Here’s the thing about PIMCO’s Compounding Opportunity1: it doesn’t read like just another market outlook. It reads like a reality check.

Written by Tiffany Wilding and Andrew Balls, the piece starts from a simple but uncomfortable truth. Yes, 2025 delivered strong returns. But that strength didn’t smooth out the world — it fractured it. Economies, markets, and investors are increasingly moving in different directions. And that divergence, more than any single forecast, is where opportunity now lives.

This isn’t a “same trade, different year” outlook. PIMCO frames 2026 as a moment where discipline matters again. Where selectivity matters again. And where fixed income — long dismissed as boring or obsolete — quietly reasserts itself as a serious compounding engine.

Resilience, but Not Uniform Strength

The global economy, according to PIMCO, has held up better than expected. Big policy moves in 2025 — including a sharp increase in U.S. tariffs — failed to trigger the recession many feared. Growth, instead, proved “surprisingly resilient,” supported by policy responses and technology-driven productivity gains.

Artificial intelligence plays a central role here. Not as hype, but as infrastructure. AI-linked investment is lifting productivity and trade in very specific corners of the economy, particularly those tied to computing power and data capacity.

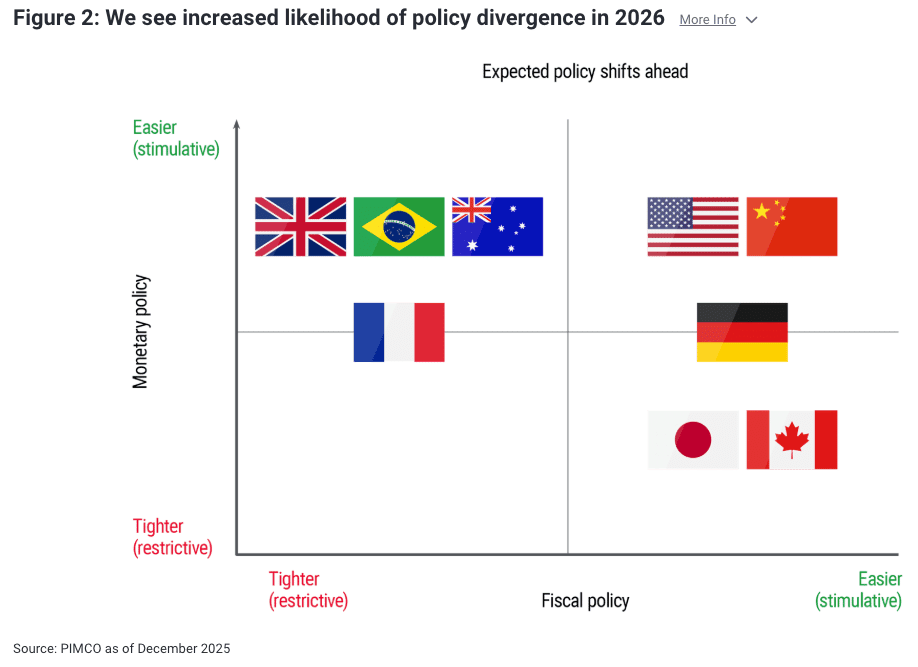

But the gains aren’t evenly shared. PIMCO points to a clear “K-shaped” outcome: capital-intensive firms and wealthier households are pulling ahead, while others lag. That imbalance isn’t just a social issue — it’s an investment signal. Divergence in outcomes creates divergence in markets.

Valuations Change the Game

If growth surprised to the upside, valuations did not. Equity markets, in PIMCO’s view, are still priced for optimism. That matters because high starting valuations tend to compress future returns.

Fixed income, by contrast, looks very different.

“Bonds are cheap versus stocks at current valuations.”

That single sentence anchors the entire outlook. After years of being overshadowed by equities, bonds now offer something rare: attractive starting yields that don’t rely on heroic assumptions to deliver compounding returns. Even after solid fixed income performance in 2025, yields remain elevated by historical standards. The opportunity didn’t disappear — it endured.

Why Active Management Matters Again

One of the strongest themes in the report is dispersion. Markets are no longer moving in lockstep. That’s bad news for blunt, passive exposures. But it’s fertile ground for active investors.

PIMCO notes that active fixed income strategies delivered some of their best results in years during 2025 — and they argue the environment ahead may be just as rich for alpha. Why? Because differences across countries, sectors, and securities are widening, not narrowing.

The opportunity set rests on three pillars: genuine global diversification, careful security selection (particularly in higher-quality credit and securitized assets), and a thoughtful approach to duration that locks in yield without overcommitting to a single rate outcome.

In short, dispersion rewards judgment.

Emerging Markets: From Category to Case-by-Case

Emerging markets are a good example of that shift. Once treated as a single risk bucket, EM fixed income now reflects a wide range of policy choices, real yield profiles, and economic backdrops.

PIMCO highlights that EM local currency bonds delivered strong returns in 2025 while also contributing meaningful diversification. The takeaway isn’t that EM is suddenly “safe.” It’s that it’s no longer one-dimensional. Selectivity turns what used to be a blunt exposure into a source of idiosyncratic value.

Credit: Constructive, but Not Carefree

The report’s tone on credit is measured. PIMCO remains constructive, but far from complacent. Tight spreads and strong recent performance are not signals to reach indiscriminately for yield. They are reminders that credit markets tend to punish laziness late in the cycle.

Here again, the message is consistent: opportunity exists, but it’s uneven. Compounding works best when investors accept that not every asset, sector, or strategy deserves equal weight.

What This Means for Advisors and Investors

First, fixed income is back — not as ballast, but as a return generator. The combination of yields and valuations creates a foundation for compounding that equities may struggle to match from here.

Second, active management matters more when markets fragment. Broad exposures smooth differences away. Skilled positioning leans into them.

Third, divergence isn’t noise. It’s the signal. Economic winners and losers, regional policy gaps, and sector-level dispersion are shaping returns.

And finally, conviction still needs discipline. Especially in credit, where selectivity matters more than enthusiasm.

Compounding, Reframed

At its core, Compounding Opportunity argues that compounding isn’t automatic. It’s not the byproduct of owning “the market” and waiting. It’s the result of engaging with a world that’s increasingly uneven — and being willing to make deliberate choices within it.

That’s the quiet shift PIMCO is pointing to. Not a new cycle. A more demanding one.

Footnote:

1 Wilding, Tiffany and Andrew Balls. "Compounding Opportunity." Pacific Investment Management Company LLC, 15 Jan. 2026.