by Carl Tannenbaum, Chief Economist, Northern Trust

Editor’s note: We are devoting our entire issue this week to the possibility of the Federal Reserve becoming politically compromised. This outcome would have substantial consequences for the global economy and global markets.

I was favored with an invitation to the Federal Reserve’s Jackson Hole conference in 2007. Entitled Housing, Housing Finance, and Monetary Policy, the sessions illustrated troubling feedback loops between the mortgage markets and the global economy. The clouds I recall gathering over the Grand Tetons were symbolic; a little over a year later, the world was in crisis.

I don’t know what the weather was like in Wyoming this year, but the symbolic clouds that were gathering as the world’s financial dignitaries assembled there were ominous. Presentation topics focused on labor markets and inflation, but the main issue hovering over the event was whether the Fed can remain independent of political influence. Should it lose that battle, the aftershocks could be substantial.

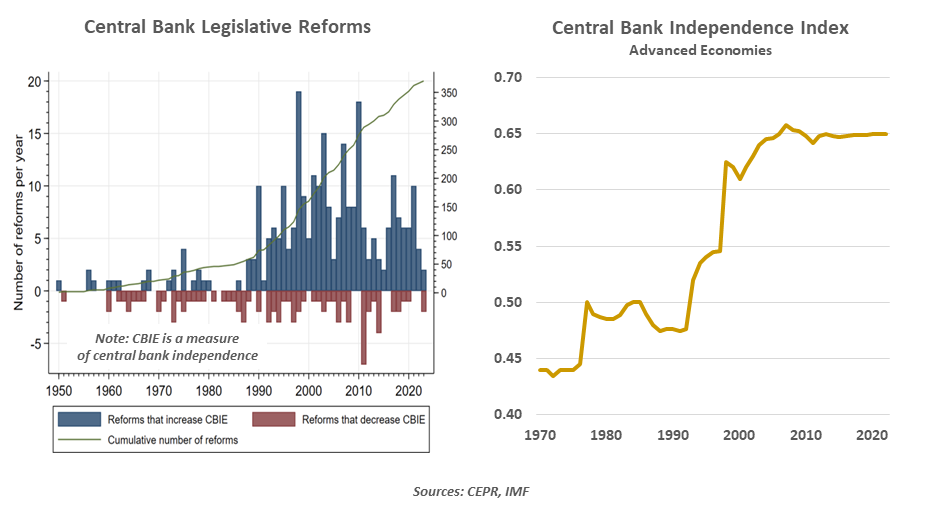

Independent central banks are a relatively recent concept. The Federal Reserve didn’t split cleanly from the Treasury Department until 1951; the Bank of England was a branch of the U.K. government until 1997. Debate over the proper degree of partition is still active in many places today.

Those favoring close alignment note the importance of accountability. Political leaders are democratically elected, and feel that their agendas reflect the public’s will. Central banks, in this view, should carry out the course agreed by leaders and their legislatures.

To others, however, central banks provide a check on economic policy that is comparable to the role that courts have in adjudicating the law. Governments that accrue large deficits might wish to run the printing presses to finance themselves, leading to inflationary conditions. Creating space for central banks to focus on long-term goals like stable inflation raises the chances of achieving good outcomes. Terms for monetary authorities are long (14 years, in the case of Fed Governors), to immunize them from shifts in political cycles.

The Case For Independence

There is a substantial body of literature that links distance between governments and their central banks with lower rates of inflation. This, in turn, is positive for economic growth, employment and asset prices. The Fed’s success in fulfilling its mission over the past forty years inspired an increase in the level of central bank independence around the world.

Countries that have opted not to follow this approach have been punished by the financial markets. A recent example is Turkey, whose central bank has been directed by a string of individuals close to its president. That country has experienced double digit inflation, a weak currency and capital flight.

