by Nelson Yu, Head, Equities, AllianceBernstein

Our playbook for 2026 aims to address real risks by expanding allocations in new directions.

Global equities posted strong gains in 2025, driven by the US technology mega-caps. But the artificial intelligence (AI) trade wasn’t the only game in town. Surveying last year’s diverse return drivers can guide investors to a wider set of opportunities while preparing for evolving risks.

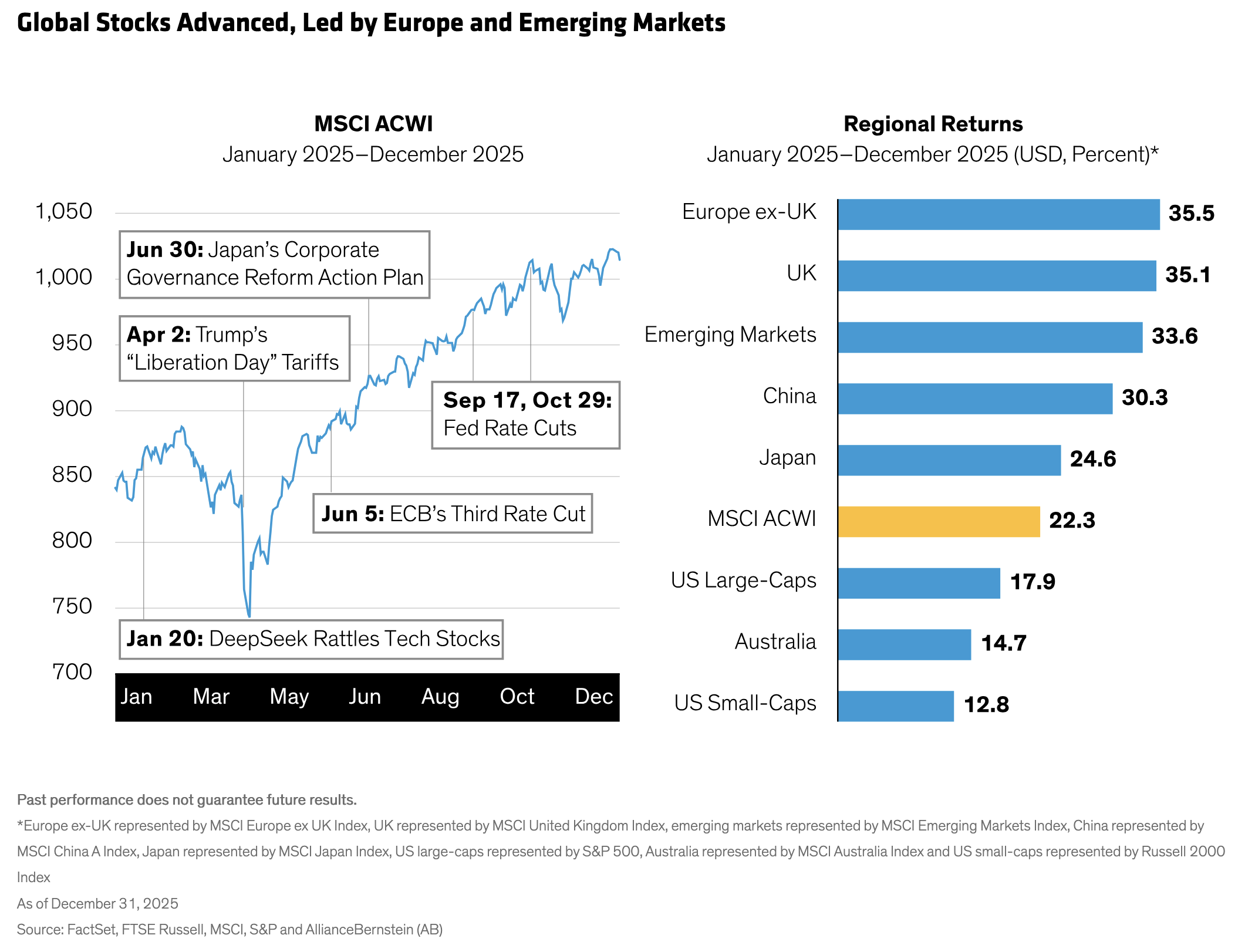

Volatile market episodes didn’t derail global equities last year, as the MSCI ACWI Index advanced by 22.3% in US-dollar terms (Display). The S&P 500 rose by 17.9%, trailing Europe, emerging markets and Japan. Although non-US returns benefited from a weaker US dollar, Japan, Europe and emerging markets outpaced the US in local-currency terms as well.

