by Avi Lavi, Global and International Value Equities; Portfolio Manager, AllianceBernstein

Value stocks are once again facing questions about an uncertain future. In recent months, growth stocks have reasserted themselves after a seven-month value rally through May. But there are still good reasons to anticipate a renewed recovery of value stocks.

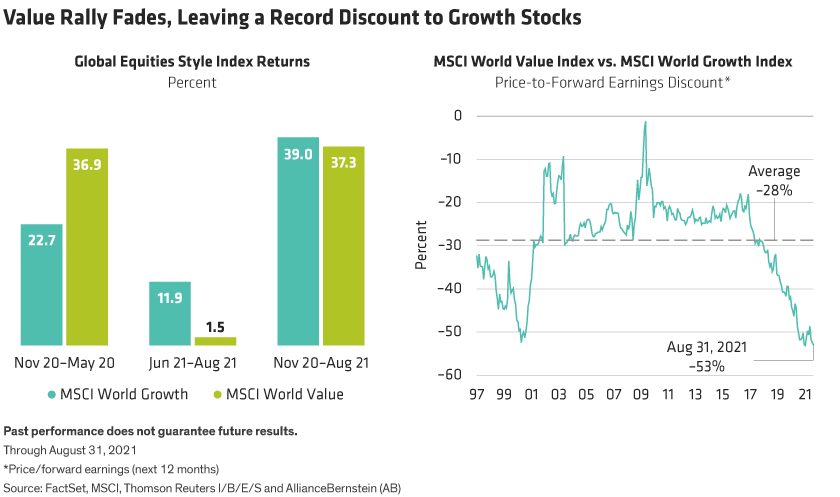

The world’s uneven recovery from the pandemic has been accompanied by changing equity return patterns. Global value stocks surged by 36.9% from November 2020 through May 2021, outpacing growth stocks by a wide margin. Since June, the trend has reversed (Display, left). By the end of August, global value stocks again traded at a record 53% discount to growth stocks (Display, right).

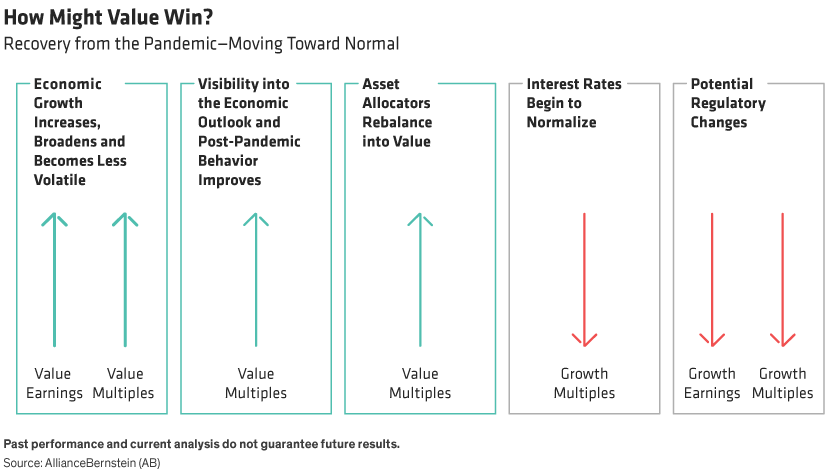

Over the last decade, value investors have repeatedly asked what it would take to turn the tide from growth’s dominant outperformance. In our view, five key developments could foster an unwinding of the extreme divergence of value and growth stock valuations in the coming years (Display).

1. Economic Recovery Accelerates and Broadens

The COVID-19 pandemic triggered the worst global macroeconomic crisis in decades. As entire industries shut down, unemployment surged, growth collapsed and uncertainty mounted. However, the historic collapse may also map the contours of a historic recovery. Consensus estimates project real US GDP growth of more than 6% in 2021. While the path to recovery will face obstacles, over time, as the world begins to return to normal, we believe growth will accelerate and broaden, generating a tangible rebound in business activity overall and across more industries. And growth will likely become less volatile as its sources diversify. These trends should make a visible impact on the earnings of value companies, which would in turn provide an impetus for pushing up the multiples of value stocks.

2. Visibility into the Outlook as Post-Pandemic Behavior Improves

Multiples of value stocks are also affected by confidence in the future. Since value stocks are typically seen as riskier investments than their growth peers, a lack of confidence in the outlook makes investors demand much higher risk premiums for owning these stocks, which in turn suppresses their multiples. As COVID-19 vaccinations are increasingly rolled out and countries make progress in combating the pandemic, we believe investors will gain confidence in the trajectory of the nascent economic recovery. When this happens, the risk premia for owning value stocks should decline, which would help support a recovery of value multiples, in our view.

