by Sammy Suzuki, CFA, Head—Emerging Markets Equities, Christian DiClementi, Portfolio Manager—Emerging Market Debt, AllianceBernstein

Emerging-market assets have benefitted from a softer dollar, which could remain weak for a while.

The US dollar (USD) has weakened over the last few months, fueling strong emerging-market (EM) stock and bond returns in 2025. Now, with more clarity around tariffs and the record-long US government shutdown resolved, will the greenback strengthen and flip the script on EM? We don’t think so.

Investors in EM have enjoyed a bumper year. The MSCI Emerging Markets Index surged by 33% in USD terms through October 31, nearly double the S&P 500’s return. Meanwhile, the J.P. Morgan Emerging Markets Bond Index rose 13%. After such strong gains, it’s a good time to gauge the forces affecting the dollar and their influence on EM stocks and bonds.

Six Forces Weighing on the Dollar

Several indicators suggest the USD weakness will continue.

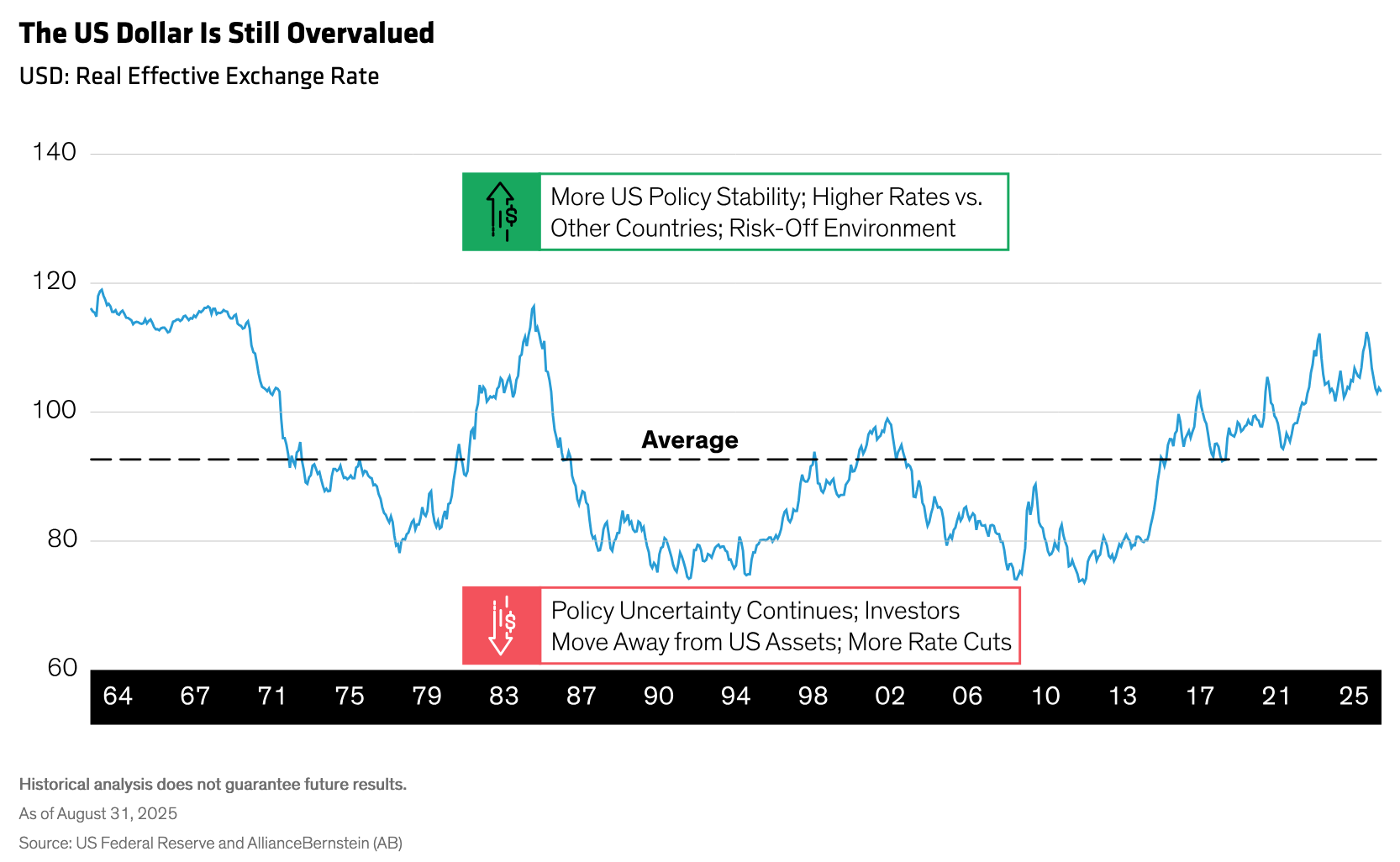

- Weak or strong, currency cycles tend to last years, not months. Since 1983, periods of dollar appreciation and depreciation alike have lasted about 10 years (Display). In this context, the USD is still relatively strong versus its long-term history, which is why we believe today’s weak cycle is likely just getting started and may last a while longer.

- Major central banks are gradually moving away from the USD to diversify reserves. For instance, China and Russia, historically among the largest USD investors, have shed considerable dollar holdings in recent years. A combination of shrinking demand, greater supply and negative market sentiment would tend to depreciate the currency over time.

- Foreign investors could be deterred by growing US deficits, which are at historical peacetime highs. Combined with America’s more internally focused policy, US debt may drive foreign investors to hold less US currency, or US assets in general, versus history.

