by Howard Marks, Vice Chairman, Oaktree Capital

When I travel to see clients and spend entire days discussing investing and the markets, memo ideas often pop up. Last month’s visit with clients in Australia is a case in point. We talked about the “sea change” I believe is taking place in interest rates and about the role of credit in portfolios, and in a few cases, this led to the general topic of asset allocation. The result wasn’t a lot of new ideas on the subject, but rather a new way to combine old ideas into a unified theory.

Before I proceed, I want to mention that, from time to time in this memo, I’ll say “generally,” “usually,” or “everything else being equal.” These caveats are likely applicable to many more sentences and ideas herein, but for the sake of readability, I’m not going to repeat them ad nauseum. In addition, I’m going to use a lot of graphics, as I truly believe one picture is worth a thousand words. Please bear in mind that these representations are intended to be notional, not technically correct.

Asset Classes

From my vantage point, “asset allocation” is a relatively new thing. No one used that phrase when I joined the industry 55 years ago. Structuring portfolios was a pretty simple matter, generally following the classic “60/40” split. Most U.S. investors limited themselves to investing in U.S. stocks and bonds, and there was a time-honored notion that something like 60% equities and 40% bonds represented reasonable diversification.

Today, investors are presented with so many choices – and there’s so much emphasis on getting the decision right – that the term “asset allocation” is very prominent, and there are individuals and whole departments dedicated to doing just that. It’s their job to decide how to weight the asset classes to be held in a portfolio, meaning asset allocators spend their time on decisions like these:

- How much in equities and how much in debt?

- How much in stocks and bonds and how much in “alternatives”?

- How much in public securities and how much in private assets?

- How much in one’s home country and how much abroad?

- How much of the latter in the developed world and how much in emerging markets?

- How much in high quality assets and how much in low quality?

- How much in more volatile “high beta” assets and how much in steadier ones?

- How much in levered strategies and how much unlevered?

- How much in “real assets”?

- How much in derivatives?

It’s enough to make your head spin. Many investors use computer models to help with these decisions, but the models require inputs regarding expected return, risk, and correlation, and most of these are based on history and thus of questionable relevance to the future. Correlation between asset classes is particularly difficult to predict. It’s often a case of garbage in, garbage out (but with the added comfort that comes from using mathematical models).

Ever since coming up with my sea change thesis regarding interest rates two years ago, I’ve been talking about the increased utility of credit investments. And the more I’ve done so, the more I’ve thought about the difference between credit investments and equities. Thus, the first thing I want to mention about my “Australian epiphany” is the unconventional idea that, at bottom, there are only two asset classes: ownership and debt. If someone wants to participate financially in a business, the essential choice is between (a) owning part of it and (b) making a loan to it.

When I moved from Citibank’s equity research department to its bond department in 1978, I learned firsthand that this is a matter of night and day. On my new desk, I found a machine called a Monroe 360/65 Bond Trader. If you typed in a bond’s interest rate, maturity date, and market price, it would tell you the yield to maturity . . . in other words, what your return would be if you bought the bond at that price and held it to maturity (and it paid). This was revolutionary to me. On the equity side I’d come from, there was no place you could look to find out what your return would be.

This highlighted for me something I’ve always felt most investors don’t grasp viscerally: the essential difference between stocks and bonds . . . that is, between ownership and lending. Investors seem to think of stocks and bonds as two things that fall under the same heading. But the difference is enormous. In fact, ownership and lending have nothing in common:

- Owners put their money at risk with no promise of a return. They acquire a piece of a business or other asset and are entitled to their proportional share of any residual that remains after the necessary payments have been made to employees, providers of raw materials, landlords, tax authorities, and, of course, lenders. If there’s something left over, it’s called profit or cash flow, and the owners have the right to share in whatever part of it is paid out. And if there’s profit or cash flow (or the potential for it in the future), the business will have “enterprise value,” in which the owners also share.