Today’s uncertainty isn’t limited only to the economic outlook. Uncertainty about how consumer and business behavior will change after the pandemic has made it very difficult for investors to forecast long-term cash flows in many industries. But this won’t last forever. As economies start to reopen, we expect to see a rise in consumer and business spending, particularly in hard-hit industries such as travel, entertainment and retail. Given the recent resurgence of the delta variant globally, it’s still hard to say today what the recovery trajectory will look like for industries that were severely impaired during the crisis. That’s why the range of expected outcomes for many companies is extremely wide. However, as life begins to return to normal and investors gain clarity on post-pandemic behavior, we expect that range of outcomes to narrow. Even if demand in industries such as business travel will be reset at much lower levels than in the past, the reduction in uncertainty itself will help lower the risk premium for value stocks.

3. Asset Allocators Rebalance into Value

Growing confidence could start to pull flows back toward value portfolios. As asset allocators reassess the environment—and their exposures—we expect more fund flows to shift toward value, which should add support for value stocks.

4. Interest Rates Begin to Normalize

As the global economy struggles to regain its footing, central banks are committed to keeping interest rates low. But in late 2020, US Treasury yields began to rise amid hopes that COVID-19 vaccines could support a broader economic recovery. Massive fiscal stimulus programs around the world may ultimately fuel higher inflation. And at some point, central banks would be compelled to raise rates in response. While 10-year Treasury yields have fallen from peaks of about 1.7% in April to about 1.3% in August, we believe an incremental rise in rates will eventually materialize. In late August, the Bank of Korea raised interest rates from historic lows, becoming the first major Asian economy to do so—and raising speculation of potential rate hikes to come elsewhere. If the trend broadens, it will add an important element to the normalization of the value-growth valuation gap by pushing down multiples of growth stocks relative to value stocks.

5. Potential Regulatory Changes

In recent years, the best-performing growth stocks were dominated by the US FAANGs—Facebook, Amazon, Apple, Netflix and Google. Investors have been captivated as the growing dominance of these companies has fueled strong, long-term growth potential, and by the boost they received from increasing digitalization of work, leisure and commerce during COVID-19. At the same time, increasing concern about the FAANGs’ unchecked power in multiple industries has drawn the attention of lawmakers and regulators. In July, a regulatory crackdown on China’s big technology companies triggered a self-off in the sector. Could this be a harbinger for the west? Increased regulatory scrutiny in the coming years may have an impact on big tech’s business models and earnings potential, potentially constraining the multiples of mega-cap growth stocks.

What Are the Risks to Recovery?

There are many risks to this five-pronged value-recovery scenario. First, the global economic recovery from the pandemic isn’t progressing in a straight line and confidence in the long-term outlook remains shaky. Second, it’s still difficult to predict how business and consumer behavior will change over the long term.

Third, interest rates are a wild card. While there are good reasons to believe that interest rates will eventually rise—particularly if inflation surfaces—major central banks are still committed to keeping rates at historical lows for an extended period. Fourth, regulatory action is always hard to predict. So it’s hard to determine how tighter scrutiny on growth mega-caps might unfold, how long it will take and how investors will react to the new risks.

Nobody can say exactly how these trends will unfold. That said, since the value recovery scenario we’ve outlined has five components, there is room to maneuver. Disappointment on one front could be offset by upside surprises on another. And since value stocks still trade at a huge discount to growth stocks, we believe the payoff potential in a recovery scenario is especially enticing.

This blog is the fourth excerpt in a series based on our recent white paper Value’s New Hope: Will the Pandemic Exit Be the Catalyst?, published in March 2021.

Avi Lavi is Chief Investment Officer—Global and International Value Equities; Portfolio Manager—Global Research Insights

The views expressed herein do not constitute research, investment advice or trade recommendations and do not necessarily represent the views of all AB portfolio-management teams and are subject to revision over time.

MSCI makes no express or implied warranties or representations and shall have no liability whatsoever with respect to any MSCI data contained herein. The MSCI data may not be further redistributed or used as a basis for other indices or any securities or financial products. This report is not approved, reviewed or produced by MSCI.

This post was first published at the official blog of AllianceBernstein..