Canadians have never looked richer on paper—and yet, strangely, many have never felt more exposed. Over the last thirty years, household wealth has ballooned. People own more real estate, more financial assets, and more savings vehicles than ever before. But underneath that growth is a quieter, far more troubling reality: we’ve handed everyday Canadians full responsibility for managing their financial lives without giving them the skills to do it confidently.

Workplace pensions are disappearing. DIY retirement planning has gone mainstream. And financial products keep multiplying in complexity. What used to be handled by large institutions is now sitting in the laps of individuals—many of whom aren’t ready for the job.

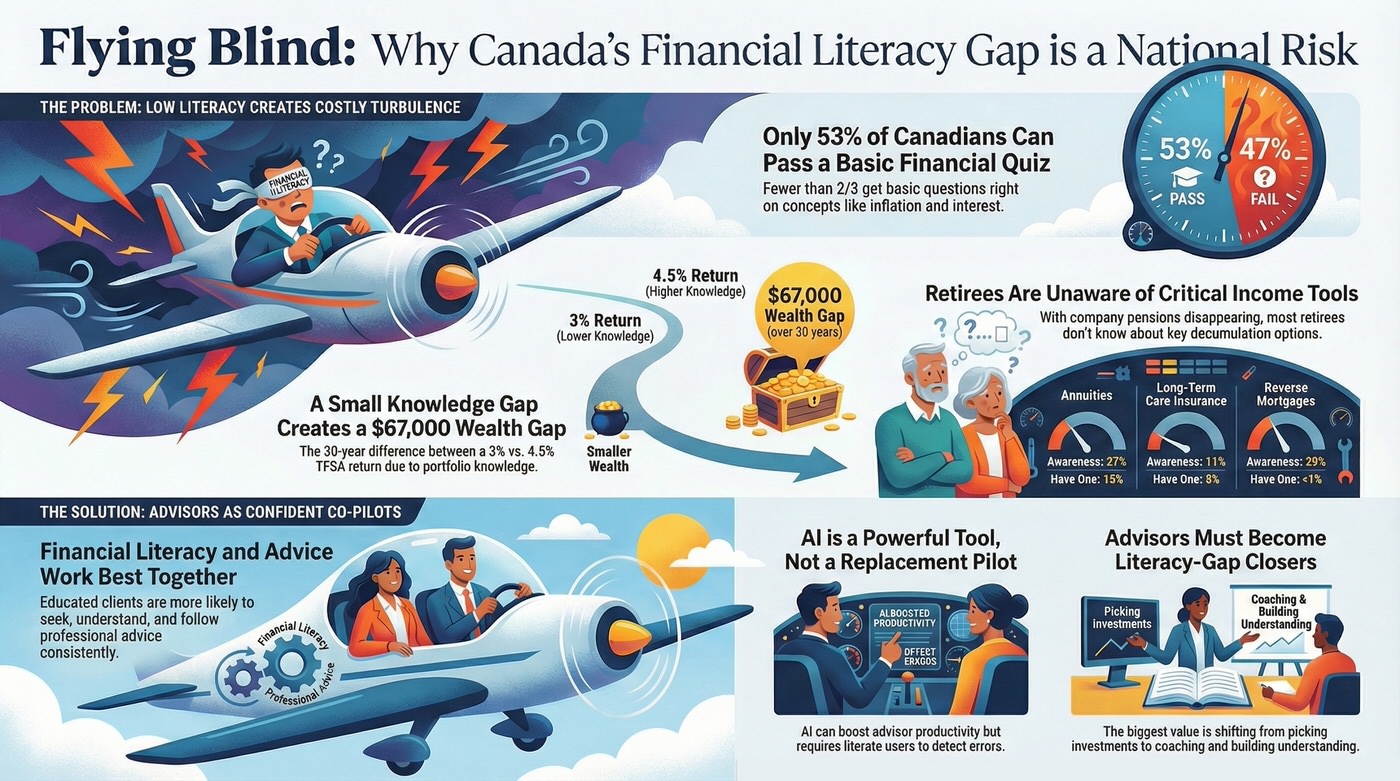

The latest C.D. Howe Institute report1 sums it up perfectly: Canadians are “in the cockpit,” but most still don’t know how to fly the plane.

And the air is getting choppier.

The Hidden Fault Line: Financial Literacy Is Stuck in Neutral

Despite years of updated school curriculums and national campaigns, Canada’s financial literacy levels haven’t moved much—and the baseline isn’t great.

When tested on six simple concepts (compound interest, inflation, bond pricing, debt doubling, diversification, and mortgages), fewer than two-thirds of Canadians get the answers right, and only 53% can answer more than half correctly.

These aren’t niche topics. They’re the financial equivalent of reading your fuel gauge.

The gaps become even more glaring when we look at Canada’s core savings tools. Understanding how RRSPs and TFSAs work—taxes, withdrawals, contribution rules—is surprisingly low. Less than 26% of Canadians answer more than half of six basic account questions correctly.