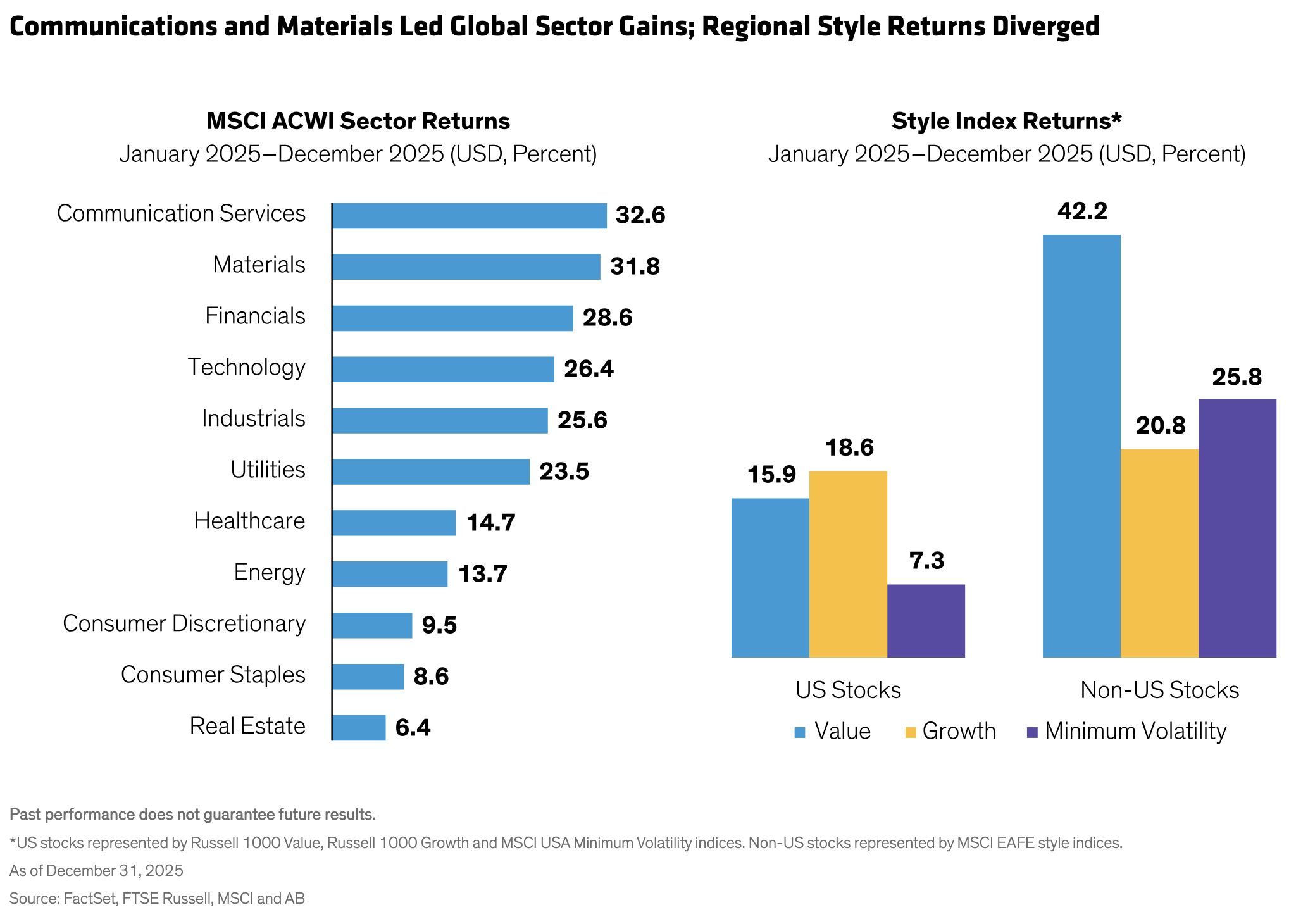

Communications and materials led global sector returns, while consumer sectors underperformed (Display). Global style returns diverged, with growth stocks continuing to lead in the US. Outside of the US, however, the MSCI EAFE Value Index surged by 42.2%—far eclipsing the performance of non-US growth stocks.

