by Shamaila Khan, AllianceBernstein

In a global pandemic, everyone is in the same storm, but they aren’t in the same boat. As the crisis began, the market had significant concerns about the seaworthiness of some emerging markets (EM), and with good reason. Had these smaller, more fragile economies attempted to implement some of the policies developed-market countries embarked on, they would have been swamped. But they didn’t, and they weren’t.

Everything That Could Go Wrong Didn’t

And yet, within the EM debt space, both hard- and local-currency sovereigns sold off much harder than corporate credits during the COVID-19 shutdowns. Why?

For one thing, investors were concerned that EM countries would bog down their economies by trying to undertake developed-market-level quantitative easing. Instead, EM countries facilitated liquidity and market operations through limited open market bond purchases, restraining debt monetization to very small amounts as a percentage of GDP.

Investors were also concerned that costs stemming from the pandemic might capsize smaller EM economies. While some fiscal deterioration materialized, EM generally navigated the health situation better than expected, and both markets and the International Monetary Fund (IMF) stepped up quickly to provide needed liquidity.

Finally, the G20’s Debt Service Suspension Initiative prompted a flurry of headlines and research papers suggesting there may need to be multiple restructurings in EM debt. However, our bottom-up fundamental research suggested that, while selectivity was warranted, there was no systemic problem.

Looking Forward—Opportunities Abound

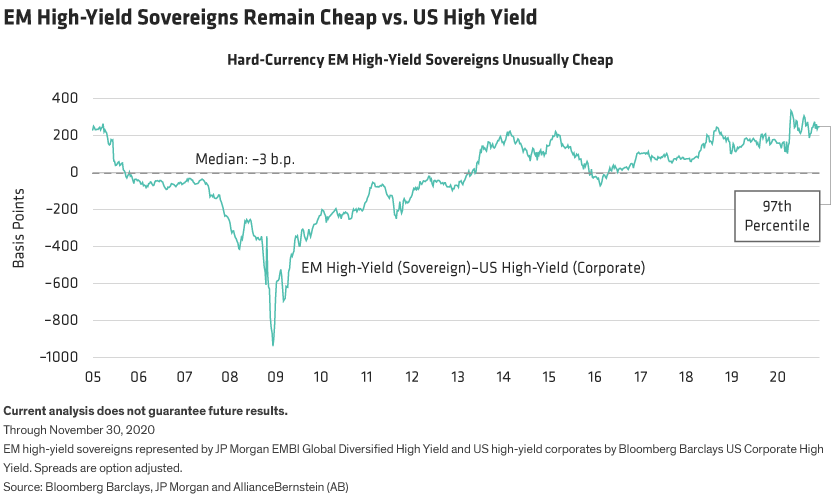

While the potential risks to EM sovereigns have dissipated, valuations for high-yield sovereigns remain the most compelling opportunities. EM high yield is currently trading at historically wide spreads compared to US high yield (Display).

Importantly, we expect strong global growth in 2021 to provide relatively smooth sailing through a cyclical uplift for EM, with relatively robust external balances providing additional wind in the sails. However, this uplift may not look like a textbook case of economic resurgence.

As economies recover, increased imports by EM countries could partially unwind the external improvement seen in 2020. This would be a healthy rebalancing and proof of recovery. Additionally, we expect that remittances to EM countries, which held up better than expected during the crisis, will continue to increase. And finally, as global activity and tourism recover, we expect EM oil exporters to benefit from rising commodity and oil prices.

Strong demand for EM debt coupled with low net bond supply should also create favorable investing conditions. We believe there is a growing likelihood of a new IMF Special Drawing Rights (SDR) allocation, which would be supportive of EM finances and bond prices. This would be of specific benefit to countries with high external financing needs, which benefit the most from SDR allocations.

All Debt Is Not Equal

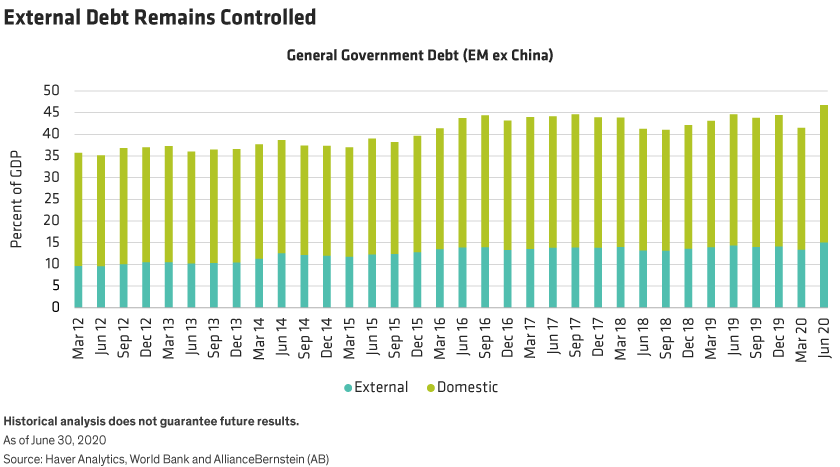

Some market participants have expressed concern about EM debt burdens sinking the expected recovery. Those concerned about EM debt burdens should, however, remember that all debt is not equal. Had EM countries leaned disproportionately on external or hard-currency debt, the risks would have been greater, but most EM debt increases have been domestic. Not only are external debt levels not overwhelming, they also have not increased significantly over the past eight years (Display). And finally, for the external debt that does exist, our outlook is for US-dollar depreciation that could help to lower EM debt burdens.

The Rising Tides Should Lift Many Boats

The best opportunities in EM sovereigns remain in high-yield countries where assets remain mispriced and fiscal improvement is likely. But the benefits will accrue from different streams and waves.

For example, South Africa is a low-growth country with high fiscal deficits and whose bonds were heavily impacted by the COVID-19 crisis. The pandemic exposed economic and fiscal vulnerabilities, but it also led to—or forced—promising political and policy reform. South Africa is also likely to be a big beneficiary of rising commodity prices and global growth.

While Angola would also benefit from rising oil prices and global growth, further buoyancy for Angola would come from a new round of SDR funding, given their high external financing needs and an SDR that comprises a large portion of their existing reserves. Similarly, Ukraine would also be an outsized beneficiary of a new IMF SDR allocation.

We believe the impetus for cyclical uplifts for other EM countries may be quite diverse. Remittance- and tourism-dependent El Salvador and Egypt, for example, came through the COVID-19 downturn better than expected, as remittances did not sink as much as expected. Still, both countries should benefit from remittances returning to more normal levels. Egypt will benefit over time from a return to more typical tourism flows, and El Salvador will benefit from the US recovery.

Finally, credits such as Argentina, have gone through restructuring, may be mispriced, trading on sentiment rather than fundamentals. Once Argentina has set medium-term economic policy based on negotiation with the IMF, we believe prices will move toward intrinsic value.

Investors should always be discriminating when investing in EM debt. But as we expect the greatest cyclical uplift over the next year in select EM high-yield sovereigns, those navigating these waters should be prepared with ongoing fundamental research to keep portfolios on course. Investors should have the opportunity to collect higher income while investing in economies ready to be lifted by cyclical waves.

Shamaila Khan is Director of Emerging Market Debt and Adriaan du Toit is Senior Economist—Africa at AB.

The views expressed herein do not constitute research, investment advice or trade recommendations and do not necessarily represent the views of all AB portfolio-management teams. Views are subject to change over time.

This post was first published at the official blog of AllianceBernstein..