- Lenders typically provide funds to help owners purchase or operate businesses or other assets and, in exchange, are promised periodic interest and the repayment of principal at the end. The relationship between borrower and lender is contractual, and the resulting return is known in advance as described above, again assuming the borrower makes the promised payments when due. That’s why this kind of investing is called “fixed income” – the income is fixed. For the purposes of this memo, however, it might help to think of it as “fixed outcome” investing.

This isn’t a difference in degree; it’s a difference in kind. Ownership assets (things like common stocks, whole companies, real estate, private equity, and real assets) and debt (bonds, loans, mortgage backed securities, and other streams of promised payments) should be thought of as entirely different, not variations on a theme. They have different characteristics and potential, and the choice between them is one of the most basic things investors must decide.

The Essential Choice

At the outset of this memo, I listed some of the decisions that comprise the asset allocation process. But how can those decisions be approached? What’s the framework for making them?

The next piece that clicked into place in my thinking “down under” was with regard to the basic characteristics of a portfolio. In my opinion, one decision matters more than – and should set the basis for – all the other decisions in the portfolio management process. It’s the selection of a targeted “risk posture,” or the desired balance between aggressiveness and defensiveness. The essential decision in investing is how much emphasis one should put on preserving capital and how much on growing it. These two things are mostly mutually exclusive:

- Insistence on preserving capital – or, secondarily, on limiting the portfolio’s volatility – calls for an emphasis on defense, which precludes pursuing maximum growth.

- Correspondingly, a decision to strive to maximize growth requires an emphasis on offense, meaning preservation of capital and steadiness must be sacrificed to some degree.

It’s one or the other. You can’t simultaneously emphasize both preservation of capital and maximization of growth, or defense and offense. This is the fundamental, inescapable truth in investing. The questions listed on page one are just details, the options available for reaching your targeted risk posture.

If you think about portfolio construction in this sense – looking for the right balance between offense and defense – it becomes clear that the goal should be optimization, not maximization. To my mind, it shouldn’t be “wealth,” but “wealth pursued in an appropriate way, taking into account the investor’s wants and needs.”

Many people think the proper goal in investing is achieving the highest return. More sophisticated thinkers understand – either intellectually or intuitively – that the goal should be to achieve the best relationship between return and risk. If you follow that latter mandate, it’ll hopefully lead you to assets whose expected return is more than sufficient to compensate for their risk, and thus to a portfolio with the potential for an attractive risk-adjusted return. But that’s not enough.

The absolute level of risk in a portfolio shouldn’t be an unwitting consequence of the asset allocation process described above, or of the search for superior risk-adjusted returns. The absolute risk level must be consciously targeted. In fact, in my view, it’s the most important thing. For an investment program to be successful, the level of risk in the portfolio must be well compensated and fall within the desired range . . . neither too much nor too little.

