by Craig Basinger, Chief Market Strategist, Purpose Investments Inc.

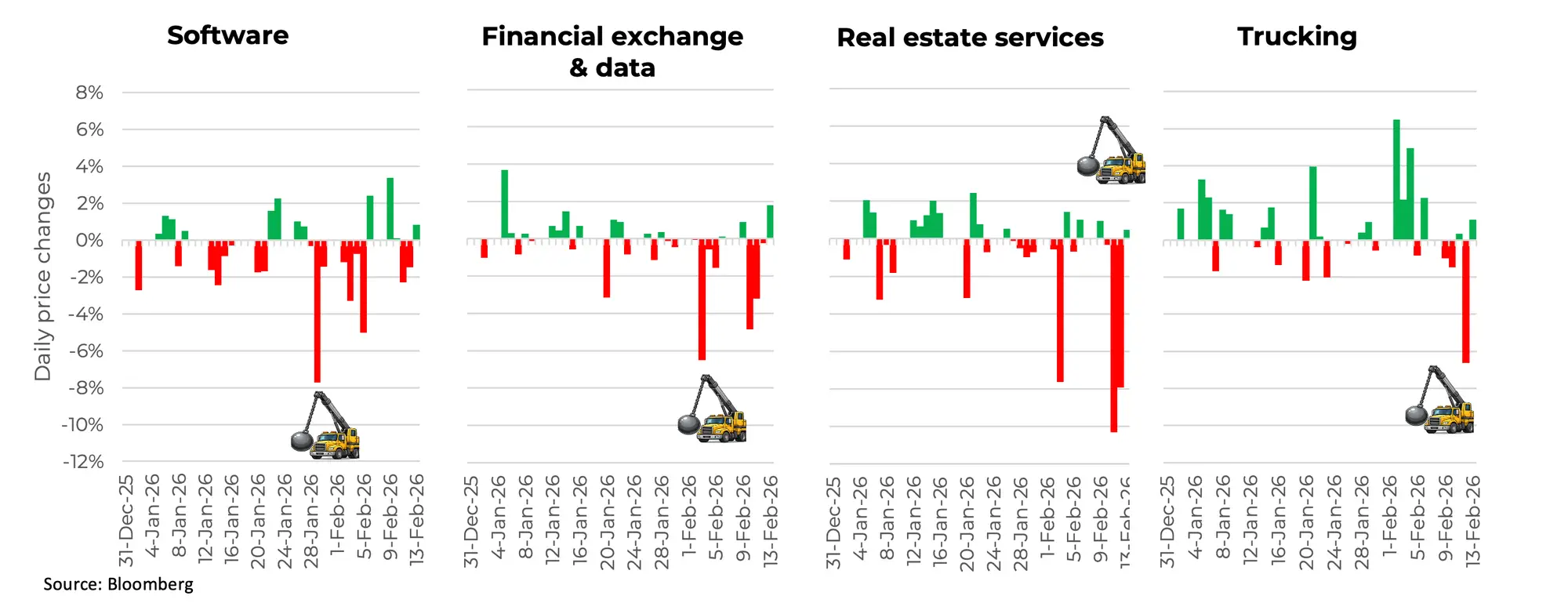

There is a wrecking ball bouncing from one industry to the next, and folks are calling it the AI Scare Trade. Wherever there’s any whiff of how AI could potentially disrupt an existing business model or service, stocks plunge lower. We discussed this last week in “Markets get Claude’d”, as Anthropic AI services’ new functionalities impacted the software space generally. This spread to legal and other services.

This past week, the AI wrecking ball visited wealth services, real estate firms, insurance brokers, rating agencies, and trucking. Some of the price moves are a bit eye-watering. S&P and Moody’s, both providers of financial services, including credit ratings, were down 25% and 20%, respectively, over the past couple of weeks. Raymond James, a wealth services company, dropped 10% when a financial planning AI tool was announced.

Perhaps the most outrageous price reaction may have been in the trucking industry. A Florida company, Algorhythm Holdings, announced its service has improved customers’ scale freight volumes by 300% to 400% without adding headcount. This knocked billions in market capitalization off truck transport shares. This company had $2 million in revenue as of September and just recently divested its previous core business of selling karaoke machines. The company’s ticker is RIME, more fitting when the name was Singing Machine Company.