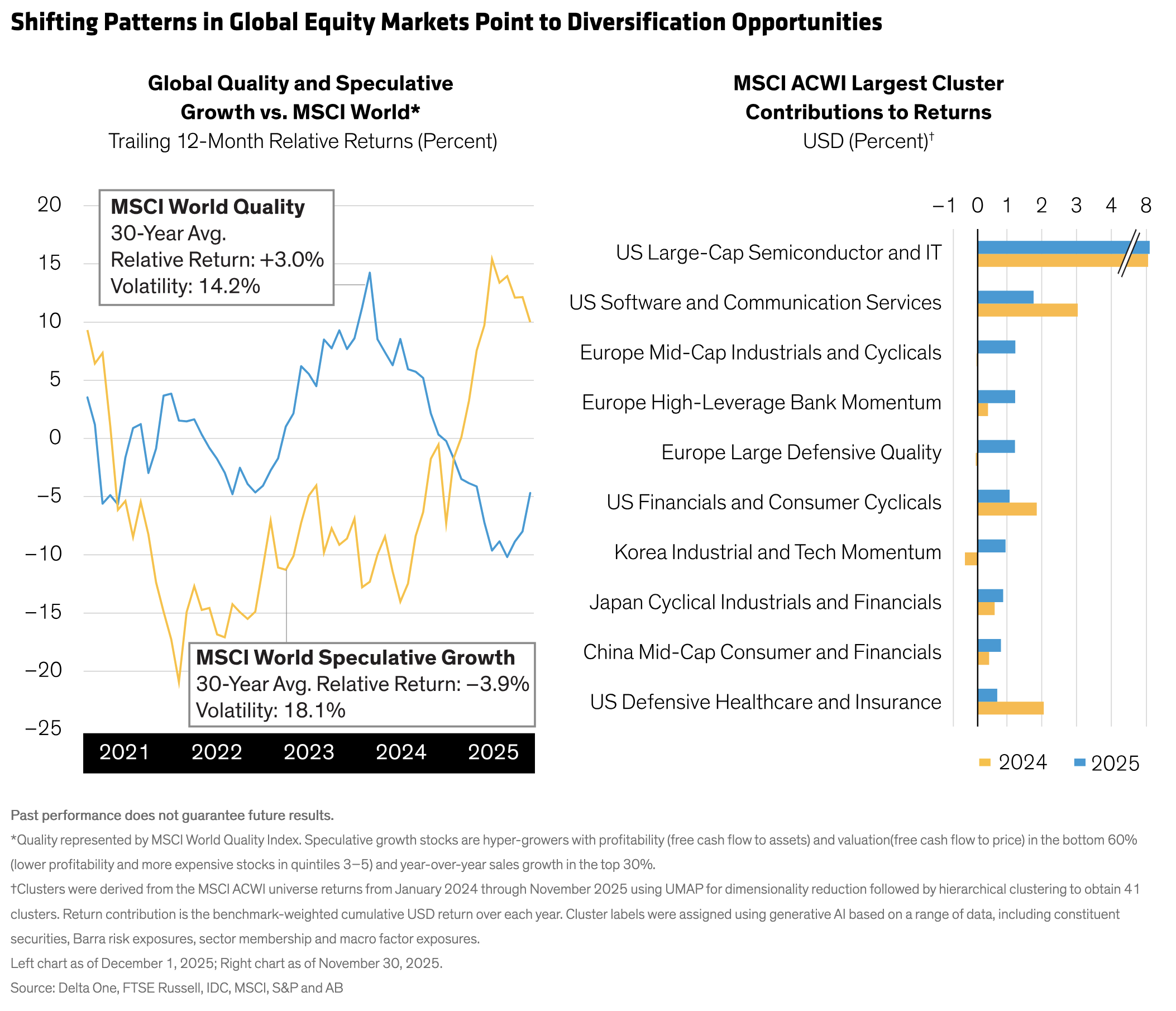

After two years of narrow performance leadership driven by the US AI hyperscalers, our cluster research shows the beginnings of a global broadening in themes in 2025 (Display). Shifting return patterns were also seen through most of last year in the weakness of quality stocks alongside a rally in speculative growth stocks, which benefited from expectations of US interest-rate cuts and the AI trade.

The speculative growth rally implies that investors are confident about the macroeconomic backdrop. Global economic growth defied abrupt policy moves and geopolitical instability in 2025, yet frictions remain beneath the surface. For 2026, AB economists project a lower risk of a significant downturn and a pickup in inflation. The moderate US expansion is facing conflicting forces, while European growth is stagnant and China is mired in a slowdown. Japan, too, faces heightened policy uncertainty as markets assess the economic agenda of newly elected Prime Minister Sanae Takaichi.

Beyond macro forces, market outcomes may be shaped in 2026 by ongoing debates over the role of US equities in a global allocation and AI—two prominent issues for the new year’s equity investing playbook.

Examining the Role of US Equities

US equities face three notable headwinds as we enter 2026: market concentration, elevated valuations and continued questions about US exceptionalism. Are the tides turning against the S&P 500, which has outperformed non-US markets in 11 of the last 15 years?

In recent years, that outperformance was spurred by the dominant technology titans, which pushed US equity market concentration close to a record high. By the end of 2025, the 10 largest stocks accounted for more than 40% of the S&P 500’s market capitalization, making diversification within US equities more challenging. It also means the performance of a handful of large-cap technology stocks can disproportionately impact overall returns and volatility. In 2025, the S&P 500’s relative volatility versus non-US markets reached a record high for the 21st century.

