by George Ullstein, Portfolio Manager, Global Equity & Growth, AllianceBernstein

Detecting the real drivers of equity risk today starts with a critical look at traditional portfolio theory.

In today’s equity markets, investors face a paradox: share price swings are more dramatic than ever yet often have little to do with a company’s underlying health or earnings. So how can investors achieve true diversification and risk reduction in a world driven by fickle market forces?

Modern Portfolio Theory (MPT), introduced by Harry Markowitz in 1952, revolutionized investing by showing that diversification could optimize the trade-off between risk and return. By combining assets with imperfectly correlated returns, investors can achieve higher expected returns for a given level of risk—or lower risk for a desired level of return.

The Intuitive Appeal of Traditional Risk Concepts

To quantify risk, Markowitz settled on the idea of variance as a proxy. This has intuitive appeal: an asset price that moves erratically suggests uncertainty, which introduces the possibility of permanent loss, or ‘risk.’ Over time, numerous academic papers proved the historical validity of this linkage.

Diversification is similarly appealing. We’ve all been told from an early age never to place all our eggs in one basket. Mountains of empirical evidence support the intuition.

But not so fast. Although MPT makes sense, we believe several behavioral and fundamental factors have eroded the theory’s core tenets and raise questions about its application today.

Technical Forces Fuel Volatility

Trading trends in recent years have rattled risk concepts. The retail trading fervor stoked by COVID lockdowns has been intensified by trading platforms that increase access to derivatives. Since 2016, the total traded value of US over-the-counter equity-linked products has jumped by 64%, according to data from the Bank for International Settlements. Retail traders drove the surge using zero-day options, which reached an average daily record of 2.7 million contracts in October, according to the Options Clearing Corporation.

Zero-day options amplify investor leverage and create rapid feedback loops. Dealers hedge their positions, which affects option prices and necessitates further hedging. This process intensifies at market close, increasing stock-price volatility.