As the AI wrecking ball moves from one industry to the next on even the slightest whiff of disruption, does it present an opportunity, or is the market right to drop five, 10, even 20%? Markets do overreact in the short term and sometimes underreact in the really long term. It also appears these dramatic moves are driven in part by retail and likely some quant algorithms. It’s somewhat reminiscent of Roaring Kitty, but instead of hyping up questionable business models, it’s quickly deflating profitable businesses.

Leadership Rotation: Can The Market Have It Both Ways?

Lately, there have been rising concerns over the return on investment for the hyperscalers that are building out AI infrastructure. The capex levels are eye-watering and still rising, while the market is simply not sure they will make enough money to justify the dollars spent.

This is captured in the credit default swaps for Oracle, perhaps the hyperscaler with the most aggressive push into the space. In September, swaps sat at 40 bps, now 160 bps. BUT, if AI can disrupt all the above-mentioned industries in a material way, there’s clearly huge ROI potential.

As with everything, the truth usually sits somewhere in the middle. The hyperscalers will likely have a challenging time generating enough ROI, but they have strong balance sheets and are comfortable with the risk. Plus, the trend over the past year has been to spread that risk via more debt structures and circular finance arrangements. On the various industry sides, yes, there will be disruption, and business models will evolve – just probably not in the doomsday events being priced in off one headline here or there.

