by Russ Koesterich, CFA, JD, Portfolio Manager, BlackRock

In this article, Russ Koesterich discusses why stocks are proving to be resilient in the face of higher rates and muted expectations for monetary easing.

Key takeaways

- Russ discusses why he thinks markets can move higher, with growth stocks remaining in the lead.

- While investors will always prefer lower to higher rates, stocks can survive modestly higher rates if accompanies by stronger growth.

Year-to-date stocks are proving resilient in the face of higher interest rates and more muted expectations for monetary easing. Back in February I suggested several factors that would support stocks, despite higher rates. Today, I still believe the market can move higher, with the additional qualifier that growth stocks, which suffered disproportionately in 2022, can continue to lead. The differences between today and two years ago include a smaller rise in rates and a more benign economic outlook.

A difference in magnitude

Two years ago, growth stocks were one of the hardest hit investment styles. Growth stocks are defined as companies that are growing their share prices, revenue, profits or cash flow at faster rates than the market at large. This made sense as growth, particularly ‘early’ growth companies, are distinguished by more distant cash flows, that in turn are penalized more by higher interest rates.

In 2022 the Russell 1000 Growth Index fell roughly 30% versus returns of -20% and -10% for the S&P 500 and Russell 1000 Value Index respectively. Thankfully, this year is proving different. The Russell 1000 growth is up nearly 11%, beating the market, as measured by the S&P 500, by roughly 3% and value, as measured by the Russell 1000 Value Index, by approximately 6%. What accounts for the difference?

To start, this year’s backup in rates is much more contained. Back in 2022 10-year yields surged, going from approximately 1.5% at the start of the year to an October peak of around 4.5%. Interestingly, the increase was not driven by higher inflation expectations, which had already surged in 2021. Instead the driver was mostly a shift in real or inflation-adjusted interest rates. Using the U.S. TIPS market, real 10-year yields started 2022 in negative territory, at approximately -1%. By the end of the year, they were over 1.5%.

This year’s backup in rates has, thus far, been more muted. 10-year yields are up 50-60 bps from where they started the year, with a similar move in real yields. This leaves rates about where they were last Thanksgiving.

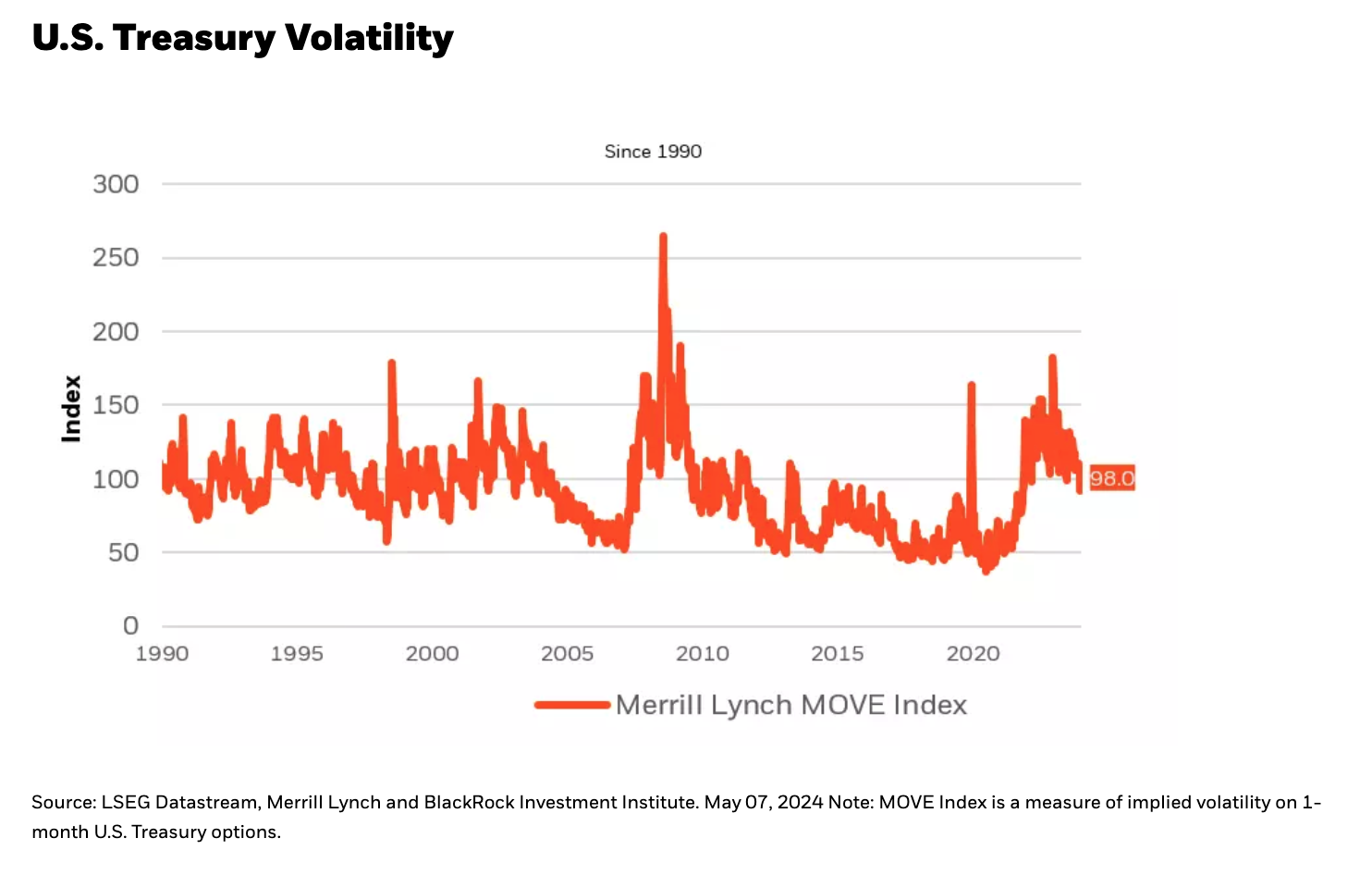

Another difference: 2022’s rate surge was much more volatile. From the fall of 2021 to the fall of 2022, the MOVE Index, which tracks index options tied to rates, surged more than 200%. This year’s backup in rates has proved more orderly. Rate vol peaked in 2023 and is modestly lower year-to-date (see Chart 1).

Economic resilience leading to market resilience

The other big difference between 2022 and today is a more benign economic backdrop. When tech companies were getting punished in 2022, investors were increasingly discounting a Federal Reserve (Fed) induced recession. Today, the Fed is poised to cut interest rates, albeit later than investors had hoped, and estimates of economic growth are rising. According to Bloomberg, economic estimates for 2024 economic growth, as measured by real growth domestic product (GDP), have risen from 1.3% in January to 2.4% today.

While investors will always prefer lower to higher rates, stocks can survive modestly higher rates if accompanied by stronger growth. Furthermore, large-cap growth-oriented companies have some of the strongest balance sheets and are most levered to many of the secular trends, i.e., artificial intelligence (AI), that are supporting a resilient economy. We believe they can continue to lead. In this environment, we would advocate for a continued overweight to segments of the market tied to secular growth themes, particularly companies tied to the advancement of AI across the market.

Copyright © BlackRock