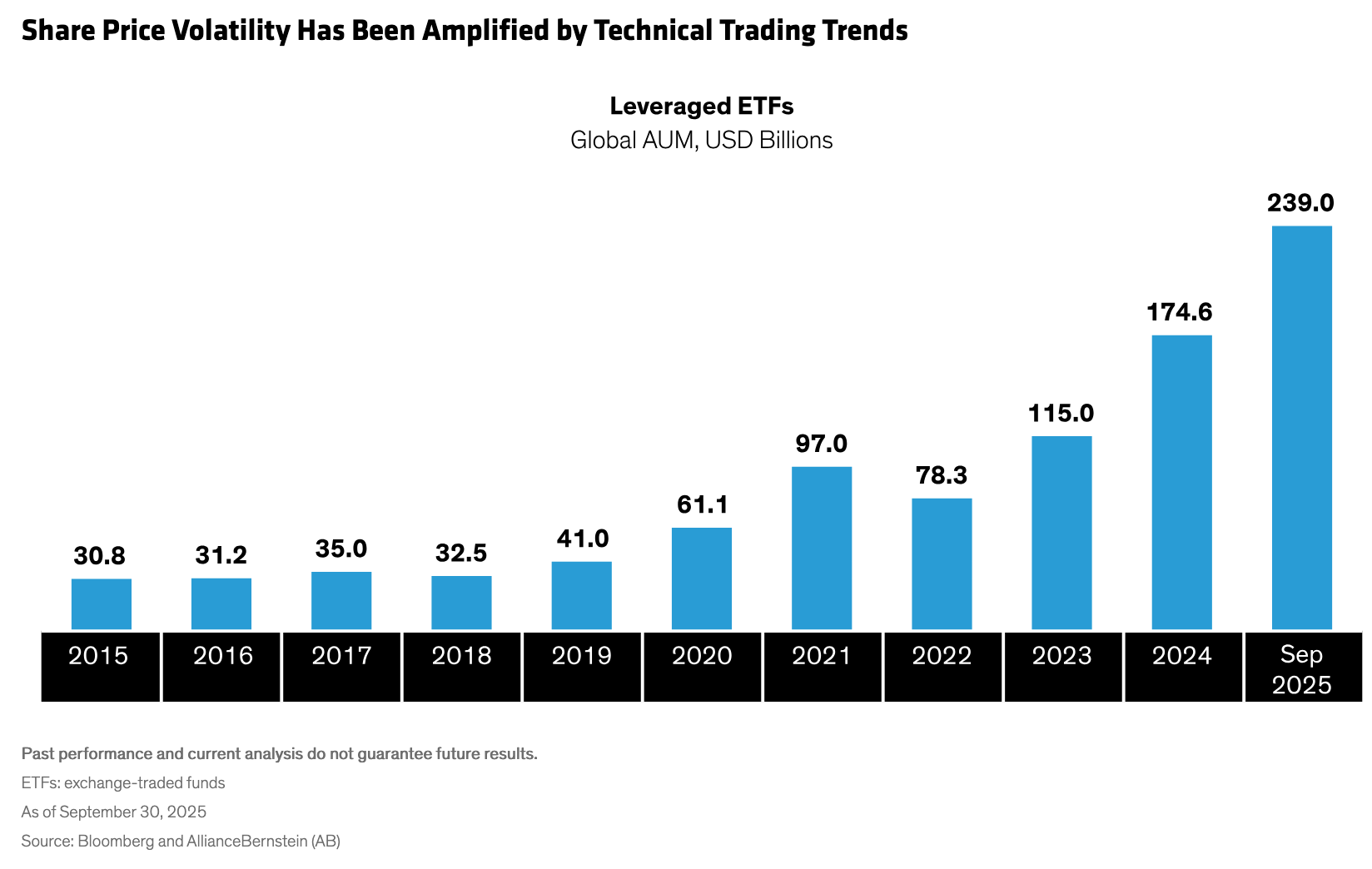

Leveraged exchange-traded funds (ETFs) have also fueled instability. These instruments, which reached a record $239 billion assets under management in September (Display), also create feedback loops; as markets rise, ETF exposure shrinks so the funds must buy, pushing the market higher. Here, too, most activity takes place at the market close when ETFs rebalance, augmenting price volatility.

In both cases, the resulting equity volatility has little or no connection to the underlying company’s earnings. So, if variance as a proxy for risk is not what it used to be, what about diversification?

GICS Classifications Are Fallible

Many investors diversify by mapping portfolios to an index, broken down by sector and country under the Global Industry Classification Standard (GICS), a system developed by MSCI and S&P.