And because of that, the RRSP-vs-TFSA decision—which is often worth tens of thousands of dollars over a lifetime—is being treated like a coin flip.

Lack of knowledge doesn’t just create confusion. It quietly chips away at long-term wealth. And that erosion is already happening.

Low Literacy = Costly Mistakes That Compound for Decades

The report taps into real tax data, and the picture isn’t flattering: most Canadians earn significantly lower returns inside their TFSAs than they should.

Across ten years, average TFSA returns sit around 2.7%–3.0%—well below the ~4.6% you’d expect from a basic 40/60 portfolio.

On paper, that gap looks small. In real life, it’s huge.

A Canadian who saves $5,000 a year for 30 years at 3% ends up with about $238,000. At 4.5%, the same person retires with roughly $305,000. That’s a $67,000 difference, simply because one person understood the basics of building a diversified portfolio—and the other didn’t.

Higher-income Canadians tend to score better on literacy—and, unsurprisingly, earn better portfolio results. The literacy divide is starting to shape the wealth divide.

And the challenge doesn’t end when people stop working. In fact, it gets harder.

The Decumulation Dilemma: No More Autopilot

With private-sector defined benefit pensions collapsing from 31% coverage in 1980 to under 10% today, retirees now carry the full responsibility of turning savings into income that lasts.

But awareness of key retirement tools is very low:

- Annuities

- 27% know they exist

- 12% have one

- Long-term care insurance

- 11% awareness

- 3% take-up

- Reverse mortgages

- 29% awareness

- less than 1% usage

These tools matter deeply in a world where people live longer, healthcare costs rise faster, and home equity often becomes the largest retirement asset. Yet most retirees don’t know how they work—or that they exist.

Even incentives designed to improve retirement outcomes don’t work as intended. The option to delay CPP/QPP for higher lifetime income barely moves the needle among lower-literacy Canadians.

The pattern is clear: high-stakes retirement decisions are being made with low-stakes understanding.

Advisors Aren’t Replacement Pilots—They’re Co-Pilots

A standout message in the report: financial literacy and financial advice work best together.

Clients who understand the basics are more likely to:

- seek advice proactively

- follow plans consistently

- evaluate recommendations with confidence

- spot advice that may not align with their needs

Advisors often talk about the value of behavioural coaching, but coaching works best when clients have enough baseline knowledge to engage meaningfully.

And as advisors lean into more sophisticated modelling, planning, and risk analysis tools, that baseline matters even more.

Which brings us to AI—the newest cockpit instrument on the dashboard.

The AI Moment: A Boost, Not a Substitute

The report takes a practical, grounded view of AI’s role in personal finance. It sees enormous potential—but only if literacy isn’t neglected.

Where AI shines:

- delivering real-time education at the moment of decision

- handling pre-meeting analysis and data gathering

- improving the quality and consistency of recommendations

- increasing advisor productivity

Where AI struggles:

- hallucinations

- inconsistent accuracy

- poor auditability

- limited ability for low-literacy users to detect bad output

The message is simple: AI is powerful, but it needs literate users and human oversight.

For advisors, that’s great news. As AI takes over routine tasks, advisors can double down on the human side of advice—coaching, clarifying, contextualizing, and guiding long-term behaviour.

A Fragmented System Without a Clear Leader

One reason literacy gains have stalled is structural: no single institution in Canada “owns” the responsibility of helping Canadians understand the financial system.

Retirement planning, tax rules, savings incentives, and consumer protections are split across multiple levels of government, regulators, and agencies.

The report calls for a centralized leader—potentially the Financial Consumer Agency of Canada—to build cohesive tools, dashboards, and AI-enabled educational support.

Canadians need something akin to a flight simulator before they’re expected to take off.

For Advisors: This Is a Leadership Moment

The shift from institution-led to self-managed financial decision-making is permanent. And literacy is not catching up fast enough.

That gap creates a powerful opening for advisors to lead.

Be the literacy-gap closer. Be the behavioural coach. Be the one who helps clients read the dashboard clearly.

People aren’t just looking for someone to pick investments anymore. They’re looking for someone who helps them understand, simplify, and navigate the entire financial journey.

Advisors who step into that role will create deeper trust, stronger relationships, and more resilient outcomes—across generations.

Conclusion: Teach Canadians to Fly Before the Skies Get Rougher

At its core, the C.D. Howe message is unmistakable:

Financial literacy isn’t optional. It’s the infrastructure everything else relies on.

Without it, households will continue making suboptimal decisions, advisors will face greater coaching challenges, and policy tools won’t deliver on their promise.

Canada has world-class building blocks—public pensions, private savings vehicles, highly trained advisors, and emerging AI tools. What we lack is a national strategy that brings it all together.

The turbulence may not be avoidable. But with the right preparation, Canadians won’t have to face it alone.

Footnote:

1 Michaud, Pierre-Carl, and Bernard Morency. Learning to Fly: How Canadians Can Navigate a More Complex Financial Landscape. C.D. Howe Institute, Commentary no. 698, Nov. 2025. PDF.

Copyright © AdvisorAnalyst.com