Inflationado? Muni Investors Should Seek Cover - Context

by Fixed Income AllianceBernstein

US inflationary pressures are developing that could be destructive. Investors need to seek protection quickly. But how? For municipal investors, some inflation strategies fall short, leaving portfolios at risk.

To be sure, not everyone is convinced that inflation is a serious concern today. In fact, until a January data release showed accelerating wage growth, a good many investors believed that inflation was dead because it had been dormant for so long. But that data, followed on February 14 by faster-than-expected core inflation data, which excludes food and energy, began to turn investors’ heads.

Many investors are now coming around to our view that inflation is going to rise in 2018.

Inflation Pressure Is Building

At 1.85%, year-over-year core inflation is still below the Fed’s 2% target. However, pressures are building below the surface. Six-month annualized core inflation is running well above the 2% mark and is climbing. Various factors that continue to hold down the year-over-year reading are likely to dissipate over the next few months.

At the same time, many factors are likely to drive inflation higher over the near to medium term. These include accelerating US and global growth, tighter labor markets, a weakening dollar, and easier financial conditions. (It’s true: despite the Federal Reserve’s efforts to drain liquidity from the system, it’s easier for businesses to access and deploy capital today than at the start of 2017.)

Further factors? Falling federal revenues and increased federal spending—think tax reform and the federal budget deal—which together create an inflationary environment. Rising oil and copper prices over the longer term, which offer further evidence to support our expectations for higher prices over the near term. And we’ve also considered demographic trends, such as retiring baby boomers, which translate into a declining work force; as well as more restrictive trade and capital flows, which encourage cash trapping.

Put it all together, and inflation could heat up.

Why does rising inflation matter so much to investors? Because higher rates of inflation erode bond returns, sometimes to the point that bond returns are negative after accounting for the effect of inflation (Display).

What’s more, savvy investors know that even before inflation begins to erode the value of their portfolio, they can profit from inflation strategies. Here’s how it works.

Expectations Drive Results

Since the Fed began raising official rates in 2015, both bond yields and “break-even” inflation rates have been rising. The break-even inflation rate describes the difference between the yields on Treasury Inflation-Protected Securities (TIPS) and the yields on comparable-maturity Treasuries.

They also serve as a measure of market participants’ collective inflation expectations. Since December 2015, those expectations, as measured by the break-even inflation rate on five-year securities, rose from 1.3% to 2.0%.

During that period, inflation protection outperformed. That’s because inflation strategies outperform when expectations rise, as well as when inflation itself rises. For example, in 2017, as inflation expectations climbed, five-year Treasury securities posted returns of 0.68%, while comparable-maturity TIPS delivered 0.80%, for an outperformance of 0.12%.

Subject to Taxes? TIPS Fall Short

Buying TIPS is the most common and direct way to get inflation protection. TIPS provide inflation protection by adjusting the face value of the investment by the inflation rate and then paying interest on the adjusted face value. For example, a TIPS with a $1,000 face value and a 1.5% coupon will pay $15 in annual interest. If inflation is 2%, then the value is adjusted to $1,020 and the annual interest increases to $15.30.

The advantage of TIPS’ structure is that investors keep up with inflation and are offered a real rate of return. The disadvantage is that, for investors who pay taxes, TIPS are notoriously tax inefficient. The interest on the underlying TIPS is taxed at ordinary income rates, and so is the inflation adjustment.

But here’s the kicker. The inflation adjustment is received when the TIPS mature, but is taxed in the year in which it was realized. That makes it “phantom income.”

Thankfully, for investors who are subject to taxes, there is a more tax-efficient form of inflation protection.

Inflation Protection Designed for Muni Investors

The tax-exempt market has its own form of inflation-protected securities known as municipal inflation-protected securities (MIPS). Unfortunately, due to the MIPS market’s relatively small size—just over $1 billion—it’s a very illiquid market. Because they are scarce, MIPS often trade at more expensive levels relative to TIPS than the municipal/Treasury relationship suggests.

Fortunately, there’s another way. By combining tax-exempt (and not inflation-protected) municipal bonds and consumer price index (CPI) swaps, investors who pay taxes can tap into two very large and highly liquid markets. CPI swaps are agreements in which investors arrange to “swap” fixed interest payments for floating-rate payments tied to inflation rates, for a predetermined length of time.

The combination offers two layers of tax efficiency. First, the underlying municipals are exempt from federal taxation. Second, the CPI swaps are taxed at capital gains rates, which can be sheltered through the realization of losses. And there is no phantom income.

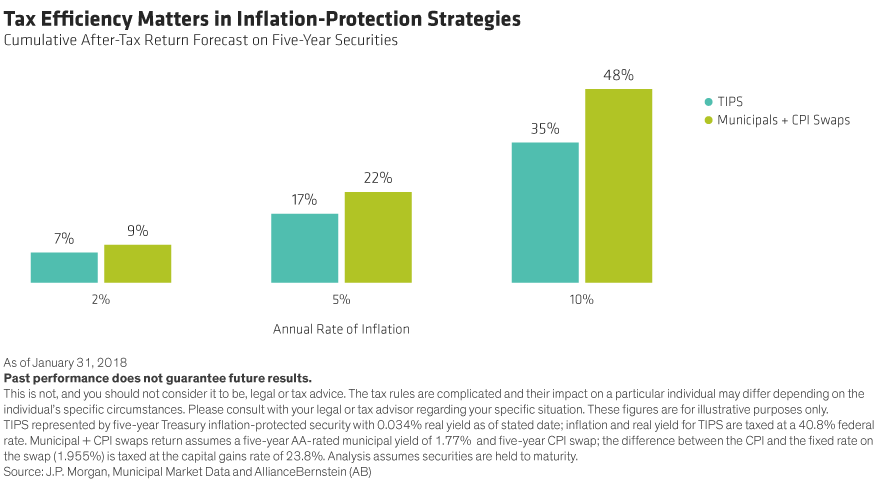

This tax efficiency really adds up during inflationary environments, relative to TIPS (Display).

As inflationary pressures build, tax-efficient inflation protection should not only shield municipal portfolios from surges in actual inflation, but it should also outperform ordinary municipals even as expectations rise.

That means it’s important for investors not only to seek cover before inflation starts to erode returns but before inflation protection becomes expensive to buy. And it almost goes without saying that it’s critical that your manager knows how to assemble inflation protection in the most tax efficient and liquid way. Because when a storm is brewing, you’re only as secure as your shelter.

The views expressed herein do not constitute research, investment advice or trade recommendations and do not necessarily represent the views of all AB portfolio-management teams.

Copyright © AllianceBernstein