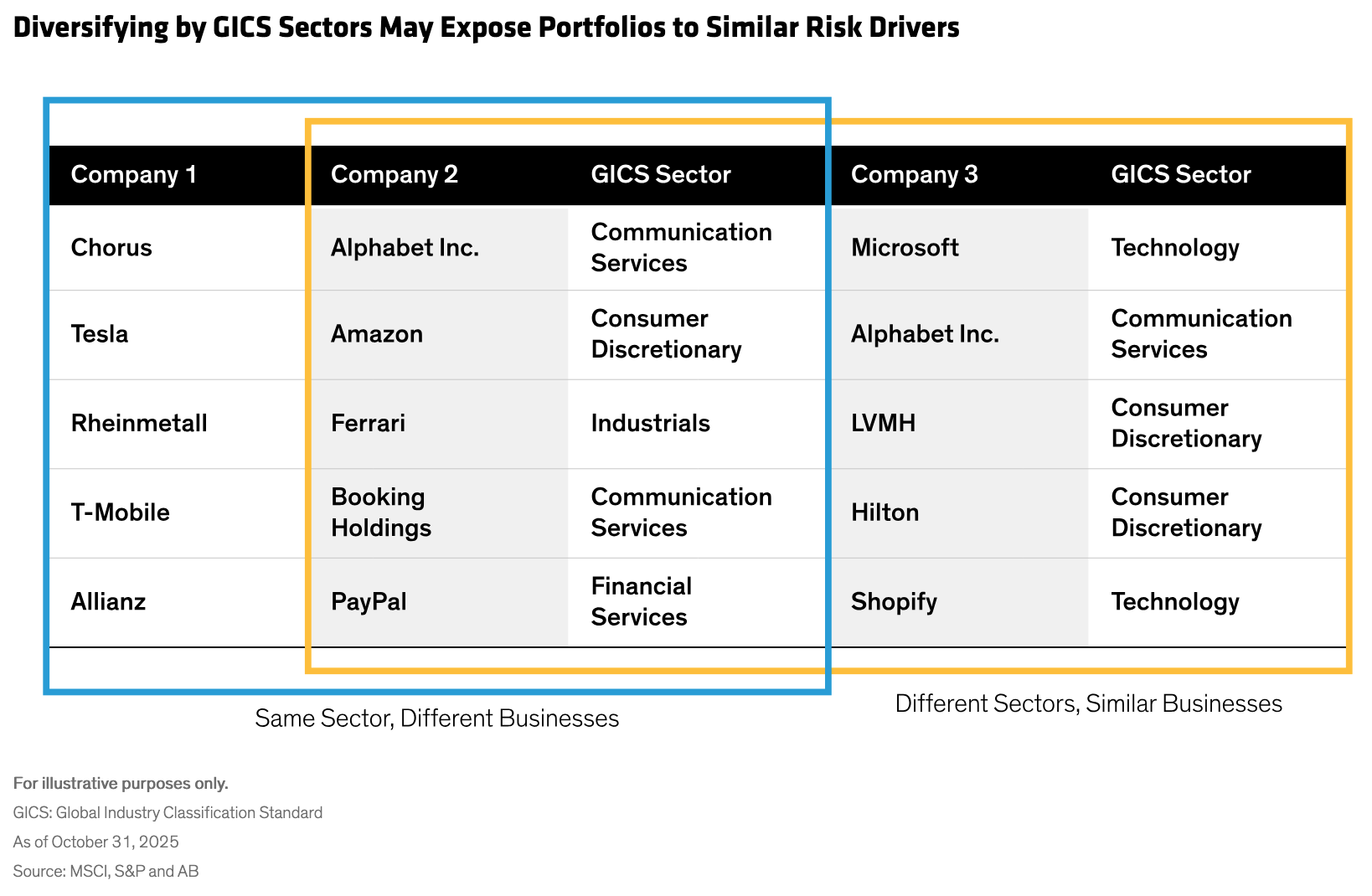

But sector classifications aren’t clear cut. For example, under GICS, Microsoft is an Information Technology company, whilst Alphabet Inc. (Google’s parent) and Chorus are in Communications Services (Display). However, both Microsoft and Alphabet have very similar businesses in global advertising, productivity applications and cloud infrastructure. Chorus, in contrast, owns and operates New Zealand’s fiber internet network. So Microsoft and Alphabet’s revenues and profits are quite correlated, yet GICS suggests a portfolio is diversified by owning Microsoft and Alphabet, but not if it owns Alphabet and Chorus.

Country classifications are similarly flawed because they typically determine a company’s geographic exposure based on its domicile. So, for instance, a position in Rio Tinto provides exposure to the UK—which only actually accounts for 1% of the company’s revenues.

Global Value Chains Add Risks

Standard classifications don’t capture the complexity of contemporary businesses. Disruptions can cascade across industries and borders. Firms with similar profiles might correlate with businesses in different industries and regions. Indeed, today we see cases of second, third or even fourth order contagion, as businesses many steps away in a value chain impact others. In 2021, an infamous fire at a Japanese plant of Renesas Electronics, which makes semiconductors for cars, disrupted Ford’s operations thousands of miles away.

Investors often trade deep company knowledge for the convenience of GICS-based diversification. This shortcut works—until it doesn’t. When President Trump announced his “Liberation Day” tariffs in early April, the broad equity market downturn reflected the interconnected reality of businesses and end-market exposures. Diversification through GICS classifications provided no protection.

How to Curb Risk in Capricious Markets

Given the drawbacks of standard risk and diversification tools, how can we improve efforts to maximize return and minimize risk? We believe a fundamental risk-management approach should look through two lenses:

- Use Actual Earnings (Not a Proxy): As long-term fundamental investors, we believe that (1) the value of an equity is the sum of its discounted future cash flows and (2) in the short term, markets are inefficient (and increasingly so). That’s why we think investors should focus on the volatility of actual company earnings, using both quantitative and qualitative analysis. Scrutinizing industry structure, company strategy and operational efficiency is the best way to determine the durability of a company’s actual earnings, in our view.

- Use Revenues and Costs (Not GICS): To understand portfolio companies, we undertake a Porter’s Five Forces analysis, a framework for identifying and analyzing industries. That involves mapping a company’s end-market exposures (customers or companies) by geography, sector and subsector (e.g., US advertising), which provides a view of actual aggregate portfolio-level exposures. Then, we dig deeper into the underlying end markets to identify potential correlations (e.g., brand versus direct response advertising). The five forces analysis also sharpens our focus on suppliers. While it’s nearly impossible to map all suppliers across a portfolio, searching at a high level for supplier concentration can empower investors to investigate the implications for the company and the broader portfolio.

Of course, this type of analysis is time-consuming. Since it can only be performed thoroughly on a relatively small number of companies, we think this approach works best in a concentrated portfolio of about 25 stocks. That might sound counterintuitive to conventional wisdom about diversification. Yet applying new risk-management perspectives to a concentrated portfolio can unlock the power of truly fundamental diversification—to deliver on the promise of MPT in today’s fast-moving markets.

About the Authors

George Ullstein is a Portfolio Manager for Global Equity Income and Growth. Prior to joining AB in 2021, he worked at Schroders as a portfolio manager responsible for growth and income strategies. Before that, Ullstein was a research analyst for Sarasin & Partners on the global equity income team. Earlier he was in various asset-management research and portfolio-management positions at Putnam Investments, Jupiter Asset Management and Bestinvest. Ullstein began his career in corporate public relations at Citigate Dewe Rogerson. He holds an LLB in law from the University of Southampton, England, and is a CFA charterholder. Location: London

Copyright © AllianceBernstein