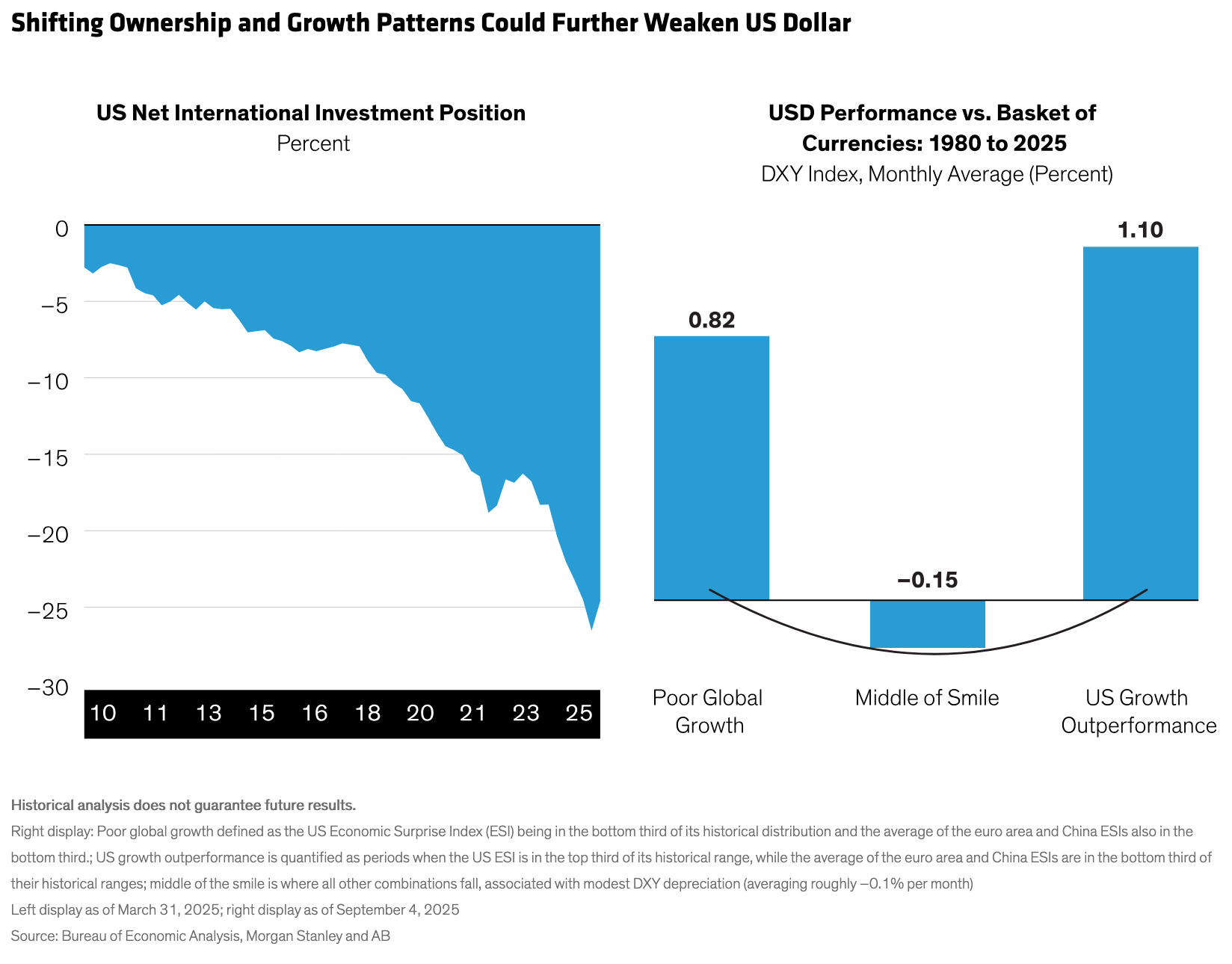

- Global investor overweight to USD-denominated assets leaves room to rebalance away from the currency. Foreign ownership of USD-denominated investments is near all-time highs. In fact, more foreigners invest in US assets than Americans invest overseas, as indicated by the –26% of GDP for the US net international investment position (Display). Since a weak USD shrinks the value of US assets in non-US currency terms, we think this may prompt more foreign investors to allocate away from US-denominated assets, potentially toward EM opportunities.

- The interest-rate differential between the US and other countries may start to narrow, which tends to weaken the USD. Historically, when interest-rate differentials widened, the dollar consistently strengthened (except briefly during April’s tariff turmoil). But with trade policy less fuzzy and the US Fed easing again, old patterns are reappearing. If the US cuts rates more than other developed markets, as we expect, the shrinking interest-rate differential should prompt further USD weakness.

- The greenback has historically softened when US growth aligns with other developed countries, which is currently the case. AB economists forecast US real GDP at a sluggish 1.7% for 2026, but relatively consistent with the 1.2% expected for other industrial countries. However, when the US outperformed or the global economic environment deteriorated, the dollar appreciated. The two upside extremes form the bookends of a so-called “dollar smile” (first advanced by Stephen Jen at Morgan Stanley), at which USD performance is currently at its smack-center weakest spot (Display, above).

How Does a Weaker Dollar Help EM Assets?

EM assets benefit from a falling dollar for three reasons:

- A weaker dollar can attract more inflows as investors seek higher returns in a depreciating-dollar environment, potentially stimulating corporate and economic growth as well.

- Bond issuers benefit when their debt-servicing costs drop, since many EM sovereigns and corporate bonds are denominated in US dollars.

- Commodities prices, a key driver across many EM economies, tend to rise when the dollar weakens—another potential tailwind.

Nobody knows whether the USD will continue to fall, particularly with US policy in flux and the Fed under pressure from the Trump administration. For now, however, the dollar continues to trend weaker, which history has shown is a boon to EM assets.