The Shape of the Curves

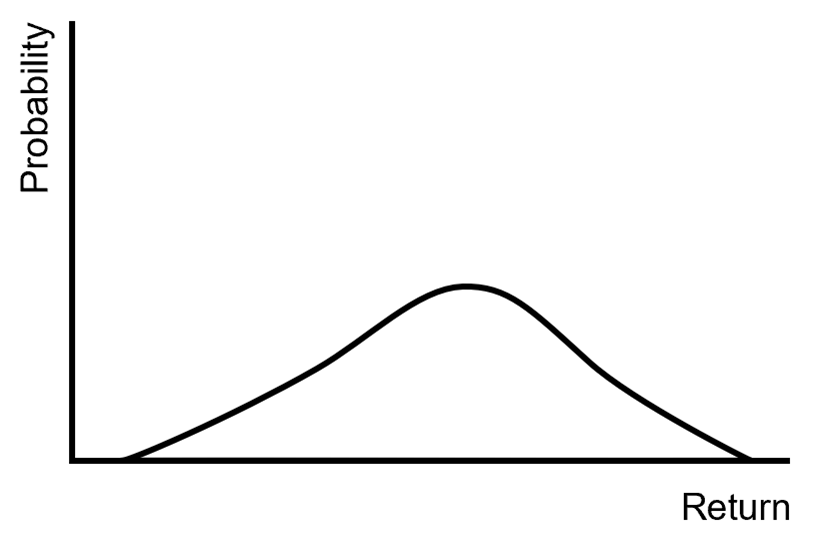

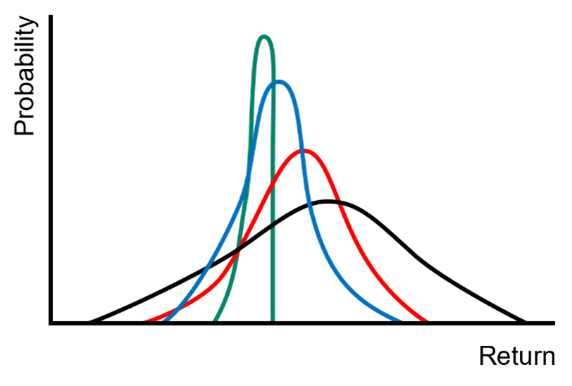

In the last few months, I’ve been drawing probability distributions to illustrate the fundamental difference between the potential returns from ownership assets and debt (or “fixed income,” “credit,” or whatever you want to call it). Here’s the general shape of the curve describing the potential return on a portfolio of ownership assets (Figure 1):

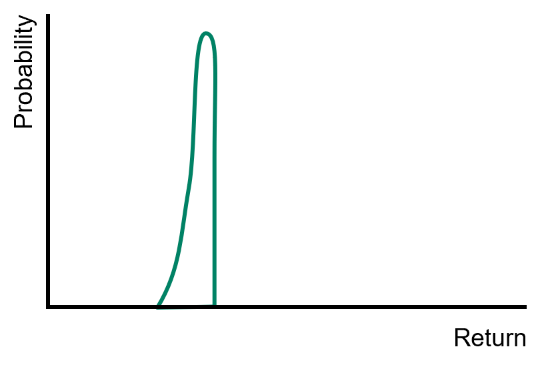

And following on page four is the shape of the curve describing the potential return on a portfolio of debt (Figure 2):

Ownership assets typically have a higher expected return, greater upside potential, and greater downside risk. Everything else being equal, the expected returns from debt are lower but likely to fall within a much tighter range. There’s generally no upside on debt – no one should buy an 8% bond expecting to make more than 8% per year over the long term. But there’s also relatively little downside – you’ll get your 8% if the borrower pays, and relatively few fail to pay. For this reason, offense is usually better played through ownership assets, and defense is usually better played through debt. (I hasten to add that investing isn’t a matter of either/or. The two can be combined, meaning the operative question surrounds the right mix.)

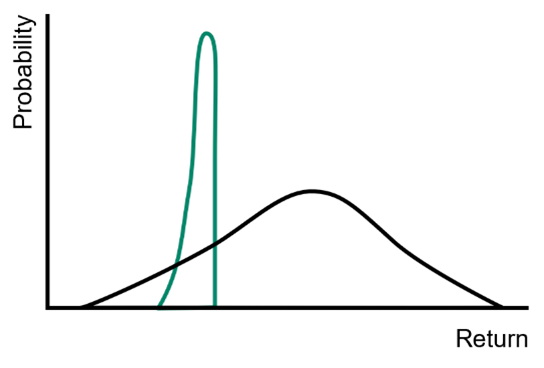

In the low-interest-rate environment that prevailed from 2009 through 2021, the expected return from debt was extremely low in the absolute and far below the historical return on equities, rendering debt relatively unattractive (Figure 3).

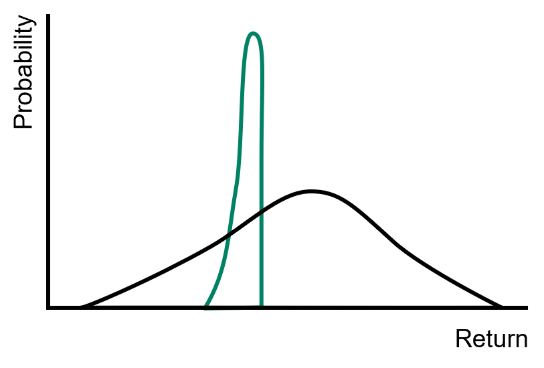

But today, it’s considerably higher than it was and closer to that of equities (Figure 4). That’s why I’ve been urging increased investment in credit.