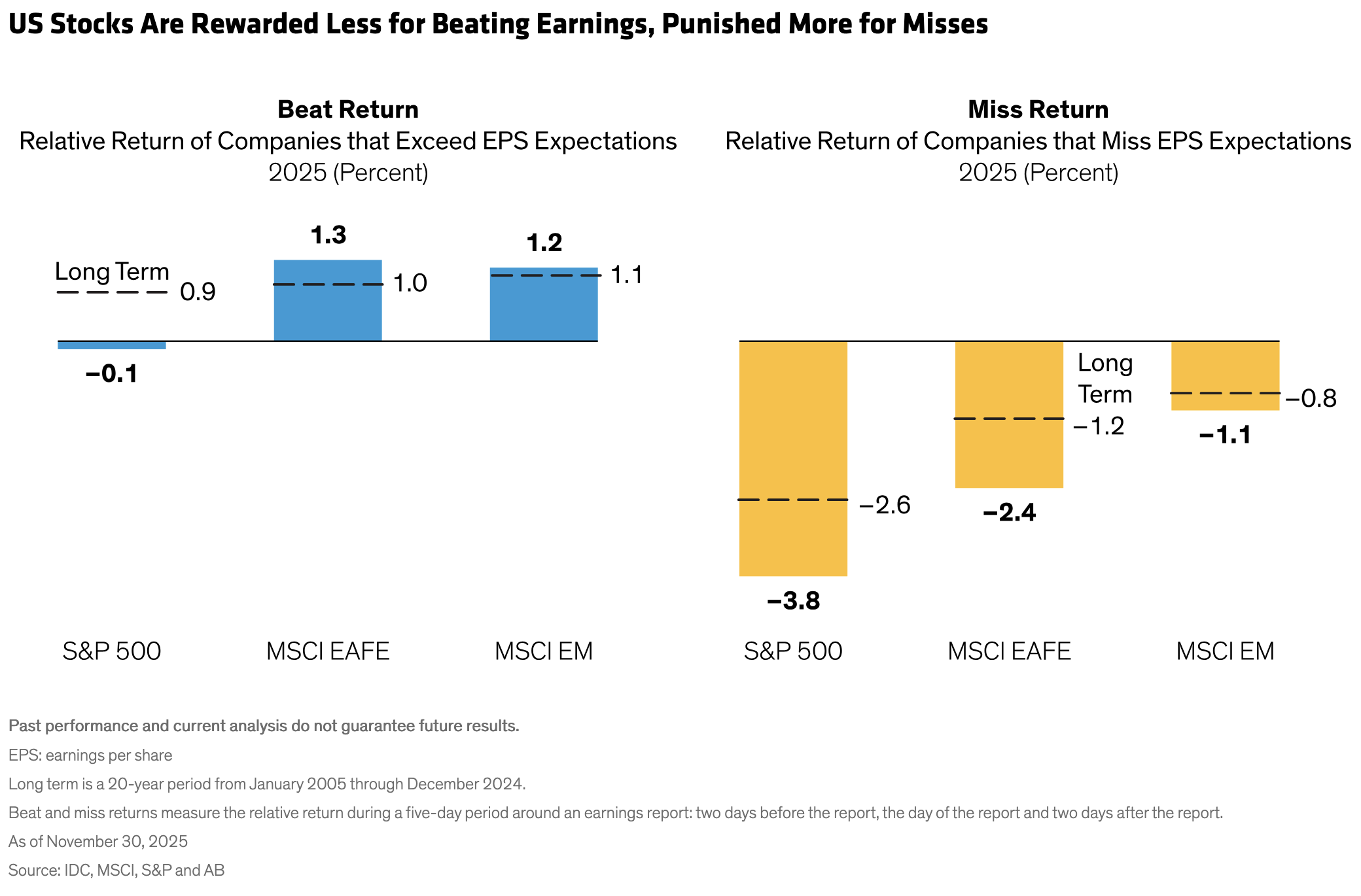

High valuations are another consequence of these dynamics. Even after trailing non-US markets last year, US equities remain relatively expensive versus global peers, which may explain why earnings season has become more erratic. Historically, when US companies delivered a positive earnings surprise, their stocks outperformed. However, beating expectations wasn’t rewarded last year, and shares of US companies that missed forecasts were hit harder. In contrast, companies outside of the US continued to enjoy positive payoffs for exceeding earnings forecasts (Display).

Meanwhile, policy uncertainty—including trade tensions, government shutdowns and concerns about Federal Reserve independence—is magnifying doubts about the durability of US exceptionalism.

We believe this pessimism may be overstated. US companies continue to benefit from deep capital markets, innovation clusters and a corporate sector with superior profitability. These advantages help explain the relatively higher valuations in the US market.

As we see it, US equities remain an important component of global portfolios, but disciplined diversification and a highly selective approach are essential. The key for investors is to uncover companies with resilient business models, strong profitability and long-term growth potential. Active management and risk-aware portfolio construction can capture exposure to world-leading US firms while mitigating the risks.

Assessing the AI–Driven Market

Concentration and valuation risks have been fueled by enthusiasm for AI. The dominance of a small group of AI–driven mega-cap stocks has intensified the debate around active and passive investing.

AI’s rapid growth may unlock productivity gains and return potential, but transformational technology comes with considerable risks. Today, as the hyperscalers pour hundreds of billions of dollars into infrastructure capex, more questions are being asked about their future return on investment and whether we’re in an AI bubble.

Given the scale of spending, bubble fears are understandable. That said, capex in public markets is mostly being financed from free cash flow rather than debt, which should help alleviate potential stresses. However, the next phase of AI is being financed by less stable sources, including circular deals between large players and private-credit structures that could be more vulnerable.

Despite the risks, we don’t think long-term investors can stay on the sidelines. AI is making a pervasive impact across businesses and markets. As a result, we think investors should search beyond the mega-caps across the entire AI ecosystem for future winners, from early enablers to semiconductor suppliers and software firms building new architectures. Opportunities will also emerge among a broader range of companies that will become consumers and beneficiaries of AI.