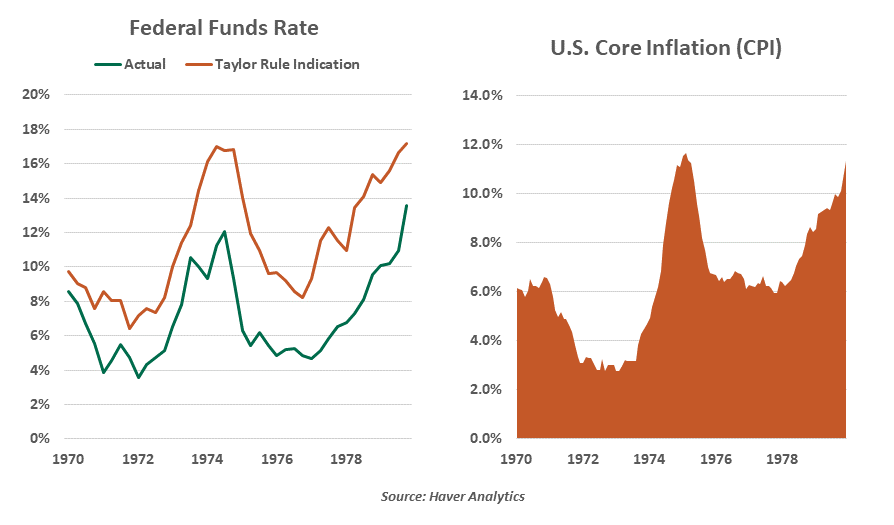

The experience of the 1970s is a cautionary tale for opponents of central bank independence.

This evidence hasn’t stopped American leaders from trying to influence monetary policy. As we described last spring, political criticism of the Fed is the rule, not the exception. Most of the time, this has been limited to public statements.

The most significant incursion of politics into U.S. monetary policy came during the 1970s, when Richard Nixon appointed his advisor Arthur Burns to head the Fed. Burns kept interest rates lower than they should have been, resulting in substantial inflation at the end of the decade. (The “Taylor Rule” estimation in the chart below provides an estimate of what interest rates should have been, given trends in growth and inflation.) That experience informed a “hands off” posture from the White House that lasted until 2017.

The Fed is an unelected group, but it is not unaccountable. Governors are subject to political approval; they are nominated by the White House and confirmed by the Senate. The Chair provides a monetary report to Congress twice each year, and fields pointed questions from both sides of the aisle. The Fed’s operations are independently audited each year, and they are subject to review by the Government Accountability Office, which is accountable to Congress. The communication surrounding the Fed’s decision-making has expanded substantially over the past forty years; some would say that there is actually too much of it.

Under both Trump administrations, calls for lower rates and disparagement of Fed officials have been common. Nonetheless, monetary strategy has continued to be guided by fundamentals. Post-pandemic inflation, which remains above the 2% target, has kept policy on the restrictive side. This has increased the ire of the White House, which has called for overnight rates to be 300 basis points lower than they are today.

The President has frequently mused about firing current Fed Chairman Jay Powell, whose term at the head of the table concludes next May. This has been seen by most market participants as posturing. But last month, the President took action to terminate Fed Governor Lisa Cook. Cook has sued to retain her position; the matter is now in the hands of the courts. At issue is what “cause” is sufficient to remove a senior official; the termination has no precedent.

The move is part of an effort by the White House to gain control of monetary policy. “We’ll have a majority very shortly,” said the President last week, referring to the makeup of the Fed’s Board of Governors. If Governor Cook loses her appeal to stay, four of the seven members will soon be Trump appointees.

There is no assurance that this cohort will vote as a block. Governors Bowman and Waller have made strong statements this year in favor of Fed independence; Waller spent many years as the research director at the Federal Reserve Bank of St. Louis. But if the courts uphold Governor Cook’s dismissal, the Administration could seek grounds to terminate others.

A partisan Fed could take a number of unorthodox steps.

What Would A More Political Fed Do?

A politically motivated majority of Governors could take a number of actions over time that would have been unimaginable before this year. Among them:

- The Presidents of the regional Federal Reserve Banks are chosen by independent directors, and they are approved by the Board of Governors. Presidents have their positions confirmed by the Fed’s Board at five-year intervals. The next review takes place in the first quarter of next year.

This is normally a routine affirmation. But a more activist Board could withhold support for leaders who will not carry out its wishes. This could scramble the membership of the Federal Open Market Committee, the group that decides on monetary policy, providing a window for aggressive rate cuts. The bar for raising interest rates under any circumstances would rise, potentially exaggerating inflationary cycles.

