by Michelle Gibley, CFA, Director of International Research, and Chris Ferrarone, Schwab Center for Financial Research

Key takeaways

- The war in Iran has evolved from a geopolitical event to a global energy supply shock. The disruption to energy and commodity supplies is likely to have an increasingly negative impact on economic and financial conditions the longer it goes on.

- Even if military activity ends soon, the impacts to growth, inflation, and commodity prices could linger. And the longer energy and commodity supplies remain disrupted, the greater the potential economic damage. Asia appears most vulnerable, with Europe also facing meaningful exposure.

- While markets would likely rebound in the case of an end to military operations, international developed and emerging-market stocks may not resume their outperformance. Our base-case outlook is consistent with the Moderate scenario we lay out below, and implies greater downside risks for international markets in the near term and lingering economic and financial pressures that could persist over the next six to 12 months even with a quick end to the conflict. Said differently, we are less convinced international stocks can resume their outperformance in a Moderate case scenario.

Scenario framework: Three potential outcomes

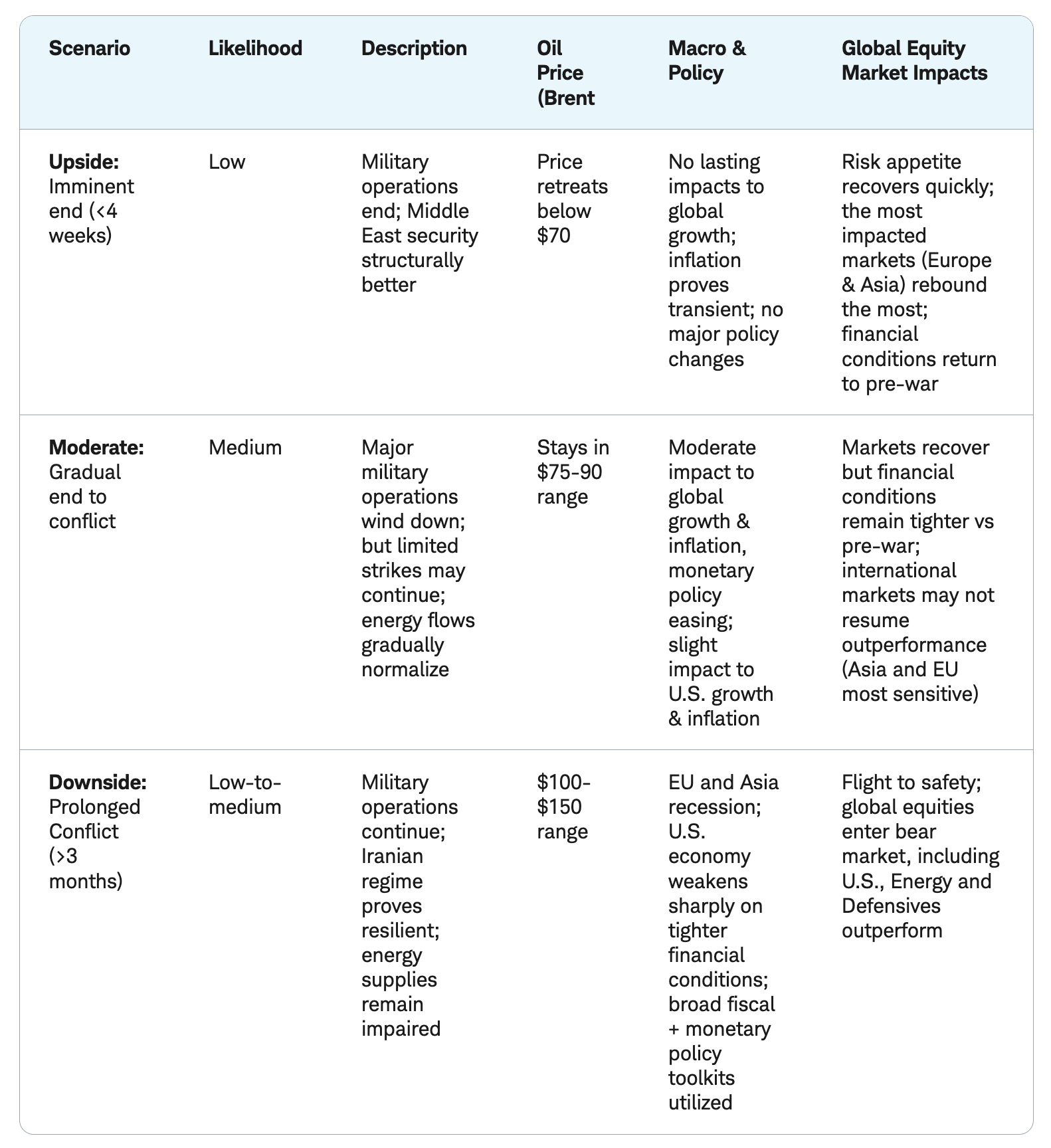

We are tracking the Iran war and potential economic and market outcomes via a scenario analysis that has three potential outcomes—an upside case, a moderate case and a downside case. The scenario table below provides an assessment of the likelihood of each case, including details on the potential impact to equity markets. The upside case is defined by a quick end to military operations, with energy production and shipments normalizing and market pricing returning toward pre-conflict levels. We see the likelihood of this case as reduced given the worsening conflict and disruptions to energy and commodity supplies.

The probability of the moderate case has increased and is now consistent with our baseline view. In this scenario, military operations may continue for several weeks before winding down. Oil prices may remain elevated due to lingering supply impacts and general uncertainty. The disruption to energy supplies has already increased in both intensity and duration since the start of the war. The longer energy and commodity supplies remain disrupted, the greater the economic damage. In this environment, financial conditions can remain tighter than normal and risk aversion can stay higher for longer, and market leadership may not revert to international markets as had been the case leading up to the war.

The downside case presents more severe risks to portfolios with a prolonged conflict leading to energy and commodity shortages, sharply higher commodity prices and rapidly tightening financial conditions. Such an outcome would raise recession risk while also possibly lifting inflation, which is a particularly difficult mix for policymakers to respond to. In this scenario, the potential for deeper and more persistent drawdowns across global equities increases. The risk of this scenario has increased but remains less likely than the moderate case, in our opinion.

