by John Taylor, Head—European Fixed Income; Director—Global Multi-Sector, Nicholas Sanders, CFA, Portfolio Manager—Global Multi-Sector, Tom Nicol, Investment Strategist—Emerging Market Fixed Income, AllianceBernstein

US investors often stick to US markets. But that could be a costly mistake—especially today.

Compared with US bonds, global bonds hedged to the US dollar have historically been less volatile and generated higher risk-adjusted returns. That’s not the only reason that a home bias may present significant opportunity costs: hedged global bonds also have demonstrated better defensive characteristics than US bonds.

We saw this most recently in 2022—the worst year on record for bond markets. During that year, hedged global bonds outperformed US-only bonds due to the scale of the global bond market and the benefits of diversifying across globally disparate business and policy cycles.

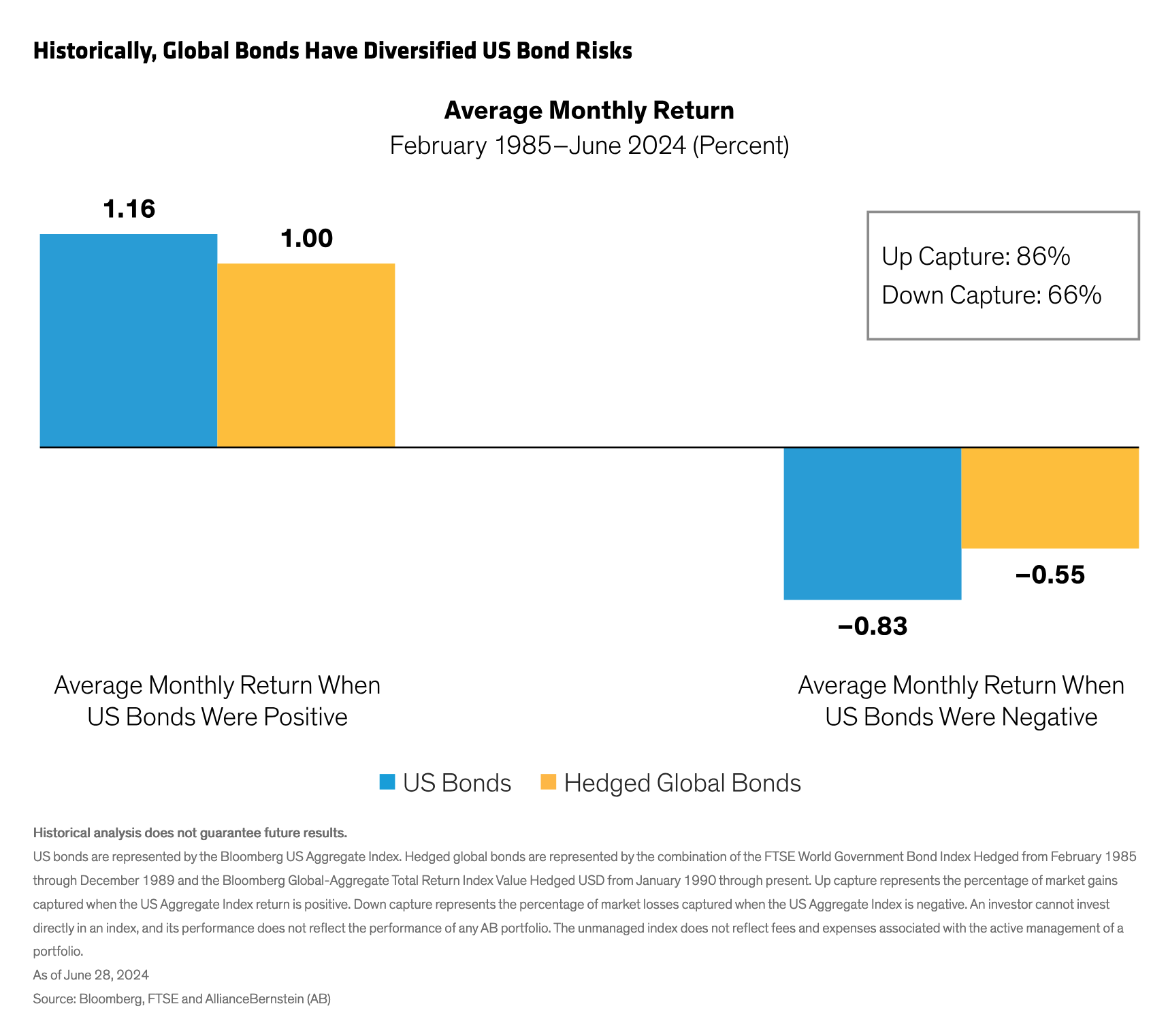

That hedged global bonds outperformed US bonds during a downturn is not surprising given hedged global bonds’ track record of providing attractive up/down capture ratios relative to US bonds (Display). In fact, over the past 40 years, hedged global bonds have captured 86% of gains when US bonds rallied. Conversely, when US bonds sold off, hedged global bonds experienced just 66% of that downturn.

We’re now facing a different environment than in 2022, when central banks began to aggressively hike rates to stem the inflationary tide. Global yields are coming off their highest levels in a decade, monetary and fiscal policies are diverging globally, and unique credit opportunities offer new sources of alpha. We think all these conditions favor global fixed-income exposure.

Global Yields Are at 10-Year Highs—for Now

After years languishing at historically low—and even negative—levels, bond yields have climbed to heights not seen in more than a decade. The yield on the 10-year Treasury bond alone is more than eight times what it was four years ago, and global bond yields have followed suit.