Obviously, the relationship between the two curves at a point in time has a very direct bearing on the appropriate asset allocation at that time.

Which of the two is “better,” ownership or debt? We can’t say. In a market with any degree of efficiency – that is, rationality – it’s just a tradeoff. A higher expected return with further upside potential, at the cost of greater uncertainty, volatility, and downside risk? Or a more dependable but lower expected return, entailing less upside and less downside? The choice between the two is subjective, largely a function of the investor’s circumstances and attitude toward bearing risk. That means the answer will be different for different investors.

Choosing the Offense/Defense Balance

I’ve previously expressed my view that, as a starting point, every investor or their investment manager should identify their appropriate normal risk posture or offense/defense balance. For each individual or institution, this decision should be informed by the investor’s investment horizon, financial condition, income, needs, aspirations, responsibilities, and, crucially, intestinal fortitude, or their ability to stomach ups and downs.

Once investors have specified the normal risk posture that’s right for them, they face a choice: they can maintain that posture all the time, or they can opt to depart from it on occasion in response to the movements of the market and thus changes in the attractiveness of the offerings it provides, increasing their emphasis on offense when the market is beaten down and on defense when it’s riding high.

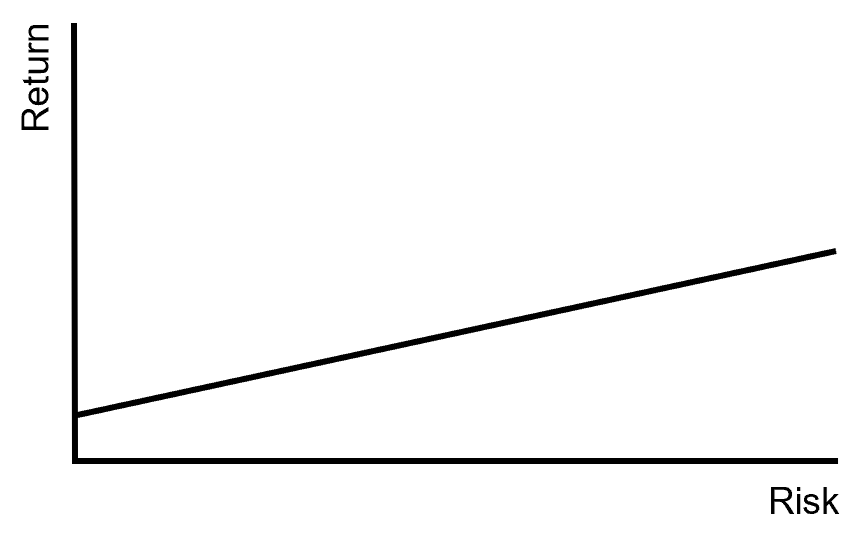

Regardless of whether one’s risk posture is fixed or variable, however, the next question is how one gets there. This question led me to think about another old idea: the relationship between risk and return. I’ve described a million times the way this was taught at the University of Chicago, beginning when I was there in the 1960s. It’s a graphical presentation we’ve all seen ever since, in which, as we move from left to right, increasing the expected risk, the expected return also increases (Figure 5):