The current environment represents a geopolitical event that has evolved into a supply shock. History shows relatively mild impacts to equity markets after geopolitical crises. By contrast, major energy supply shocks have had more severe economic and financial market impacts. This conflict has effectively stopped all traffic from moving through the Strait of Hormuz, an event that has not occurred since the 1970s. Energy producers in the Middle East are running short of storage, which threatens to halt production altogether and raises the possibility of severe supply constraints. The worsening risk changes our outlook for international developed and emerging-market stocks.

Risks for Asian economies are particularly large given their reliance on Middle Eastern energy supplies, including oil and natural gas, where supply shortages emerge quickly given the difficulties of storing liquified natural gas (LNG). This is not just about energy either, but a potential systemic disruption across dry bulk, freight, fertilizers, and other commodities that have the potential to impact food supplies and production of key global products like semiconductors. The MSCI Korea Index has over 50% exposure to two memory chip companies. The longer the war in Iran and energy supply disruptions last, the bigger the chance the memory chip shortage intensifies either due to restrictions on access to energy or higher energy prices.

History suggests equity markets would rebound, perhaps rapidly, when military operations end. That said, this conflict presents meaningful downside risks, and potential for lingering economic and market impacts that may not mean markets return to pre-war trends immediately.

Iran war scenarios and potential impact on global equities

How to think about the rise in energy prices

The rise in energy prices since the conflict started is a key input to our outlook that has changed and needs to be accounted for. Europe and Asia-Pacific are more reliant on oil and gas imports and are particularly exposed to Middle East supply disruptions. The U.S. is less exposed due to domestic energy production but is not immune to the negative impact higher global oil and gas prices can have on both consumer spending and manufacturing production.

Energy supply to international countries is currently disrupted by two main chokepoints: effective closure of traffic through the Strait of Hormuz and the shut-in of LNG production in Qatar. These chokepoints have resulted in 20% of global oil and 20% of global LNG supply being cut off. The release of strategic petroleum reserves by the International Energy Agency (IEA) can help offset some of the disruption but there is a limit to how much can be drawn down on a daily basis. It's not just energy that is disrupted—4.5% of annual global trade also passes through the strait, according to Bloomberg estimates. Fertilizer, helium for semiconductor chip production, precious metals, aluminum, and cement are likely to be the most affected.

Even if the war ends quickly, producers in the region are running out of storage, which threatens a halt in output and an extended duration of disruption. There is a non-linear impact of production halts for engineering reasons: For example, on the LNG side, there is a slow process of restarting production to avoid thermal shock to sub-zero cryogenic equipment. Restarting too fast could damage or rupture equipment. Staff may have departed and maintenance may be needed. Higher energy prices may last longer than the war.

Performance of oil prices around geopolitical conflicts

Source: Charles Schwab, ICE and Macrobond as of 3/12/2026.

