed Income Index, CMG Tactical All Asset Index or any index derived therefrom that is offered by CMG Capital Management Group, Inc. is not sponsored, endorsed, sold or promoted by Solactive AG and Solactive AG makes no representation regarding the advisability of investing in the product.

Mutual funds involve risk including possible loss of principal. An investor should consider the fund’s investment objective, risks, charges, and expenses carefully before investing. This and other information about the CMG Tactical All Asset Strategy FundTM, CMG Global Equity FundTM, CMG Tactical Bond FundTM, CMG Global Macro Strategy FundTM and the CMG Long/Short FundTM is contained in each fund’s prospectus, which can be obtained by calling 1-866-CMG-9456 (1-866-264-9456). Please read the prospectus carefully before investing. The CMG Tactical All Asset Strategy FundTM, CMG Global Equity FundTM, CMG Tactical Bond FundTM, CMG Global Macro Strategy FundTM and the CMG Long/Short FundTM are distributed by Northern Lights Distributors, LLC, Member FINRA.

NOT FDIC INSURED. MAY LOSE VALUE. NO BANK GUARANTEE.

Hypothetical Presentations: To the extent that any portion of the content reflects hypothetical results that were achieved by means of the retroactive application of a back-tested model, such results have inherent limitations, including: (1) the model results do not reflect the results of actual trading using client assets, but were achieved by means of the retroactive application of the referenced models, certain aspects of which may have been designed with the benefit of hindsight; (2) back-tested performance may not reflect the impact that any material market or economic factors might have had on the adviser’s use of the model if the model had been used during the period to actually manage client assets; and (3) CMG’s clients may have experienced investment results during the corresponding time periods that were materially different from those portrayed in the model. Please Also Note: Past performance may not be indicative of future results. Therefore, no current or prospective client should assume that future performance will be profitable, or equal to any corresponding historical index. (e.g., S&P 500® Total Return or Dow Jones Wilshire U.S. 5000 Total Market Index) is also disclosed. For example, the S&P 500® Total Return Index (the “S&P 500®”) is a market capitalization-weighted index of 500 widely held stocks often used as a proxy for the stock market. S&P Dow Jones chooses the member companies for the S&P 500® based on market size, liquidity, and industry group representation. Included are the common stocks of industrial, financial, utility, and transportation companies. The historical performance results of the S&P 500® (and those of or all indices) and the model results do not reflect the deduction of transaction and custodial charges, nor the deduction of an investment management fee, the incurrence of which would have the effect of decreasing indicated historical performance results. For example, the deduction combined annual advisory and transaction fees of 1.00% over a 10-year period would decrease a 10% gross return to an 8.9% net return. The S&P 500® is not an index into which an investor can directly invest. The historical S&P 500® performance results (and those of all other indices) are provided exclusively for comparison purposes only, so as to provide general comparative information to assist an individual in determining whether the performance of a specific portfolio or model meets, or continues to meet, his/her investment objective(s). A corresponding description of the other comparative indices, are available from CMG upon request. It should not be assumed that any CMG holdings will correspond directly to any such comparative index. The model and indices performance results do not reflect the impact of taxes. CMG portfolios may be more or less volatile than the reflective indices and/or models.

Certain information contained herein has been obtained from third-party sources believed to be reliable, but we cannot guarantee its accuracy or completeness.

In the event that there has been a change in an individual’s investment objective or financial situation, he/she is encouraged to consult with his/her investment professional.

Written Disclosure Statement. CMG is an SEC-registered investment adviser located in King of Prussia, Pennsylvania. Stephen B. Blumenthal is CMG’s founder and CEO. Please note: The above views are those of CMG and its CEO, Stephen Blumenthal, and do not reflect those of any sub-advisor that CMG may engage to manage any CMG strategy. A copy of CMG’s current written disclosure statement discussing advisory services and fees is available upon request or via CMG’s internet web site at www.cmgwealth.com/disclosures.