The Dollar and Emerging Markets: A Look Back

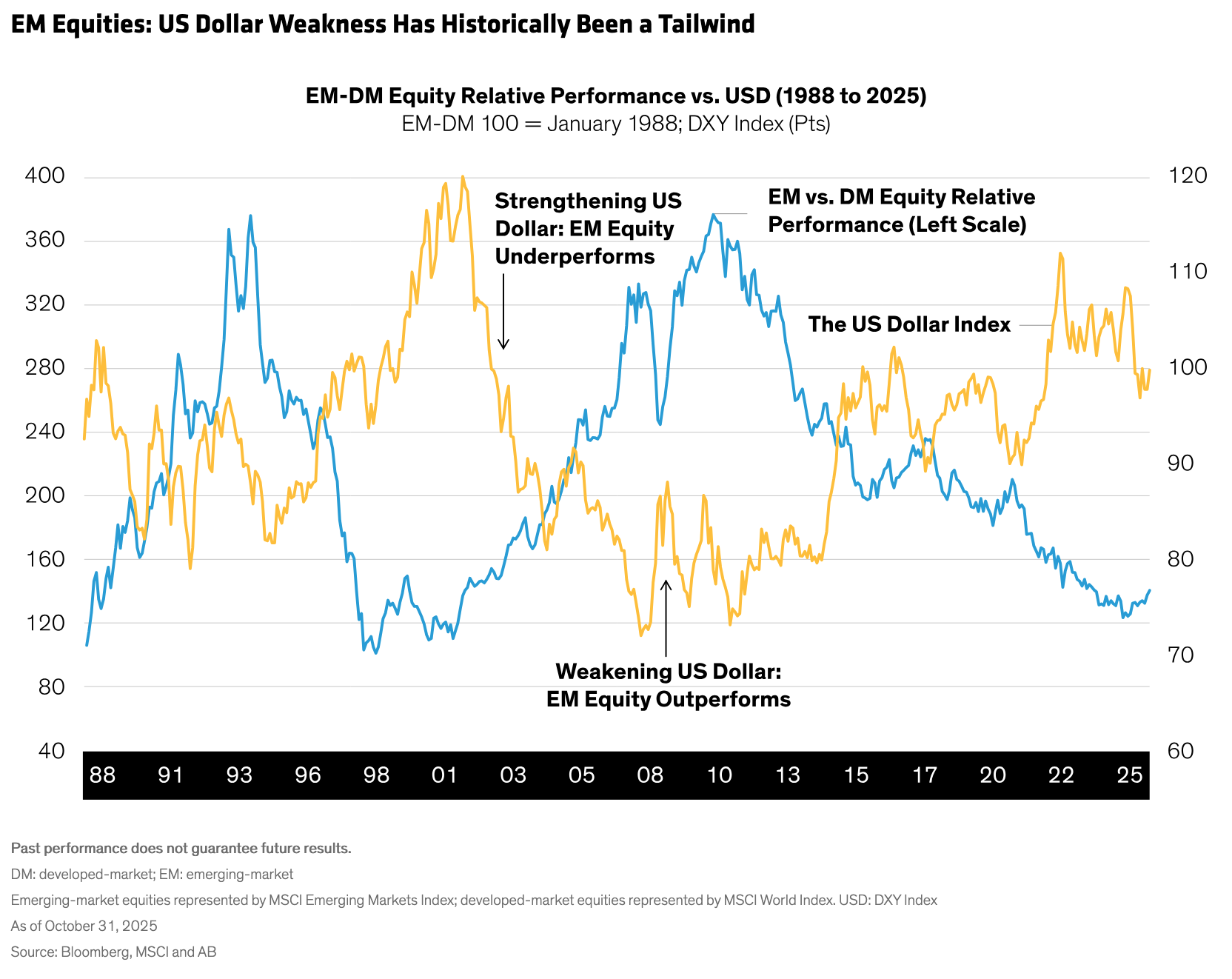

The USD’s valuation path in the last two decades especially supports our case for EM assets (Display). EM stocks, for instance, outperformed developed-market equities as the dollar weakened or stabilized from 2004 to 2011.

