by Hubert Marleau, Market Economist, Palos Management

Contrary to adversaries, who called the prediction markets run by Kalshi and Polymarket outright gambling, I’m of the opposite opinion that their success is because they are intelligent assets based on the notion that masses have knowledge, understanding and foresight about what is going on in the world, which was popularised by James Srowiecki’s book. “The Wisdom of Crowds”.

Prediction markets allow people to bet on the outcome of futures events, like the futures market does for prices of commodities, stocks and bonds, with prices shifting to reflect probability. These markets are able to aggregate dispersed information, capable of outperforming polls, experts, economic indicators and geopolitical developments. The fact that there’s no “BS” for their predictive power stems from having money on the line and speed of execution, making them an efficient transmission of important signals.

Indeed, futures and prediction markets for oil are full of information, insight and calculated conviction, and have a knack to assess the probability of what could happen with energy prices, the global economic outlook and war in the Middle East.

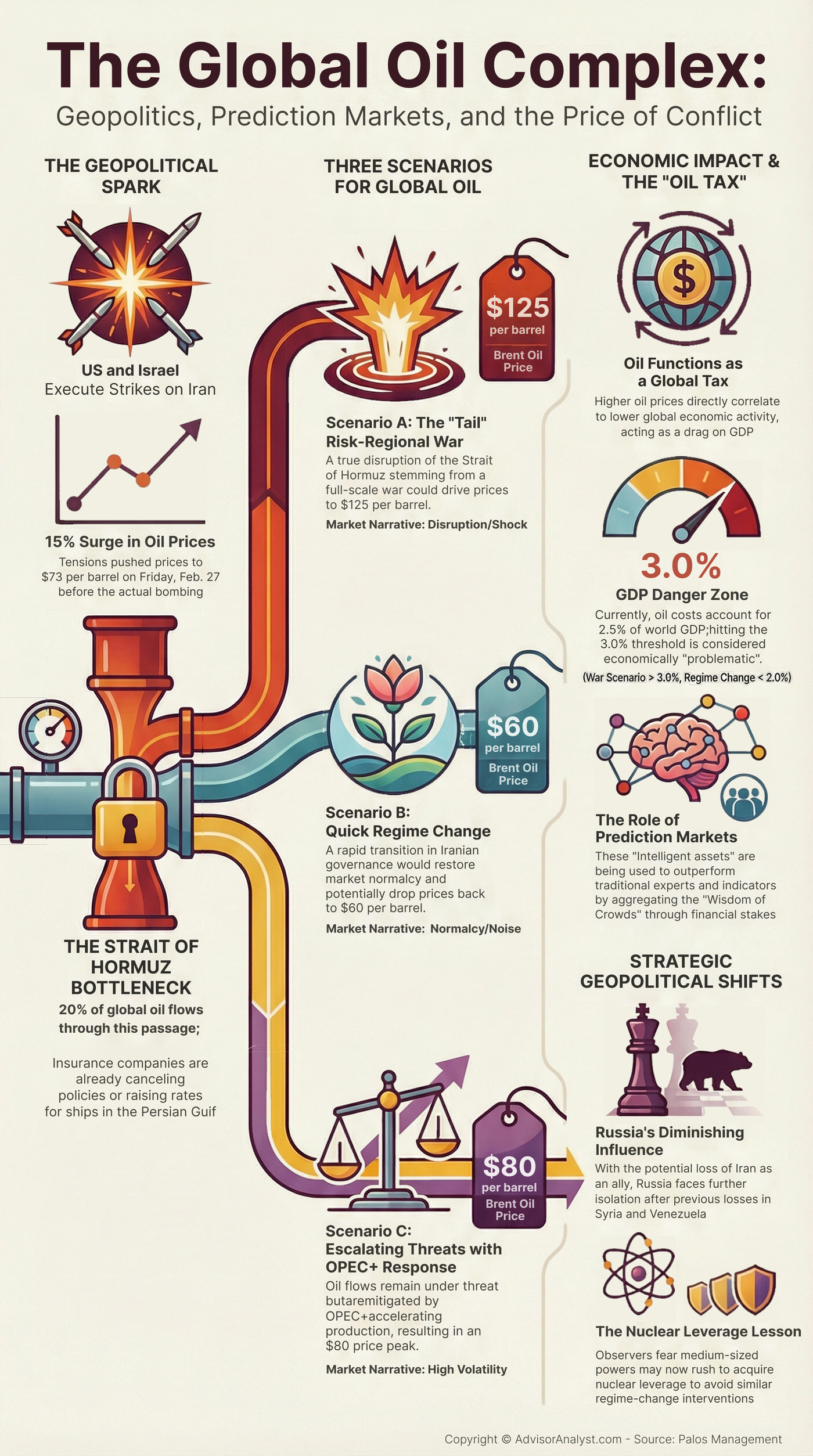

Ordering strikes on Iran by the US and Israel on Saturday morning as one would have expected, Iran reacted immediately, by launching a bunch of missiles at US bases in the oil-rich Persian Gulf, including Qatar, Bahrain and the UAE. As a consequence, all hell broke in the global oil complex. Oil prices have already risen roughly 15% since tensions between the U.S. and Iran started a few weeks ago, touching $73 on Friday before the bombing occurred.

The situation poses a huge risk for the direction of the price of oil, given that the region is economically sensitive, and that 20% of global oil flows through the Strait of Hormuz. Insurers are cancelling policies or raising prices for ships in the Persian Gulf, suspending maritime activities.

Hard geopolitics have hijacked the narrative, changing the center of gravity from AI to crude oil cargoes. The question is whether this geopolitical development will either descend into a regional war causing huge disruption in the flow of oil or bring about a quick end to the regime in Iran, allowing crude flow to move along. One is shock and the other is noise.

In this connection, the market will bridge the gap with movements in the spot and futures trade. A true Hormuz disruption scenario stemming from a war would constitute a tail scenario, which could easily increase the price of Brent oil to $125 a barrel, whereas, a quick regime change would oppositely restore normalcy and bring back oil prices back to $60 a barrel. There is a third scenario, where the oil flows under threat not in an apocalyptic manner as OPEC+ increases oil production at an accelerating pace; but nonetheless in an escalating one, constraining supply and running the price to an $80 peak.

Investors should note that oil works like a tax: the higher the price, the lower global economic activity.

Thus, over the coming days, it will be crucial to follow both the prediction and futures markets for crude and bonds; they will be full of calculated conviction, assessing the probability of what could happen to energy prices, the global economy and war in the Middle East; let alone US monetary policies and Chinese reactions.

On Friday, February 27, the Brent Crude oil closed at $73.21, $5.19 higher than a one year future. At this price, the total cost of oil accounts for 2.5% of the world GDP, only 0.5% less the 3.0% threshold where it becomes problematic.

While the American allies supported Trump’s strikes against Iran, they implored the Persian government to negotiate a solution - a probable scenario given that Iran’s Supreme Leader is now dead as a crow. The situation may force the Iranian forces to seek immunity for lack of wanting to fight, fearing that uninterrupted bombing would destroy everything military. As it stands, the Trump administration will not accept anything less than a regime change, willing to end the Iranian nuclear program.

While the objective of the attacks may be worthy of consideration, history shows that interventions in the Middle East rarely have favourable outcomes. On the one hand, Russia just lost another ally, after losing Syria and Venezuela. And that is a big plus for America and the West. On the other hand, the lesson for medium powers is to grab whatever nuclear leverage they can, as fast as possible, before they end up crossing certain unacceptable political red lines.

Copyright © Palos Management