by Richard Bernstein, Richard Bernstein Advisors (Janus Henderson)

What if the debt crisis investors have feared is not still ahead, but already here, unfolding in plain sight? In his June insight, Richard Bernstein, Global Head of Macro & Customized Investing, makes the case that the market may already be penalizing U.S. fiscal excess, not through a dramatic collapse, but through a slow burn with real consequences for investors and the broader economy.

The old saying is that a frog will jump out of a pot of boiling water but will sit and cook if one turns up the heat slowly. The idea is that slow, insidious temperature increases go unnoticed relative to massive shocks.

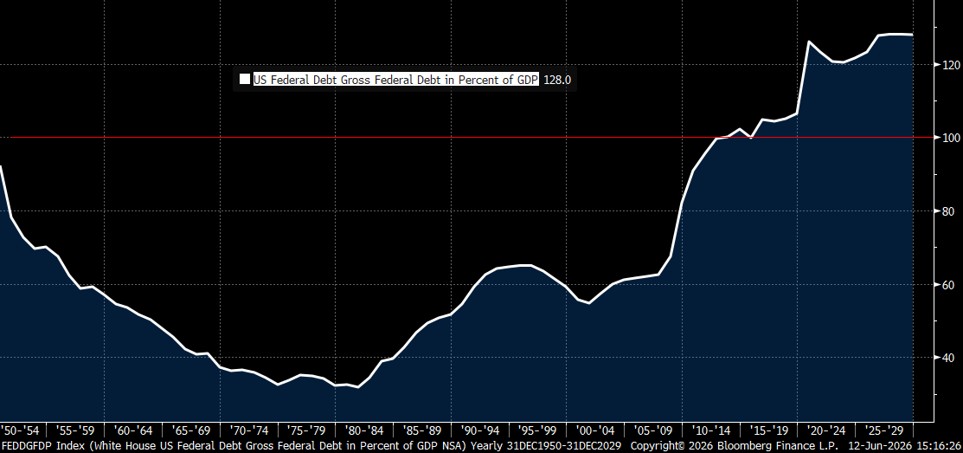

Some investors have been worried for years about a day of reckoning for U.S. debt. Consensus has been that investors will wake up one day and the financial market will be unwilling to hold the ever-increasing amount of U.S. government debt (Exhibit 1).

Exhibit 1: U.S. federal debt as a percent of GDP (Dec. 1950 – Dec. 2025, with projected ratio to Dec. 2029)

Source: RBA/JHI, Bloomberg Finance L.P.

The day of reckoning analogy seems wrong to us. In our view, the markets have been slowly penalizing the U.S. for its fiscal imprudence. The U.S. economy has been punished for more than a decade (importantly, through both Democratic and Republican administrations). The result is that corporations, municipalities, and individuals have been paying higher interest rates than they otherwise might have paid.

An economy doesn’t quickly become uncompetitive, and the added interest expense the private sector has had to pay relative to similar borrowers in other countries has almost certainly contributed to the U.S.’s gradual loss of productive market share.

There is no boiling pot of water that will cause the U.S. to suddenly realize its mistake. Rather, the markets are slowly turning up the heat.

The U.S. isn’t AAA rated anymore

Regardless of whether a borrower is a country, a company, or an individual, lenders charge higher interest rates to lower-quality, riskier borrowers to offset the risk of potential delinquencies or default.

Investors price lower-quality bonds so the bonds have higher yields to compensate for the additional risk. Generally, AAA rated bonds would have lower yields than BBB rated bonds, which in turn would have lower yields than junk bonds.

Individuals’ borrowing is not rated by an agency but by FICO score or VantageScore rating. Lower scores denote riskier borrowers, and those borrowers’ higher rates offset the perceived increased risk of default.

Although 2011’s initial downgrade of U.S. government debt from AAA was treated by many as a non-event, the markets almost immediately began to re-price U.S. debt as riskier relative to countries that maintained AAA ratings.

