by Russ Koesterich, CFA, JD, Portfolio Manager, BlackRock

In this article, Russ Koesterich discusses the recent performance of gold and its ongoing role as a store of value in investors’ portfolios.

Key Takeaways

- While gold has proven to be a somewhat unreliable short-term hedge, Russ reiterates that it continues to be an effective store of value over the long-term, particularly in today’s rocky environment of geopolitical uncertainty.

- Importantly, as U.S. debt-to-GDP ratio grows, gold has historically reacted in a non-linear fashion, with gold prices increasing as the U.S. debt pile grows.

While stocks have staged a remarkable and rapid recovery from the April lows, on a year-to-date basis U.S. equities are flat. On a global basis, returns are a bit better. Exceptionally strong European markets have led global indices to a 5% year-to-date gain. However, both domestic and international equity returns are paltry next to the performance of gold.

Although off the recent highs, year-to-date gold is still up roughly 25%. While I would not extrapolate those returns into the back-half of the year, I would continue to hold a small position in gold as a portfolio diversifier.

I last discussed gold back in January. At the time I suggested that while gold is an unreliable short-term hedge, it is an effective store of value. This characteristic is particularly important today, as investors wrestle with both record government debt and wrenching changes in international trade. The fact that the dollar is also under significant pressure, only adds to the argument.

Higher uncertainty leads to higher volatility

Back in January, investors were unprepared for the magnitude and breadth of the announced tariffs. While many have subsequently been delayed and the economic impact, thus far, has been muted, policy uncertainty remains unusually high.

Historically, when investors are confused and uncertain as to government policy, equity volatility tends to be elevated. During periods of heightened volatility, gold generally outperforms stocks, as it has year-to-date.

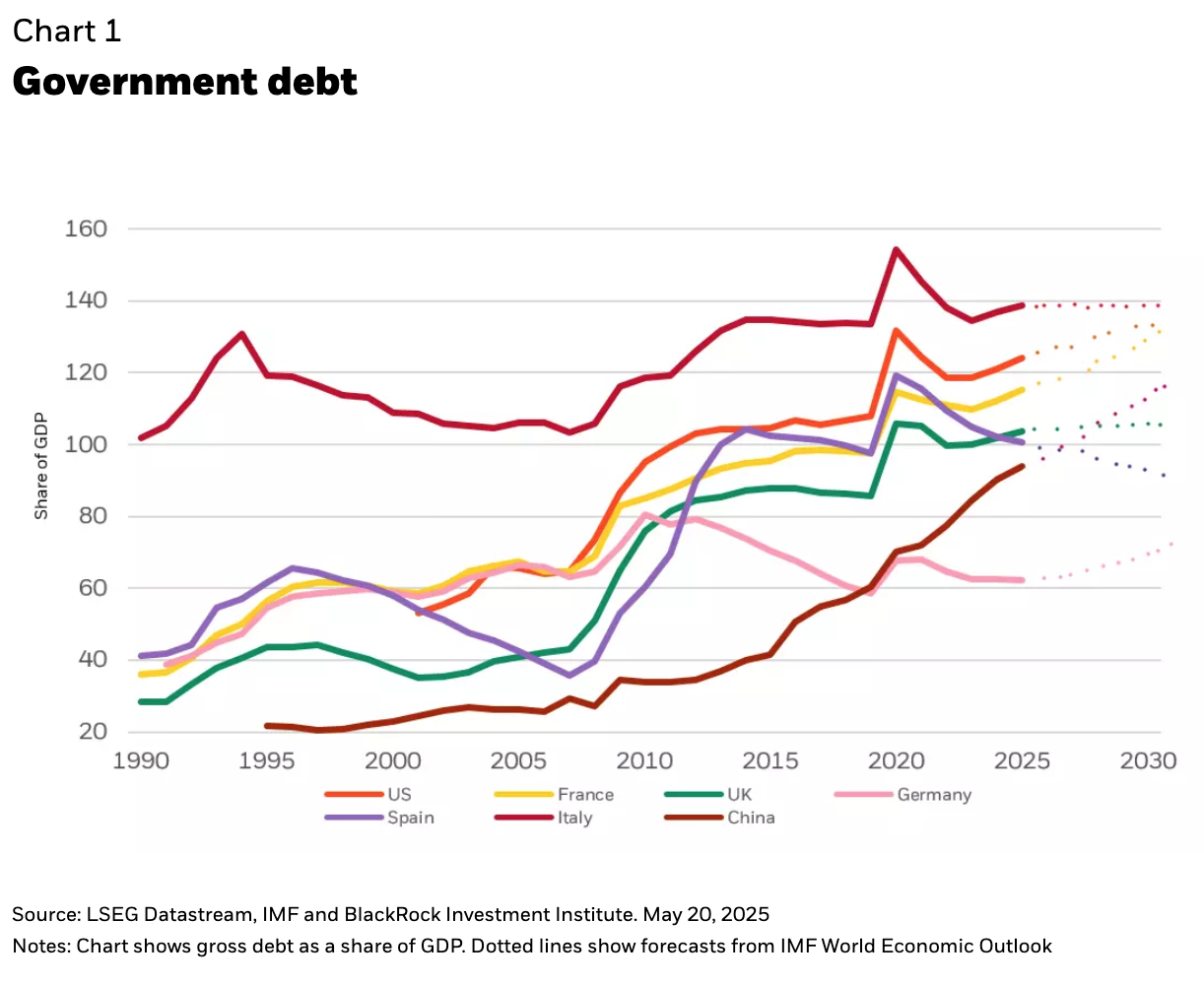

Longer-term there is a more pressing problem: huge and growing piles of government debt. While investors have focused on the U.S. fiscal situation, other countries, notably Italy and Japan, have also pushed public debt well above gross domestic product (GDP) (see Chart 1).

The growing public debt of the U.S. government is of particular concern. Given the size of U.S. debt markets and the dollar’s reserve currency status, gold prices have historically had a strong relationship with the level of U.S. public debt. As U.S. debt-to-GDP grows, gold typically follows. More importantly, in the past the relationship between gold and government debt has been non-linear. In other words, gold price gains have tended to accelerate as public debt has approached and now surpassed 100% of GDP.

Gold as a long-term holding

As I discussed back in January, investors should not expect gold to act as a hedge on a day-to-day basis. If anything, on a given day or week gold has recently been trading in the same direction as stocks. That said, the value of gold is not as a short-term hedge but as a long-term insurance policy. While the yellow metal has already had a stellar run, looking further out, heightened policy uncertainty and record debt levels suggest keeping some tucked away in your portfolio.

Copyright © BlackRock