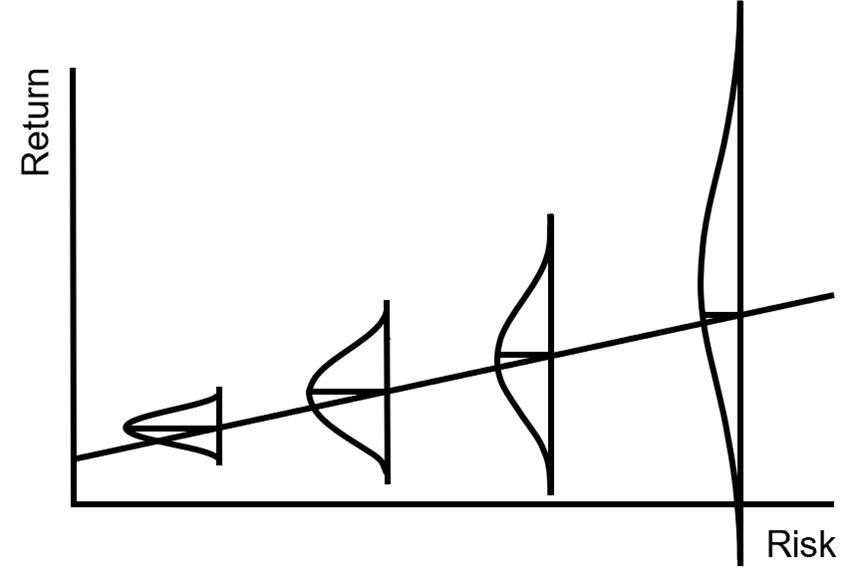

As readers know, I always felt this representation was highly inadequate, since the linearity of the relationship in the graph makes it appear too certain that increased risk will lead to increased return. This obviously belies the nature of risk. So, in a memo in 2006, I took the same line and superimposed on it some bell-shaped curves representing probability distributions turned on their side. I did this to indicate the uncertain nature of returns from riskier assets (Figure 6):

Now, we see that as the thing called “risk” increases (that is, as we move from left to right on the graph), not only does the expected return increase, but the range of possible outcomes becomes wider and the bad outcomes become worse. That’s risk! (I hope this way of presenting risk will be considered a lasting contribution to the investment industry when I’m gone.)

Doodling one day, I took the black and green curves describing ownership asset returns and debt returns from Figure 4 and added some intermediate positions in blue and red to indicate various combinations of the two. Thus, the blue curve is 2/3 debt and 1/3 ownership, and the red is 1/3 debt and 2/3 ownership (Figure 7):

In Australia, as I was showing this diagram, it struck me that Figure 7 is just another way to represent the idea presented in Figure 6. Again, as we move from left to right (more ownership assets, less debt), the expected return increases and the expected risk increases (that is, just as in Figure 6, the range of possible outcomes grows wider and the left-hand tail stretches further into undesirable territory). This way of presenting the options might be more intuitively clear.

Someone who believes in “more risk, more return” as portrayed in Figure 5 should logically adopt a high-risk posture. But if they understand the real implications of increased risk, as suggested by Figures 6 and 7, then they might opt for something more moderate.

The Role of Alpha and Beta

All the foregoing assumes markets are efficient:

- As risk increases in an efficient market, expected return increases proportionally. Or maybe that’s better stated the other way around: as expected return increases, so does the accompanying risk (the uncertainty surrounding the outcome and the likelihood of a bad one). Thus, no position on the risk continuum (for example, in Figure 6) is “better” than any other. It’s all just a matter of where you want to come out in terms of absolute riskiness, or what absolute level of return you want to aim for. The ratio of return to risk is similar at all points on the continuum – less of both toward the left, and more of both toward the right. Said another way, there’s no free lunch.

- Also, looking at each position on the risk continuum, the symmetricalness of the vertical distribution of possible returns around the expected return is similar from one position to the next. That means the ratio of upside potential to downside risk at one position on the continuum isn’t markedly better than it is at other positions – again no free lunch.

- Finally, if you want to move further out on the risk continuum, you can do so by either (a) investing in riskier assets or (b) applying leverage to the same assets (magnifying both the expected return and risk). Again, in a fully efficient market, neither tactic is preferable to the other.

The above three statements capture some of the important implications of supposed market efficiency.

Looked at this way, the only thing that matters is getting to the right risk position for you; under an assumption of market efficiency, there’s nothing to be gained in terms of return at a given level of risk. All ways of getting to a certain risk level will produce the same expected return.