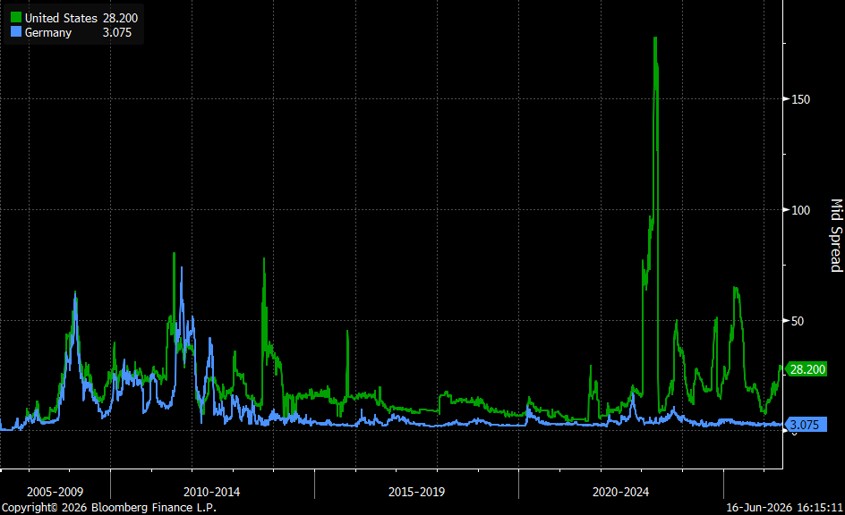

Exhibit 2 shows the spread between the U.S. 10-year Treasury and German 10-year notes. German bonds were priced as riskier (i.e., higher yields) in the early portion of the chart because of the spending that was anticipated for reunification between East and West Germany. After that period, the yields of U.S. and German bonds fluctuate back and forth.

However, U.S. bonds began to trade at consistently higher yields once the U.S. was downgraded. German bonds are still rated AAA and continue to offer lower yields than Treasuries (i.e., borrowing costs for the German government are lower than that of the U.S. government).

Exhibit 2: U.S. vs. Germany: 10-year government bond spreads (10 Aug. 1988 – 12 Jun. 2026)

Source: RBA/JHI, Bloomberg Finance L.P.

One could argue that there are many reasons why spreads could be wider, but the credit default swap (CDS) market has also priced U.S. Treasuries as incrementally risky. (A CDS is a hedge against default, and CDS spreads are measured in basis points.)

Exhibit 3 shows one-year CDS spreads for U.S. and German debt. Like the earlier spread chart, CDS spreads are roughly similar between the two countries. However, CDS spreads on US debt are marginally higher after the ratings downgrade and has never been lower than Germany’s since that downgrade.

Exhibit 3: U.S. vs. Germany: 1-year CDS spreads (28 Sep. 2006 – 16 Jun. 2026)

Source: RBA/JHI, Bloomberg Finance L.P.

De facto versus de jure “risk-free rate”

The U.S. Treasury market is the deepest and most liquid bond market in the world, and, as such, is often considered to set the “risk-free rate”. U.S. Treasuries were for decades both the de facto and de jure “risk-free rate” for global assets. That isn’t quite true anymore.

Because of the breadth and depth of the U.S. Treasury market versus the bond markets of AAA rated countries, the U.S. Treasury has remained the de facto “risk-free rate”. However, it has lost its status as the de jure “risk-free rate”: Many other countries are rated AAA and are considered less risky than the U.S.

Exhibit 4 (compiled by xAI) shows the credit ratings and 10-year yields of AAA rated countries versus the U.S. Eight of the nine AAA rated countries presently borrow at yields lower than the US.

Exhibit 4: U.S. vs. AAA rated countries (as of 12 Jun. 2026)

CountryS&P Rating10Y YieldSpread vs. US 10Y (bp)SwitzerlandAAA0.40%-408 bpSingaporeAAA2.02%-246 bpSwedenAAA2.84%-164 bpDenmarkAAA2.89%-159 bpGermanyAAA2.99-3.00%-148 bpNetherlandsAAA3.11%-137 bpCanadaAAA3.41%-107 bpNorwayAAA~4.37%~-90 bpAustraliaAAA4.82%+35 bpUnited StatesAA+4.46-4.48%Benchmark (0 bp)

Primary data source: Worldgovernmentbonds.com (updated June 12, 2026, cross-checked with Trading Economics and Bloomberg.