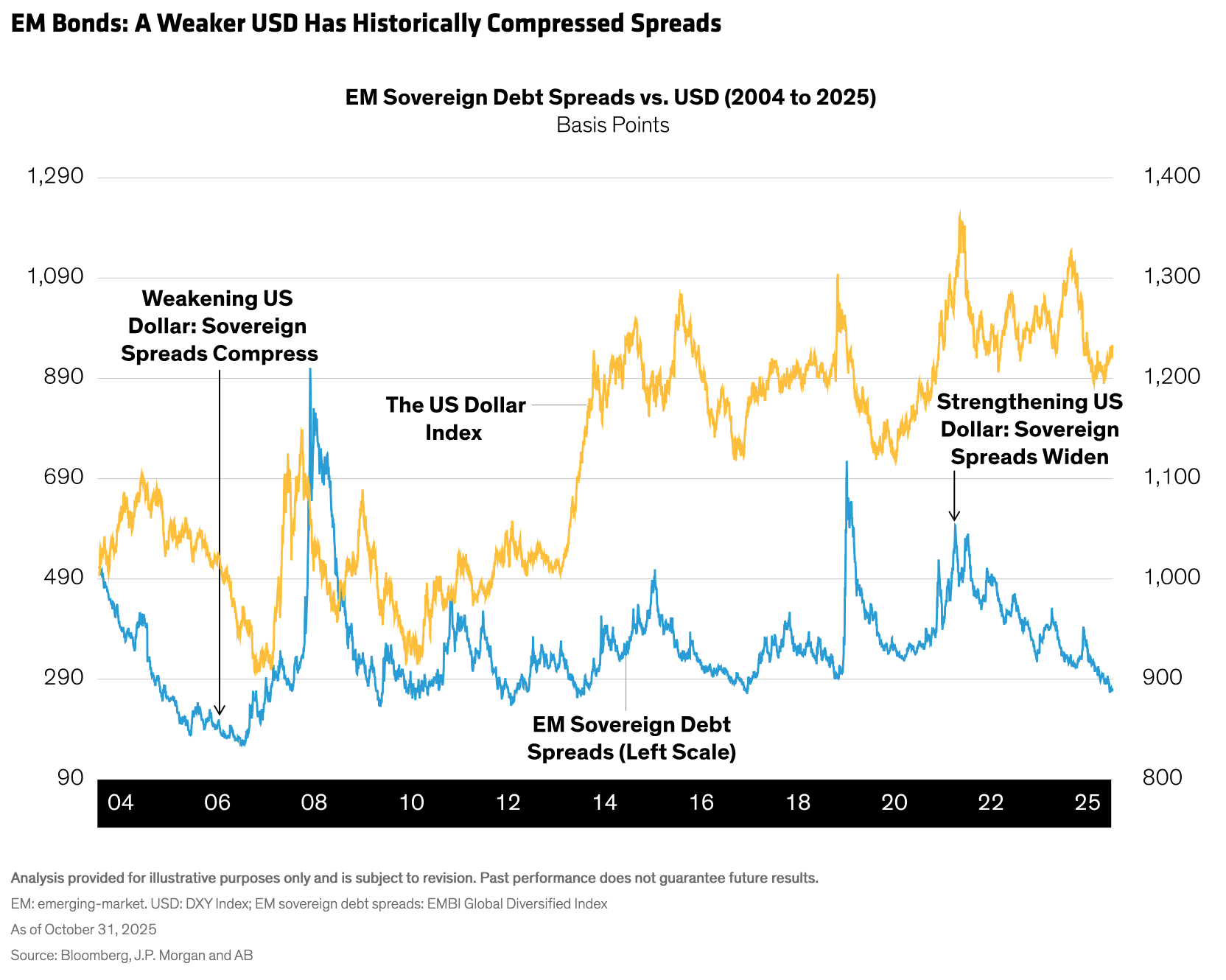

The weakening USD has also compressed bond spreads, since default risk tends to ease when debt servicing cheapens. We saw this when EM sovereign spreads narrowed for most of the 2000s—and the opposite, with spreads widening when the USD strengthened from 2014 to 2016 and in 2022 (Display). Today, sovereign spreads are their lowest since 2007 and corporate spreads remain tight versus their 15-year averages. Still, we think EM bonds offer attractive valuations for selective investors—and prices could rise relative to US Treasuries should spreads compress further.

Despite its 2025 slide, the greenback is still historically expensive compared with most currencies and conflating conditions suggest it might soften further. Either way, we’ve seen the dollar’s softening support EM assets throughout most of 2025, and there are now even more reasons to believe these trends will continue.

Currency dynamics could be a catalyst that augments the broad opportunity set across equities, sovereigns and corporate bonds. With US exceptionalism now under more scrutiny, we think investors who are underweight EM assets should reevaluate their positions and consider diversifying toward evolving opportunities across the developing world.

The MSCI data may not be further redistributed or used as a basis for other indices or any securities or financial products. This report is not approved, reviewed or produced by MSCI.