The reason for this is the academic view that, in an efficient market, (a) all assets are priced fairly relative to each other, such that there are no bargains or over-pricings to take advantage of and (b) there’s no such thing as alpha, which I define as “gains resulting from superior individual skill.” As a result, there’s nothing to be gained from active decision making: no asset class, strategy, security or manager is “better” than any other. They merely vary in terms of risk and resulting return.

Also in the academic view, since there’s no such thing as alpha, the only thing that differentiates assets is their beta, or their relative volatility, the extent to which they reflect market movements. In the theory, it’s beta that expected returns are proportional to.

Now it’s time for me to assert strenuously that, in reality, markets are not efficient in the academic sense of always being “right.” Markets may do an efficient job of (a) rapidly incorporating new information and (b) accurately reflecting the resulting consensus opinion concerning the right price for each asset given the totality of information, but that opinion can be far from correct. For that reason, gains can be achieved by choosing skillfully among the options:

- some assets, markets or strategies can offer a better risk/return bargain than others, and

- some managers can operate within a market or strategy to produce superior risk-adjusted returns.

This last idea raises one of the key questions in asset allocation: should you consider departing from your “sweet spot” in terms of risk level in order to invest in a riskier asset class with a manager believed to possess alpha? There’s no easy answer to this question, especially given that many managers who are believed to possess alpha turn out not to.

To conclude, I’ll recap the key points:

- Fundamentally speaking, the only asset classes are ownership and debt.

- They differ enormously in terms of their fundamental nature.

- Ownership assets and debt assets should be combined to get your portfolio to the position on the risk/return continuum that’s right for you. This is the most important decision in portfolio management or asset allocation.

- The other decisions are merely a matter of implementation.

- Of course, your asset allocation process will be informed by how you rate your ability to identify and access superior strategies and superior managers, recognizing that doing so isn’t easy.

*****

Moving on to the real world, I want to make some important observations regarding one of Oaktree’s key sectors, non-investment grade credit (defined as performing non-government debt):

- The prospective returns in this area today are much higher than they were in the 2009-21 period.

- These returns, starting at roughly 7% on public credit and 10% on private credit, are competitive with the historical returns on equities and capable of helping many investors toward their overall return targets.

- Because of their contractual nature, the returns from credit are likely to prove much more dependable than ownership returns.

In my view, the thought process set forth in this memo leads to the conclusion that investors should increase their allocations in this area if they are (a) attracted by returns of 7-10% or so, (b) desirous of limiting uncertainty and volatility, and (c) willing to forgo upside potential beyond today’s yields to do so. For me, that should include a lot of investors, even if not everyone.

My recommendation at this time is that investors do the research required to increase their allocation to credit, establish a “program” for doing so, and take a partial step to implement it. While today’s potential returns are attractive in the absolute, higher returns were available on credit a year or two ago, and we could see them again if markets come to be less ruled by optimism. I believe there will be such a time.

Thank you for indulging me in this foray into investment philosophy. I hope you’ve found it of value.

October 22, 2024

Legal Information and Disclosures

This memorandum expresses the views of the author as of the date indicated and such views are subject to change without notice. Oaktree has no duty or obligation to update the information contained herein. Further, Oaktree makes no representation, and it should not be assumed, that past investment performance is an indication of future results. Moreover, wherever there is the potential for profit there is also the possibility of loss.

This memorandum is being made available for educational purposes only and should not be used for any other purpose. The information contained herein does not constitute and should not be construed as an offering of advisory services or an offer to sell or solicitation to buy any securities or related financial instruments in any jurisdiction. Certain information contained herein concerning economic trends and performance is based on or derived from information provided by independent third-party sources. Oaktree Capital Management, L.P. (“Oaktree”) believes that the sources from which such information has been obtained are reliable; however, it cannot guarantee the accuracy of such information and has not independently verified the accuracy or completeness of such information or the assumptions on which such information is based.

This memorandum, including the information contained herein, may not be copied, reproduced, republished, or posted in whole or in part, in any form without the prior written consent of Oaktree.

© 2024 Oaktree Capital Management, L.P., Oaktree Capital