The entire U.S. economy has suffered

Sovereign debt in most developed markets is generally considered safer than private-sector debt. Because private-sector yields are based on government yields plus a risk premium, an increase in sovereign debt yield accordingly translates to higher borrowing costs for the private sector.

The downgrade of U.S. debt and the resulting higher government borrowing costs has translated into higher borrowing costs for the entire U.S. economy.

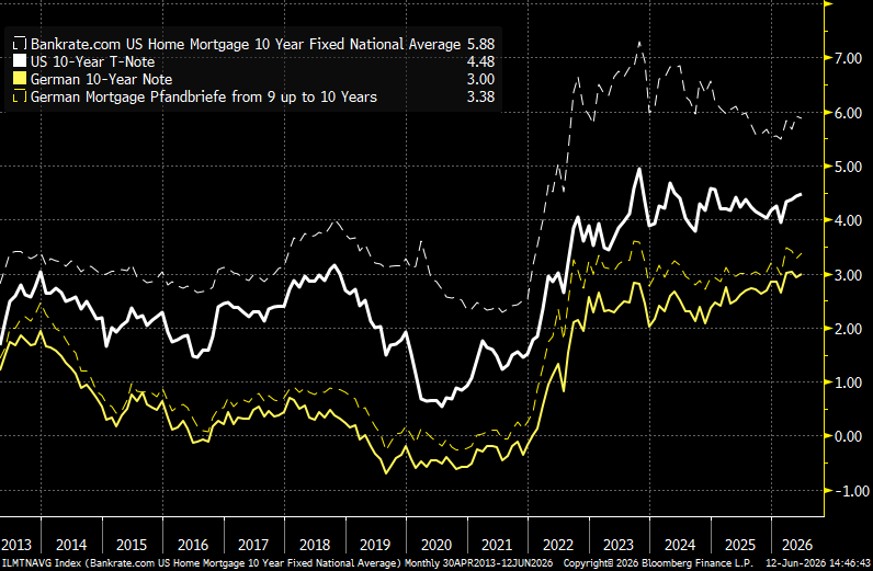

Exhibit 5 compares mortgage rates in the U.S. to those in Germany. Admittedly, these comparisons do not use totally comparable mortgage data, but the story remains important. Mortgage rates in both countries are, of course, higher than government debt yields because individuals are not as creditworthy as the government.

However, mortgage rates in Germany are lower than mortgage rates in the U.S. because U.S. mortgages are based on the yield of the U.S. 10-year Treasury, which has a higher yield than Germany’s 10-year bund.

Whether this chart represents a perfect comparison or not misses the point. The chart does reflect higher borrowing costs in the U.S. because of higher Treasury yields, which are directly related to Washington’s fiscal imprudence.

The entire U.S. economy has been paying a penalty.

Exhibit 5: U.S. vs. Germany: Mortgage rates (30 Apr. 2013 – 12 Jun. 2026)

Source: RBA/JHI, Bloomberg Finance L.P.

The frog had a spine

When a company is in financial trouble, a standard route to repair the damage includes increasing revenues and cutting costs. Unless the U.S. actively decides to follow the path of an emerging market and fosters inflation to alleviate debt issues, the standard route to improve the nation’s balance sheet will be increasing revenue and cutting costs.

However, both Democrats and Republicans refuse to admit this reality. Republicans refuse to raise taxes (i.e., increase revenues) and Democrats refuse to rationalize spending (i.e., cutting costs). Both are necessary, but each party blames the other for the country’s debt problems. Each party’s political dogma apparently is more important than lowering borrowing costs for Americans.

Frogs are vertebrates. Their skeletal system aids them in jumping out of pots of hot water. Investors should certainly hope Washington finds its spine and jumps out of the already warming pot – and does so before it reaches the boiling point.

Copyright © Richard Bernstein Advisors (Janus Henderson)