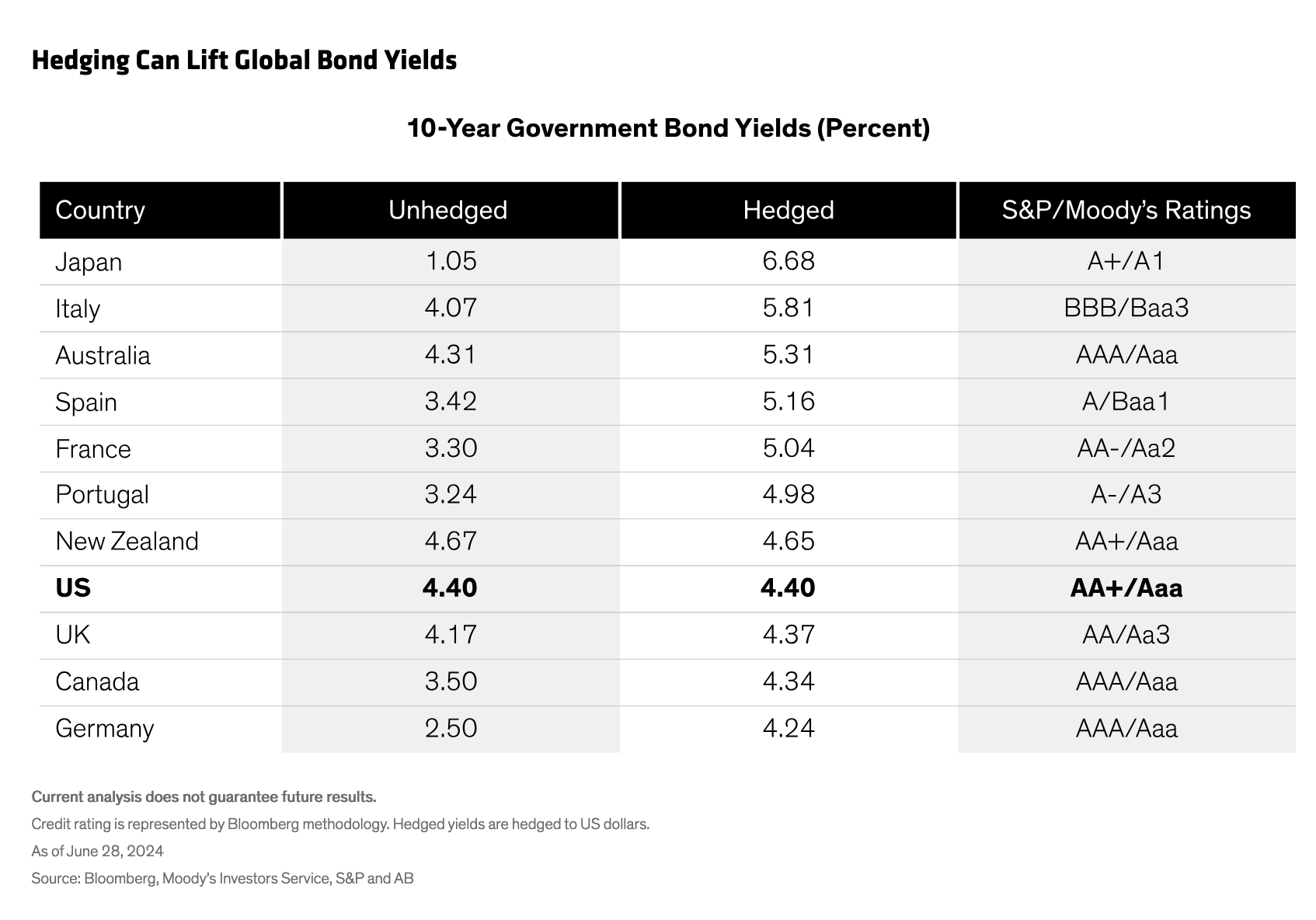

In today’s market, a global approach to bond investing may boost yields even further, provided holdings denominated in foreign currencies are hedged back to the US dollar. This is done using currency forwards and futures that eliminate foreign-exchange volatility. Given interest-rate differentials between other markets and the US, hedging may also result in higher yields, as it does today. On a hedged basis, nearly all non-US developed-market government bonds provide higher yields today than the 10-year Treasury bond (Display). A good example can be seen in Japan, where hedging boosts the low-yielding Japanese 10-year government bond yield from a mere 1.05% to 6.68%.

Over time, higher yields resulting from currency hedging have the potential to meaningfully affect a bond portfolio’s return.

Diverging Monetary and Fiscal Policies Point to Diversification

But global yields may not be at these levels for long. Already, some developed-market central banks have begun to cut interest rates. The Swiss National Bank has pared rates twice this year, while the Bank of Canada and the European Central Bank have also begun the process of monetary easing.

Policymakers in other countries have taken a more cautious stance. The Federal Reserve could take action on interest rates in the third quarter, while the Bank of England is expected make its first cut in September. Nor are the world’s central banks all moving in the same direction. The Bank of Japan hiked rates in March for the first time in 17 years, and Chinese policymakers have been cutting rates for several years already. This divergence reflects different inflationary trends and policy aims and offers fixed-income investors an added source of diversification.

Fiscal policy, too, is tacking in different directions. With roughly half of the world heading to the polls this year, election cycles could hasten stimulative fiscal policies in some cases. But the pace of spending will likely differ by region. In the US, fiscal spending has yet to pull back in response to inflationary pressures, while eurozone countries are generally exercising more fiscal discipline. The fiscal picture is a decidedly mixed bag across emerging markets.

These trends underscore ongoing policy desynchronization, which has important investment implications. In any market, investors can realize diversification benefits from investing globally, but that benefit may be even more powerful when the world’s central banks forge their own paths. And when yields come down, bond prices rise—although in our view that will happen in overseas markets sooner than it will in the US.

Today’s global fixed-income markets also provide opportunities to add alpha from security selection. By itself, the broad-based Bloomberg US Aggregate Index allows for alpha because of the varied sectors within it—all subject to different kinds of market risk. But when you add to the mix globally divergent market cycles across multiple sectors, those opportunities become even greater, in our view. Currently, we view European corporate debt as particularly compelling, and we also see select emerging-market corporates as well positioned.

