by Russ Koesterich, CFA, JD, Portfolio Manager, BlackRock

In this article, Russ Koesterich discusses the risk of higher interest rates and the potential impact (both positive and negative) such a move could have on markets.

Key takeaways

- History has shown that an abrupt move upward in interest rates can lead to a stock market correction, often resulting in a significant impact on returns. With U.S. government budget negotiations ongoing, an extended deficit could push investors to buy longer-dated bonds, likely pushing rates higher.

- Keeping these risks in mind, investors could benefit from incorporating additional hedges into their portfolios – namely gold and short-dated Treasuries – to protect themselves from such a move

Markets generally go down for one of three reasons: a recession, higher interest rates or an exogenous shock, such as the COVID-19 pandemic or the 9/11 attacks. While I continue to believe stocks will end the year higher, if we do see a correction, higher rates are probably the larger risk.

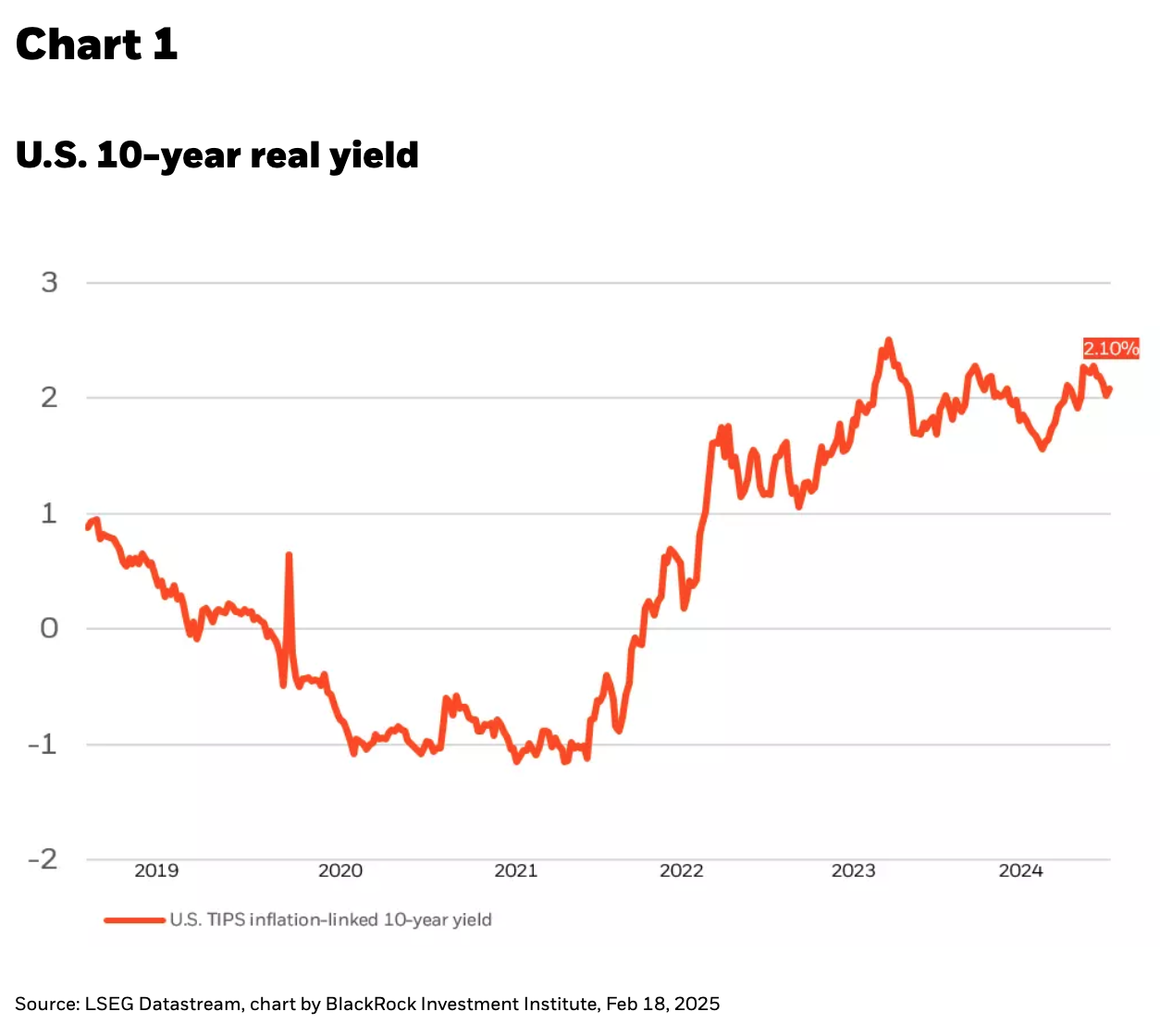

When considering the impact of interest rates on stocks, it helps to be specific. As I’ve discussed in previous blogs, stocks are most sensitive to a quick upward move in real, or inflation-adjusted, interest rates. The ‘quick’ part is an important qualifier; abrupt moves, rather than gradual adjustments, are more likely to lead to a correction.

This is exactly what happened in late December and early January. Real 10-year yields surged by roughly 0.50% (see Chart 1). Right on cue, stocks posted a modest correction. The S&P 500 fell 5%, while small caps, generally more rate sensitive, fell more than -10%.

That market move was very consistent with history, both short- and long-term. Based on the past three years of data, monthly changes in real 10-year yields have had a very significant impact on market returns, explaining approximately 65% of the variation in S&P 500 monthly changes.

Not only was the December/January move directionally consistent with similar episodes of higher rates, but the magnitude of the pullback was also about what you would expect. Since the late 1990’s, when real 10-year yields have risen sharply, defined here as a move of 0.50% or more in a month, the S&P 500 posts an average loss of around -3%, very consistent with the move earlier this year.

Budget Risks May be Front and Center

My base case remains that stocks end the year higher, and interest rates remain range bound. That said, there are risks. One in particular: ongoing budget negotiations within the U.S. government. The U.S. is already contending with debt levels and deficits not seen outside of a war or recession. To the extent deficits continue to climb, investors may decide that they require a larger term premium, i.e. the extra rate needed to coax investors to buy long-dated bonds. This would likely lead to higher real rates.

For investors concerned about higher deficits and interest rates, how to best position? One traditional strategy I would avoid: defensive stocks, such as staples and regulated utilities. Individual investors often own these securities for their high dividends, which become less appealing when investors can secure a similar yield with a risk-free asset, like U.S. Treasuries.

Instead, I would focus on two asset classes: gold and short-dated Treasuries. Gold is proving an effective hedge against structurally higher deficits. At the same time, short-duration Treasury notes are offering an attractive yield, without the rate risk that comes with longer-dated paper. Both assets should help mitigate portfolio risk if higher deficits lead to higher rates, and a softer stock market.

Copyright © BlackRock