Active portfolios should hold technology mega-caps based on a critical evaluation of their business models and valuations, in our view. Each stock should be appropriately weighted in line with an investing philosophy. That means a selective approach toward the heavyweight mega-caps and a sober assessment of their spending and profitability paths.

As AI broadens, we think investors should have diversified exposure across business models, industries and regions. Remember that the early winners in the dot-com boom don’t rule the web today and expand the search for companies that could become tomorrow’s leaders.

Three Investing Guidelines for 2026

How do these developments frame an equity investing plan for 2026? In an environment of sluggish macroeconomic growth, US policy uncertainty and AI–driven market dynamics, we think the following guidelines should shape a long-term strategy:

- Seek active approaches to curb volatility. Complacency about volatility is a risk following a strong year for equities. US market dynamics and AI controversies could provoke turbulence in 2026. For example, the mega-caps will face heightened scrutiny and any AI–related disappointments may prompt equity declines.

So how can investors prepare? First, don’t assume that the mega-caps will help curb losses in a downturn. Second, consider adding defensive equity strategies to your allocation—including in the US. Third, take advantage of the diversification that comes from the broader set of themes that are poised to deliver returns in a global investment universe.

- Cast a wider net for long-term return potential. Regional diversification isn’t just a risk-control tool—it’s a source of differentiated returns to help fight concentrated leadership. This year reminded us that equity return sources are dynamic—even after a dominant US decade.

For investors who are overweight US stocks, consider expanding toward non-US markets, where the revival of value stocks offers diversification to popular US growth allocations. Capital discipline in Europe and corporate governance reform in Japan can add uncorrelated sources of returns. Emerging markets may benefit further from a weaker US dollar as well as themes including digitization and China’s anti-involution plans.