Chart depicts 60 trading days before and 60 trading days after the start of military conflict. For illustrative purposes only. Brent is the leading global price benchmark for Atlantic basin crude oils. Commodity-related products carry a high level of risk and are not suitable for all investors. Commodity-related products may be extremely volatile, may be illiquid, and can be significantly affected by underlying commodity prices, world events, import controls, worldwide competition, government regulations, and economic conditions. Indexes are unmanaged, do not incur management fees, costs, and expenses and cannot be invested in directly. Past performance is no guarantee of future results.

The outlook for international stocks is balanced

We entered 2026 with a positive outlook for international equity exposure, predicated on several key factors including accelerating earnings, attractive valuations relative to the U.S., favorable sector exposures, and a weaker dollar. Positively, leading indicators had been picking up, supporting an acceleration in earnings expectations. The Global Manufacturing Purchasing Managers' Index (PMI) rose to a four-year high in February, with gains in new orders indicating continued growth and investment. However, an increased probability of the moderate scenario and energy shock means economic growth and earnings may slow in the near term. The slowdown may last several months and take time to reaccelerate.

Global earnings tend to move with economic growth

Source: Charles Schwab, S&P Global and Macrobond as of 3/5/2026.

The JP Morgan Global Manufacturing PMI is truncated for visual purposes; it was 36.8 in November 2008, 33.8 in December 2008, 35.2 in January 2009, and 36.7 in February 2009.

The MSCI World 12-month forward EPS refers to the estimated earnings per share (EPS) of index constituents for the next 12 months. Forecasts contained herein are for illustrative purposes only, may be based upon proprietary research and are developed through analysis of historical public data. Indexes are unmanaged, do not incur management fees, costs, and expenses and cannot be invested in directly. Past performance is no guarantee of future results.

Sector exposures are less favorable than at the start of the year. The potential for increased defense spending globally and construction of data centers for artificial intelligence (AI) and infrastructure is likely to continue. This would likely increase opportunities for stocks in the Industrials sector. Industrials account for 20% of the MSCI EAFE Index. Financials are 25% of the MSCI EAFE Index, which may experience reduced profits if the global economy slows. Emerging-market (EM) stocks are tied to the growth in the buildout to support AI due to a 33% weight in Technology, as well as internet-related companies within the Communication Services and Consumer Discretionary sectors.

The U.S. dollar decline may be arrested in the near term, reducing this positive factor for the performance of international stocks, as dollar weakness improves returns for both developed-market international and emerging-market stocks, as seen in the chart below. Once the conflict subsides, we believe dollar weakness could resume. Our view of geopolitical fracturing and a shift away from dollar-denominated assets remains intact and is potentially strengthened by the nearly unilateral start of the war in Iran.

International stocks tend to perform better when the dollar is weak

Source: Charles Schwab, MSCI, ICE and Macrobond data as of 3/12/2026.

Indexes are unmanaged, do not incur management fees, costs, and expenses and cannot be invested in directly. Past performance is no guarantee of future results.

Valuations of international stocks are still attractive relative to U.S. stocks even though developed-market valuations have risen over the past year. Valuations for emerging-market stocks remain less expensive than both developed-market international and U.S. stocks as earnings estimates for EM companies have risen faster than stock prices so far in 2026.

International stocks have lower relative valuations

Source: Charles Schwab, MSCI, Macrobond data as of 3/5/2026.

Indexes are unmanaged, do not incur management fees, costs, and expenses and cannot be invested in directly. Past performance is no guarantee of future results.

What would cause a change in our view to unfavorable on international stocks?

We would need to see a situation whereby the initial energy price shock was affecting fundamental macro-economic conditions and raising recession risk. Some of the things we will be monitoring include:

- A sustained disruption to global energy supplies that caused oil and gas prices to spike further and remain elevated, which could weigh on earnings expectations;

- Signs that higher energy prices are feeding into broader inflation persistence (beyond a short-lived bump), which would limit central bank flexibility;

- Tightening liquidity conditions that raise concerns about financial stability.

In sum

Probabilities around the Iran War have shifted negatively, with an energy shock that could cause adverse growth, inflation and financial condition impacts. Now is not the time to aggressively add risk, making international developed- and emerging-market stocks less attractive over the near term, despite factors that could support returns over a 12-month period or longer.

Stocks could rapidly rebound if military operations end but lingering energy supply disruption may limit the amount of rebound. The key trigger for a more defensive stance would be a sustained, supply-driven energy shock that meaningfully lifts recession risk.

Heather O'Leary, Senior Manager, Equity Research and Strategy, contributed to this report.

Copyright © Schwab Center for Financial Research