by Vaibhav Tandon, Senior Economist, Northern Trust

Common disparagements of television dramas include overdramatic plot twists and inconsistencies, often perceived as unrealistic and irrational. Characters abruptly change their sentiments or motivations, leading to a sense of incredulity and frustration. Some viewers enjoy the drama and suspense, but others find the constant flip-flops to be exasperating.

U.S. trade policy movements are starting to resemble a soap opera. Following a series of threats, escalations and suspensions, President Trump has extended the tariff deadline to August 1. This keeps the pressure on trading partners to offer swift concessions. Some goods imported from Canada, America’s second-largest trading partner, will be charged a 35% tariff. U.S. allies Japan and South Korea were put on notice for a 25% duty, unless they boost imports and manufacturing activity in the U.S. Other countries are staring at levies of up to 40%.

The President has also threatened some additional sectors: 50% on copper imports, 200% on pharmaceuticals and an additional 10% on countries that align with BRICS nations. Trade or economic considerations are not the sole driver of the U.S. administration’s tariff decisions. Brazil will be hit with a 50% duty over the treatment of its former president Bolsonaro.

Trade negotiations have been arduous, with only two pacts agreed over the last three months. A deal with the U.K., with which America has a trade surplus, was thin. It left a 10% tariff in place on British exports. Vietnamese exports to the U.S., reportedly, will be tariffed at a 20% rate. Transshipments will be taxed 40%, a move aimed at preventing Chinese goods from being rerouted to evade U.S. tariffs.

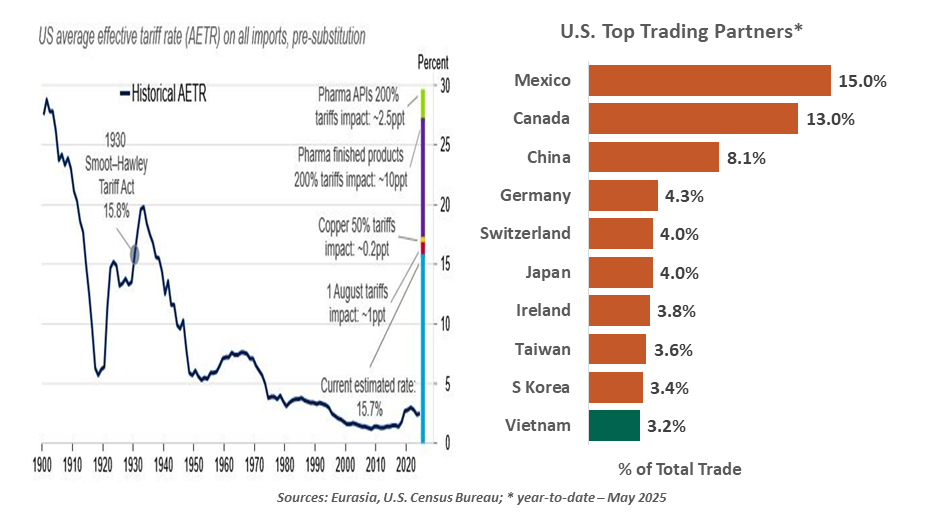

The trade war drama is raising real costs.

The 14 nations facing threats of higher tariffs accounted for $460 billion or around 10% of total U.S. imports in 2024. Raising levies to 25%-40% would push the U.S. average effective tariff rate up by a full percentage point to about 17%, the highest in nearly a century.

Tariffs are starting to bite. Amid persistent uncertainty, pessimism has crept into both business and consumer surveys. German and Japanese automobile shipments to the U.S. dropped 25% each in May. China’s producer price index declined further to its weakest reading in almost two years in June. Deflationary pressures in China are only going to worsen further, with the U.S administration turning its focus to curbing the rerouting of Chinese goods.

Higher tariffs on countries like Vietnam and Brazil will also raise prices of a range of consumer goods in the United States. Vietnam is a major supplier of electronics like smartphones. Around one-third of the coffee consumed in America comes from Brazil.

Save Vietnam, the U.S. has not struck a permanent agreement with any of its top ten trading or import partners. The clock is ticking on the fragile U.S.-China trade truce, set to expire on August 12. The prospects of a long-term deal between the world’s two largest economies are slim as barriers remain high. Japan is reluctant to open up its politically-sensitive rice market and is seeking concessions for its economically vital auto industry. The U.S. is reportedly closing in on a skeletal deal with other major trading partners like the European Union and India.

Stop-gap deals won’t mark the end of the trade war. New pacts may be limited in scope, leaving many specifics to be negotiated later. The limited “Phase One” trade deal between the U.S. and China during Trump’s first term took two years of negotiations in a less combative environment. Those still hoping that tariff uncertainty will vanish anytime soon are in for further disappointment.

We’ll remain tuned in to the long, drawn-out trade war drama. Plot twists will be inevitable. But unlike in television shows, the real-life consequences of these twists will not be entertaining.

Copyright © Northern Trust