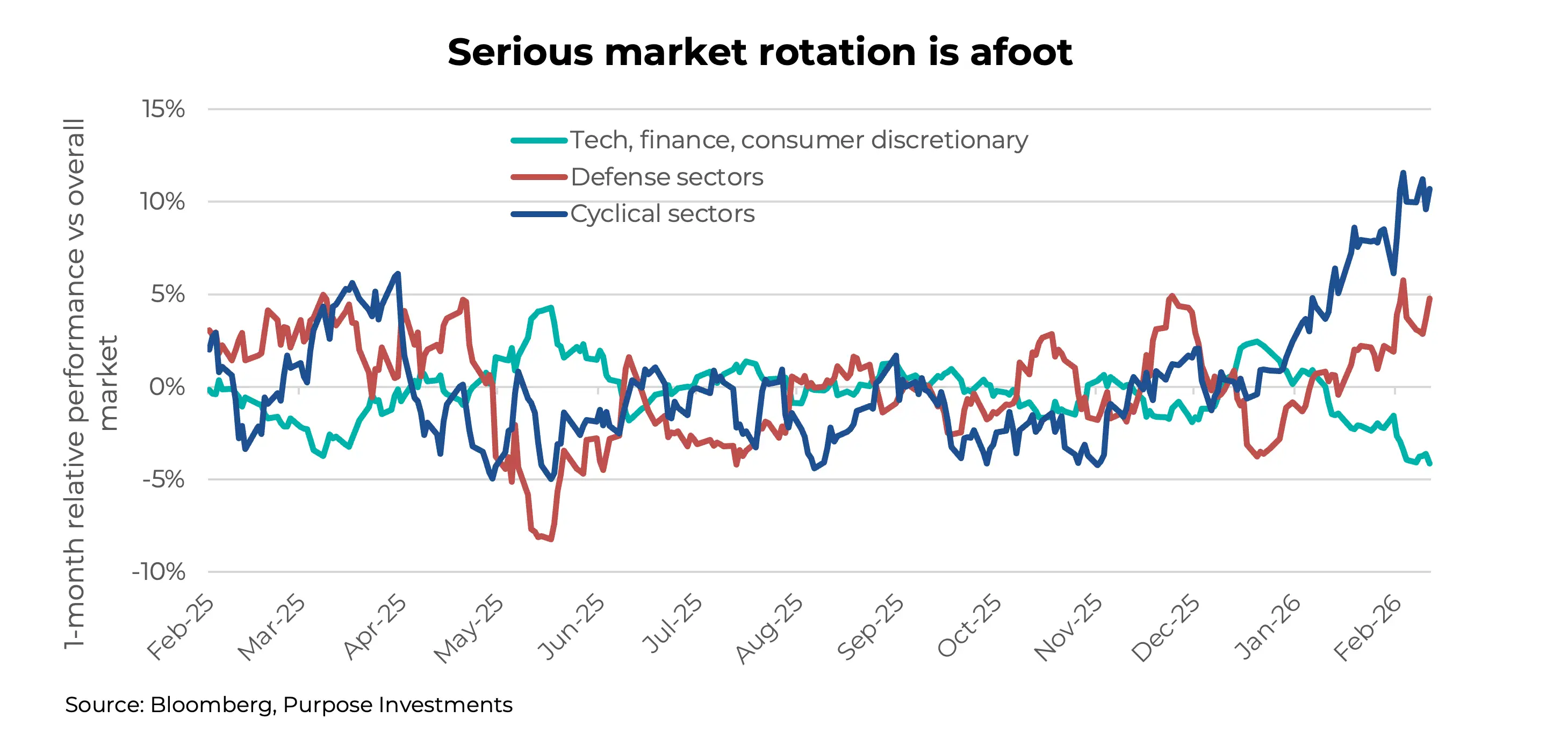

This has all created a higher level of divergence in the market. In fact, it’s a level of divergence, measuring performance dispersion among index members, that is most often seen during market selloffs. But the market aggregates are down just a bit. What has been saving the overall market from a weakening technology sector was originally the defensives in Q4 2025, including health care, consumer staples, utilities, and telcos. More recently, cyclicals from industrials, energy, and materials have been the saviours.

For all the fanfare, we should point out that the S&P 500 is currently (1:15 pm on February 13) down a paltry 1.7% from its all-time high set in late January, with the TSX down 2.0% from its all-time high set two days ago. At the headline index level, this is really just noise. But it does highlight the fragility of this market so far in 2026. Even in smaller companies that don’t influence the index much, these kinds of moves are not signs of a healthy market.