Currency Hedging Is Key

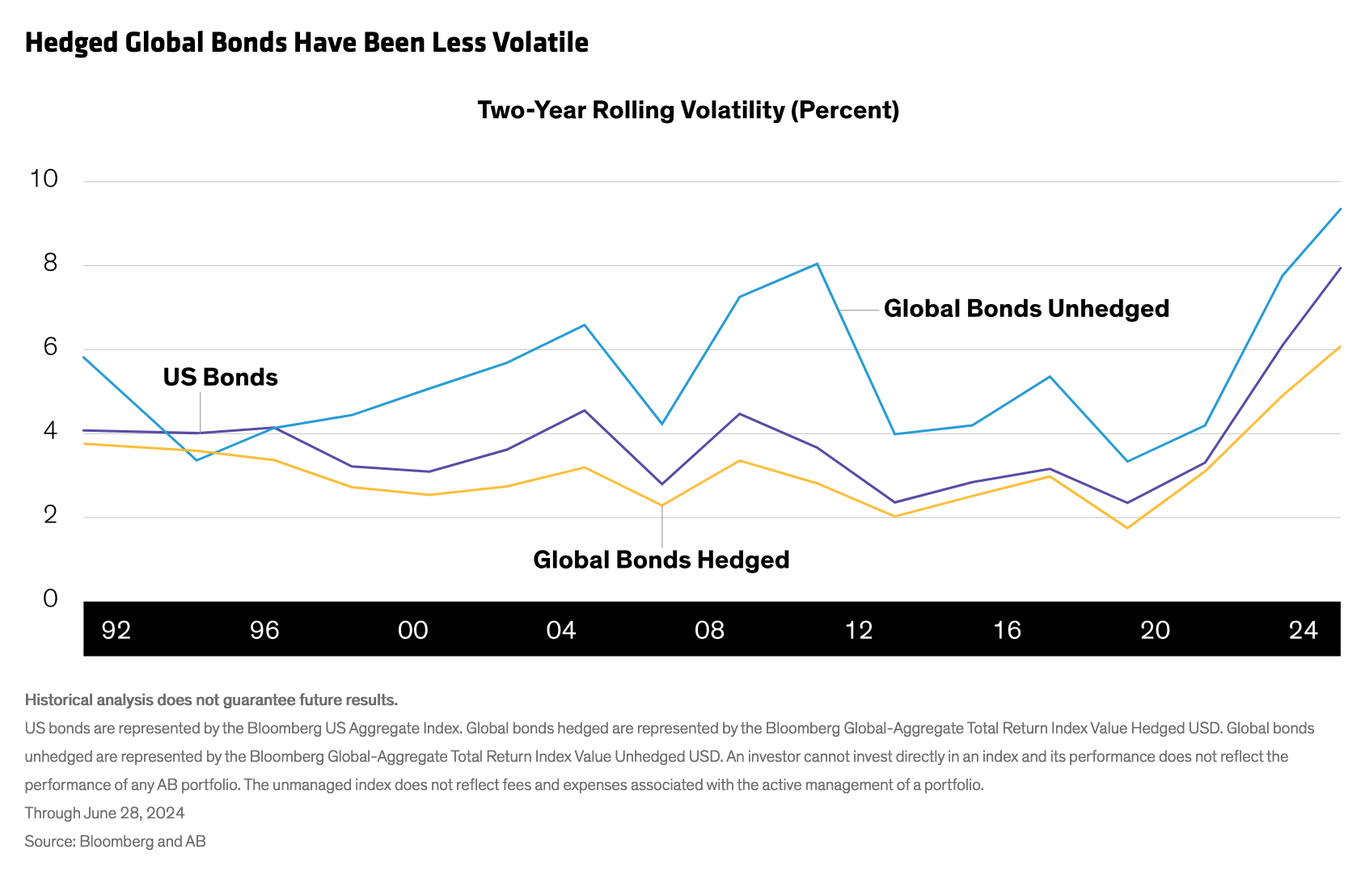

Despite opportunities available globally, fixed-income investors may be wary of foreign currency volatility, which can lead to a home bias. That’s why we believe core-bond investors should fully hedge their non-US holdings into US dollars. Careful hedging strategies can eliminate currency volatility (Display), thus preserving bonds’ role as ballast against equity market volatility—a primary core-bond mandate.

We think the time is right for core-bond investors to move beyond their home biases. Hedged global bonds have historically outperformed US bonds, and with less volatility. By hedging non-US holdings back into US dollars, fixed-income investors can realize the many benefits of global diversification without assuming undue levels of risk.

Copyright © AllianceBernstein