by Russ Koesterich, CFA, JD, Portfolio Manager, BlackRock

In this article, Russ Koesterich discusses why cyclical leadership in equities could continue into 2025.

Key takeaways

- 2024 has been a year of equity market growth, with market leadership in a state of flux. Since September, cyclical stocks have led markets, a trend that was reaccelerated post-election on hopes of tax cuts, deregulation and onshoring.

- Looking ahead, we believe the cyclical rally could continue given improving economic expectations as well as reasonable valuations.

- While in favor of cyclical exposure in 2025, an emphasis on quality may serve investors well should volatility pick-up.

While stocks continue to push higher, leadership remains in a state of flux. The first half of the year was largely a repeat of 2023: tech led the market. By mid-summer the narrative shifted; small caps, an asset class left for dead, staged a remarkable but ultimately short-lived rally. The narrative shifted again in early August, as a somewhat weak U.S. payroll report reignited recession concerns and pushed investors into low-beta, defensive stocks.

By September, as economic data evidenced more strength, leadership shifted again, this time into more economically sensitive, cyclical stocks. The trend has accelerated post-election, with hopes for tax cuts, deregulation and a U.S. manufacturing renaissance. Given the potential for solid growth and re-shoring of manufacturing activity, cyclical leadership could continue into 2025.

Recession to boom

The recent rotation into cyclicals has occurred against a background of improving economic expectations. Investors have followed economists in belatedly recognizing the extraordinary resilience of the U.S. economy. According to Bloomberg a consensus of economic forecasts now expects real 2024 gross domestic product (GDP) of 2.7%. In January the consensus was 1.2% and as recently as August it was still slightly above 2%.

Consistent with recent history, rising estimates have been driven by a resilient U.S. consumer. According to Bloomberg, the 2024 consensus estimate for real consumer spending was 2.6% in November, roughly double where it was at the start of the year.

While most economists expect a modest deceleration growth in 2025, here too estimates are improving. Consensus forecasts are for trend growth (average sustainable rate of economic growth) of around 2.1%, up dramatically from the August lows of 1.7%. Optimism is supported by continued strength in the labor market and signs of life from the manufacturing sector. In November the ISM Manufacturing New Orders component accelerated to 50.4, its highest level since early spring.

On the cheap(er) side

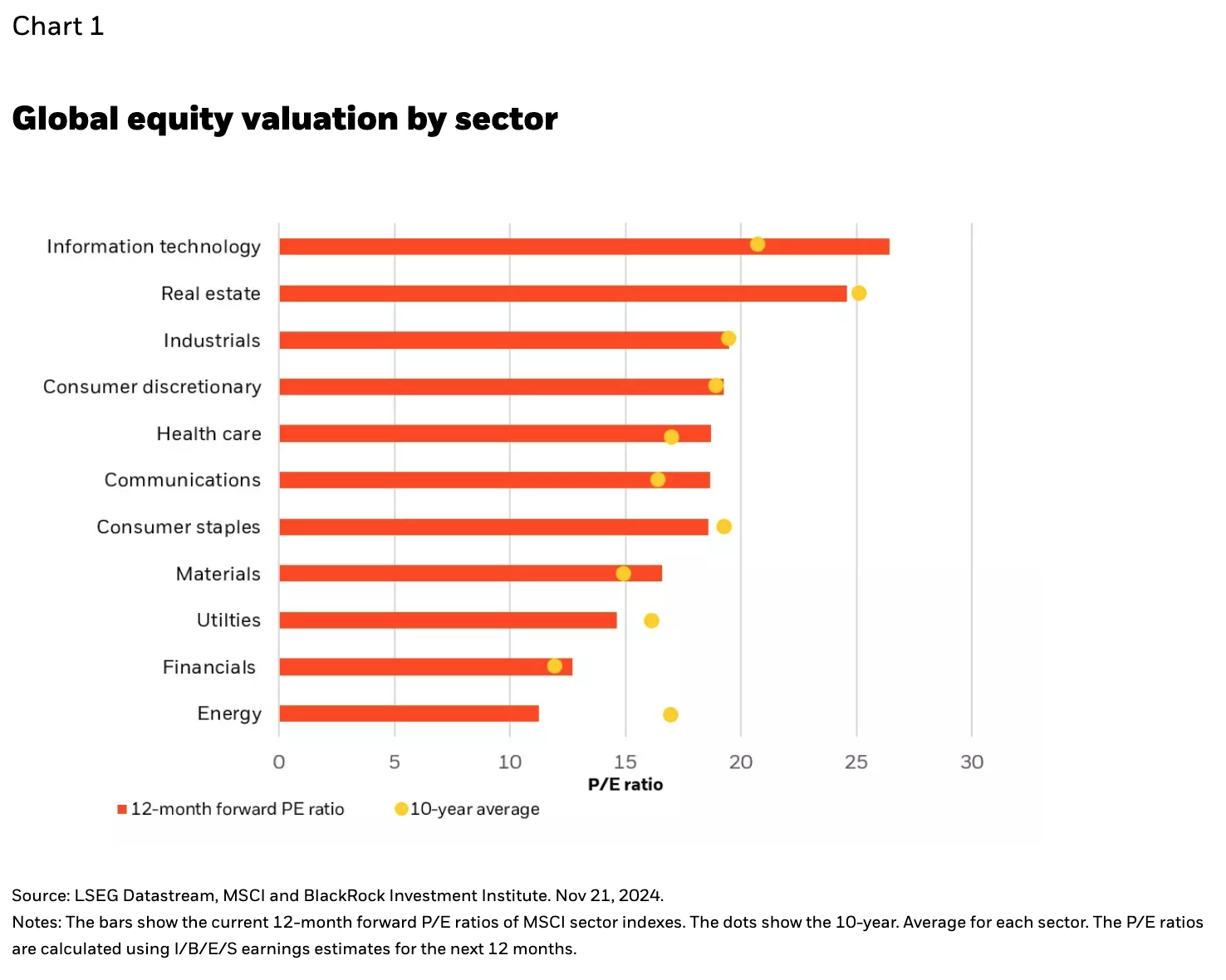

Apart from a solid growth outlook, the other argument for cyclical stocks is their relative cheapness. To be clear, with the S&P 500 Index trading at 22x next year’s earnings, apart from energy there are few absolute bargains. That said, compared to the technology sector and related names, cyclical stocks look more reasonable. Financials and Industrials are trading close to their 10-year average (see Chart 1). And while the consumer discretionary sector is trading at a premium relative to its own history, much of that is driven by internet retailing and electric vehicle (EV) companies. Outside of these two industries, which have a disproportionate weight in the sector index, valuations are more reasonable.

Cyclical but stay up in quality

Going into 2025 I would remain overweight cyclicals, particularly financials, aerospace and select consumer discretionary names. There is also room for some of the more cyclical parts of technology, including select semiconductor names. One caveat: stay up in quality. In other words, emphasize companies with high margins, proven ability to generate consistent earnings and low debt rather than the more speculative names in the space. While the economy should keep chugging along, today’s low volatility environment won’t last forever. Higher quality names will help mitigate risk when the euphoria fades and volatility picks up.