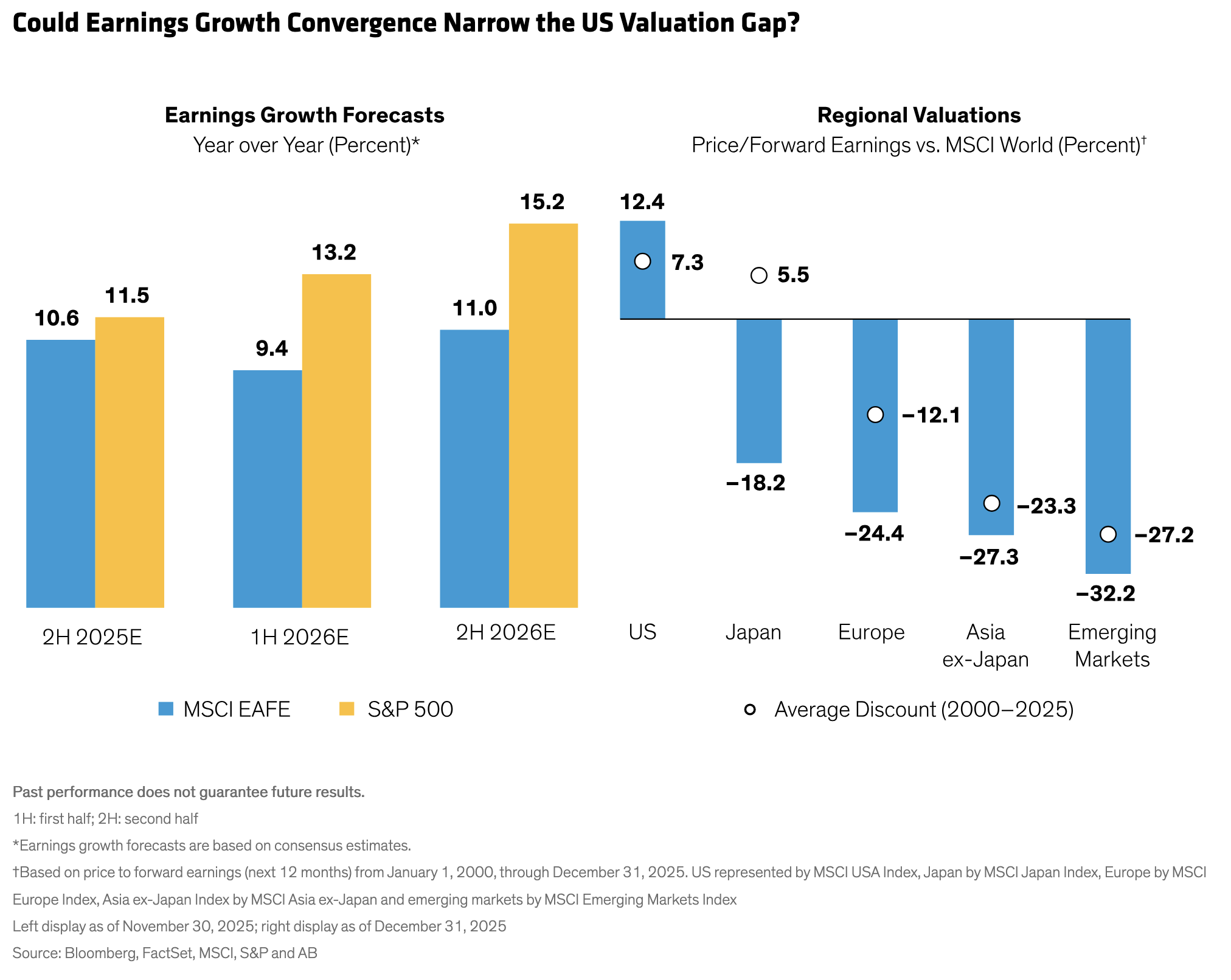

Amid global uncertainties, the outlook for earnings growth is uneven. Beneath the surface of lackluster earnings growth outside of the US is a more complex picture. Although European earnings expectations are relatively suppressed, earnings growth forecasts for Japan and emerging markets are trending upward. Earnings gains in select companies outside of the US—where valuations are relatively attractive—could spur multiple expansion that would augment market gains (Display).

To be sure, US equities remain an integral component of a well-rounded global allocation, but we believe investors should tap a wider range of US opportunities. Improving earnings growth in US sectors such as healthcare, industrials and financials suggests equity returns can extend into a wider array of market segments. - Double down on quality. Even after recent disappointments, don’t give up on resilient companies that can sustain profitability. Our research suggests that quality companies with consistent profitability and resilient business models tend to outperform over time. High-quality companies can also sustain earnings growth independent of macro conditions.

Short-term lapses in quality stock performance don’t necessarily signal a fundamental erosion of long-term potential. In our view, earnings and cash flows are still the best predictor of equity returns over long time horizons. If we see higher volatility and weaker tailwinds in 2026, we believe quality stocks could become even more valuable in a portfolio.

As the new year begins, equity investors are at a critical juncture. Policy uncertainty, macroeconomic hurdles and AI have added meaningful challenges to long-term wealth creation.