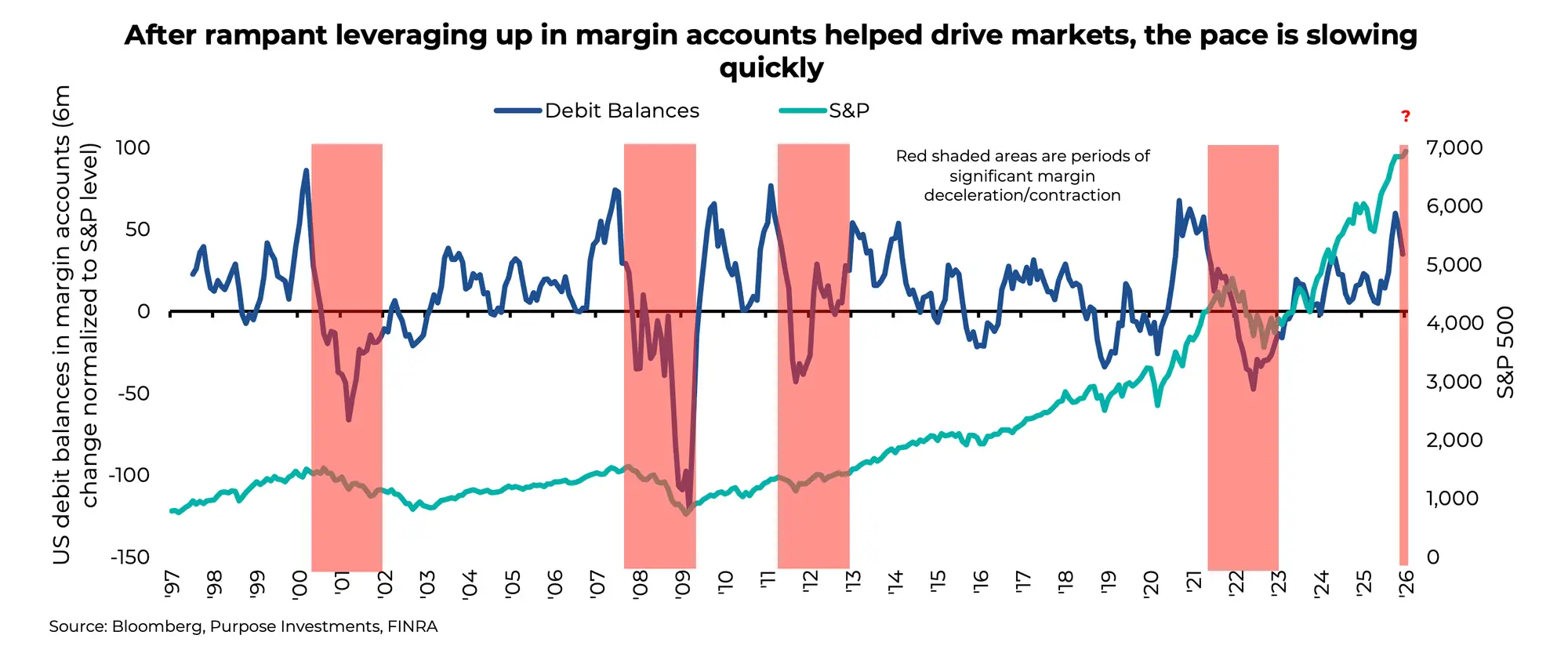

Another point of interest that supports maintaining a bit of a defensive tilt in 2026 is leverage. One factor that really helped equity markets post those strong returns in the second half of 2025 was increased leverage by investors. The chart below is the six-month change in debit balances, adjusted for the level of the S&P. This makes comparisons with years past a bit more apples-to-apples. Late last year, there was a pretty big increase in debit balances and stock ownership in margin accounts, as investors took on more leverage. The key is that when this reverses or loses upward momentum, a market reversal often follows as well. And based on the latest data point (December), the pace of margin growth has slowed.

Final Thoughts

A change in leadership, the AI wrecking ball hitting one industry after another, margin leverage starting to lose momentum, and a market that is less than a stone’s throw from all-time highs: all good reasons not to chase this market. That being said, those price reactions in various industries are clearly knee-jerk at this point, and they present potential opportunities. We’ve dabbled in both software and trucks last week.

— Craig Basinger is the Chief Market Strategist at Purpose Investments

Get the latest market insights in your inbox every week.

Copyright © Purpose Investments Inc.

Sources: Charts are sourced to Bloomberg L.P.

The content of this document is for informational purposes only and is not being provided in the context of an offering of any securities described herein, nor is it a recommendation or solicitation to buy, hold or sell any security. The information is not investment advice, nor is it tailored to the needs or circumstances of any investor. Information contained in this document is not, and under no circumstances is it to be construed as, an offering memorandum, prospectus, advertisement or public offering of securities. No securities commission or similar regulatory authority has reviewed this document, and any representation to the contrary is an offence. Information contained in this document is believed to be accurate and reliable; however, we cannot guarantee that it is complete or current at all times. The information provided is subject to change without notice.

Commissions, trailing commissions, management fees and expenses all may be associated with investment funds. Please read the prospectus before investing. If the securities are purchased or sold on a stock exchange, you may pay more or receive less than the current net asset value. Investment funds are not guaranteed; their values change frequently, and past performance may not be repeated.

Certain statements in this document are forward-looking. Forward-looking statements (“FLS”) are statements that are predictive in nature, depend on or refer to future events or conditions, or that include words such as “may,” “will,” “should,” “could,” “expect,” “anticipate,” “intend,” “plan,” “believe,” “estimate,” or other similar expressions. Statements that look forward in time or include anything other than historical information are subject to risks and uncertainties, and actual results, actions, or events could differ materially from those set forth in the FLS. FLS are not guarantees of future performance and are, by their nature, based on numerous assumptions. Although the FLS contained in this document are based upon what Purpose Investments and the portfolio manager believe to be reasonable assumptions, Purpose Investments and the portfolio manager cannot assure that actual results will be consistent with these FLS. The reader is cautioned to consider the FLS carefully and not to place undue reliance on them. Unless required by applicable law, it is not undertaken, and is specifically disclaimed, that there is any intention or obligation to update or revise FLS, whether as a result of new information, future events, or otherwise.