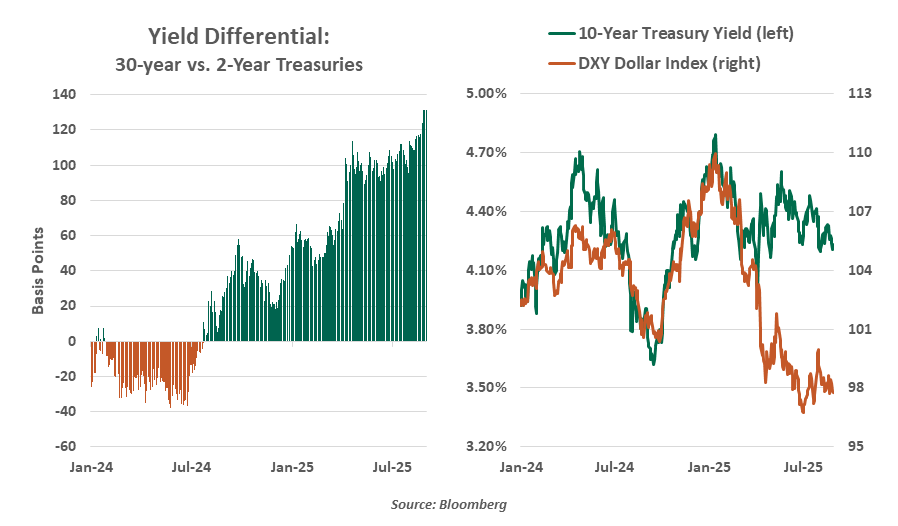

- The Federal Reserve’s balance sheet could be utilized in a series of interesting ways. Risks to the Fed’s independence have already caused the U.S. yield curve to steepen, which runs counter to the Administration’s wish for lower mortgage rates. The Fed could be directed to purchase significant sums of Treasury or mortgage-backed securities, replicating the yield curve control programs that have been used in Japan and other places. This would serve the dual purpose of creating additional demand for Treasury debt, which could help to fund burgeoning budget deficits.

In more extreme expressions, the Fed’s balance sheet could be used to house assets that are supportive of the Administration’s industrial policy. Digital currencies could be among them.

A larger central bank balance sheet would put more currency into circulation, which would likely devalue the dollar. This is also consistent with the Administration’s efforts to rebalance the terms of trade; Stephen Miran, who has been nominated to the Fed Board of Governors, has advocated for a weaker currency as part of his “Mar-A-Lago Accord.”

The dollar has been depreciating this year, and the normal link between Treasury yields and the currency has been broken. When a country’s bond prices and its currency are falling simultaneously, that is a clear sign of investor concern.

- The framework used by the Fed to implement monetary policy could be altered in a way that favors easier conditions. A review of the framework is performed every five years; Chair Powell described the results of this review in his speech at Jackson Hole. But there is nothing to prevent the Board of Governors from reopening the process.

- An effort to change the inflation target could be undertaken. The level and/or the definition of the measure used could be reviewed.

- During periods of crisis, the Federal Reserve has opened swap lines with other central banks. This allowed them access to liquidity in dollars, which was needed by their domestic institutions. Given the changing relations between Washington and other world capitals, it is not clear that a more political Fed would take this step. Without the swap lines, banking stress could escalate quickly.

- Fed supervision could potentially be used in selective ways to further a political agenda on a number of fronts. The Administration issued an executive order last month, directing regulators to investigate banks for “politicized or unlawful debanking.”

These still seem like extreme outcomes, but no possibility should be ruled out. The Project 2025 transition plan, which has influenced the Administration’s approach to a variety of policies, devoted a full chapter to musings on the Federal Reserve. The plan calls for ending the Fed’s maximum employment mandate, preemptively halting any future crisis lending, and exploring a move back to a gold- or other commodity-backed currency system. A lot would have to happen for any of these ideas to become reality. But the potential for personnel changes at the Federal Reserve over time has increased the odds of a tail event.

Bond yields and the U.S. dollar are already reflecting concern over the Fed.

The reaction of financial markets could provide a check on the Administration’s ambition to control the Fed. A selloff in stocks and bonds could prompt a policy re-evaluation, as it did after the “Liberation Day” tariff announcement in April. Legal challenges are likely along the way; in a decision related to other administrative terminations this year, the Supreme Court gave specific deference to the Federal Reserve. Congress retains the right to reject appointments or proposals that might be viewed as too extreme.

The U.S. economy is performing pretty well at the moment. Equity markets have enjoyed another favorable year. Unemployment is very low. Banks are very healthy. One might look at this evidence and wonder why the situation surrounding the Fed is such a big deal.

Borrowing a line from Casablanca, a compromised Fed may not be a problem today, or tomorrow; but it could be soon, and for the rest of our lives. If the Fed’s reputation is diminished, inflation could become unmoored. This would discourage investment, raise costs and damage asset values. The probability of this outcome is low, but rising; and the consequences are vast.

A little over a year after my attendance at Jackson Hole, I found myself working at the Federal Reserve Bank of New York, trying to ascertain the extent of the global financial crisis. The courage to do the right thing in the face of immense outside pressure was a hallmark of the Fed’s leadership at that time, and of the institution. I am convinced that we were on the verge of a second Great Depression, which was averted because central banks had the latitude to act without waiting for political endorsement.

I certainly hope that central banks can maintain the respect and space they need to do their jobs. Our economic futures will depend on it.

Copyright © Northern Trust