Now’s the time to ensure that current exposures are well aligned with long-term strategic allocations. Make sure your return sources are complementary across a spectrum of regional, style and thematic return drivers. Tapping into a truly diverse range of equities is the best way to capture long-term return potential while staying on guard for a growing array of global risks.

The MSCI data may not be further redistributed or used as a basis for other indices or any securities or financial products. This report is not approved, reviewed or produced by MSCI.

*****

About the author

Nelson Yu is a Senior Vice President, Head of Equities and a member of the firm’s Operating Committee. As Head of Equities, he is responsible for the management and strategic growth of AB’s equities business and investment decisions across the department. Since 1993, Yu has experience generating investment success in global equity markets by joining fundamental research with rigorous quantitative methods. He joined AB in 1997 as a programmer and analyst, and served as head of Quantitative Equity Research from 2014–2021. Since 2017, Yu also served as head of Multi-Style Core Equity strategies, with over $10 billion in assets. Most recently, he was CIO of Equities Investment Sciences and Insights, which brings together resources across Data Science, Quantitative Research, Advisory Services, Risk and Global Execution to deliver differentiated capabilities and insights to AB’s equities investment platform. Prior to joining AB, Yu was a supervising consultant at Grant Thornton. He holds a BSE in systems engineering from the University of Pennsylvania and a BS in Economics from the Wharton School at the University of Pennsylvania. Yu is a CFA charterholder. Location: New York