by Kristina Hooper, Chief Global Market Strategist, Invesco

Key takeaways

- A confusing 1Q - Market swings punctuated the first quarter as “central bank speak” proliferated and caused confusion.

- Gaining perspective - I put first-quarter global markets into perspective and highlight some “little victories” that may have been easy to overlook.

- US disinflation - The core Personal Consumption Expenditures Price Index for March came as a relief — and got a vote of confidence from Federal Reserve Chair Jay Powell.

First-quarter market roundup

Equities. The first quarter was a strong one for equities around the world, with few exceptions.1 Japanese equities were the standout performer, posting double-digit gains. This was followed by the US, with the S&P 500 also gaining more than 10%. European equities also posted solid gains, with UK equity gains more tepid. Emerging market equities also experienced small gains while Chinese equities in particular lost modest ground in the first quarter, adding to oversold conditions. \

Fixed income. Fixed income2 generally disappointed for the quarter (with the exception of emerging markets bonds). However, global bonds saw better performance for the month of March. The volatility in fixed income was not surprising given some of the large swings experienced by the 10-year US Treasury yield, moving below 4% and above 4.3% over the course of the quarter.3

Alternatives. Alternative asset classes were mixed for the quarter.4 Global real estate investment trusts weakened for the quarter, although they had a strong month for March. Commodities, especially energy, had a strong quarter. Industrial metals were relatively flat for the quarter but experienced a significant gain in March. Gold rose during the quarter, as did bitcoin. Major currencies were weaker versus the dollar.

Markets anticipate the start of rate cuts

As mentioned at the outset, we saw market swings along the way, as central bank speak caused confusion. So what happened? In short, this was overall a “risk on” quarter as markets largely overlooked disappointing data and hawkish talk from central bankers, despite some initial negative reactions. Markets are discounting what they anticipate will happen this year – that disinflation in Western developed economies will continue and that their central banks will start cutting rates. Markets are also discounting a soft and brief slowdown for the global economy, followed by a re-acceleration. That’s why I believe we have seen a broadening of markets in recent weeks.

Little victories to start the second quarter

The first quarter of 2024 ended with some small victories:

- The US is still on the “D train” as disinflation continued in March. There were concerns about the US inflation path after some disappointing inflation data recently, so the core Personal Consumption Expenditures (PCE) Price Index for March came as a relief. Core PCE was 2.8% year-over-year, down slightly from 2.9% in February.5 This data received a vote of confidence from US Federal Reserve Chair Jay Powell, who said it was “more along the lines of what we want to see.” He continued, “It’s good to see something coming in line with expectations.”6 Powell also said he still expected “inflation to come down on a sometimes bumpy path to 2 percent.”7

- The UK and eurozone see more progress on inflation. Eurozone inflation has also continued to fall and is now within striking distance of the European Central Bank’s 2% target. UK inflation has made even more progress lately — its most recent reading was 3.4% year-over-year for February, its lowest level since 2021 and below expectations.8

- Inflation expectations are becoming better anchored. As I’ve said, inflation expectations – especially consumer inflation expectations – are important considerations for central banks. And so it was comforting to see the final University of Michigan Survey of Consumers for March. With five-year ahead inflation expectations down to 2.8% and one-year ahead inflation expectations moved down to 2.9%, I think it’s accurate to say that inflation expectations are “well anchored” – an important litmus test for the Fed.9 It is a similar story in the UK, where a recent Bank of England survey showed median inflation expectations for the year ahead at 3%, down from 3.3% in the previous survey. Longer-term consumer inflation expectations fell to 3.1%, getting closer to the Bank of England’s target.10 This was supported by the Citi/Yougov survey, which also showed a drop in consumer inflation expectations for both the short and longer terms.11

All this suggests that rate cuts could begin for some of the major Western developed central banks by the end of the second quarter.

The little victories have continued into the start of the second quarter:

- A positive economic surprise for China. We’ve seen a strong market reaction to China’s Caixin Manufacturing Purchasing Managers’ Index (PMI) data released yesterday, which was better than expected. As I’ve said before, I believe Chinese stocks were oversold so any positive surprise could prove to be a strong catalyst to move stocks higher.

- US manufacturing data is better than expected. US ISM Manufacturing PMI surprised to the upside, moving into expansion territory for the first time since September 2022. The new orders sub-index was particularly strong, which bodes well for the future.

Now it hasn’t been all sunny:

- The ISM manufacturing PMI data for the US was actually greeted negatively by markets. It is true that the price sub-index also moved higher, but this seems to be largely driven by commodity prices which can be very volatile. And the employment sub-index, while having risen, remains tepid. Nothing in this report changes my view about when the Fed will begin to cut.

- The Bank of Japan (BOJ) Tankan report on Japan’s economy was mixed – one area of disappointment was a drop in corporate sentiment. This has purportedly caused some profit taking, but that’s to be expected after such strong equity performance in the first quarter. And, perhaps more importantly, the survey showed that companies expect inflation to remain above the BOJ’s 2% target for the next five years.12 There is clearly confidence in the BOJ and the Japanese economy.

Looking ahead

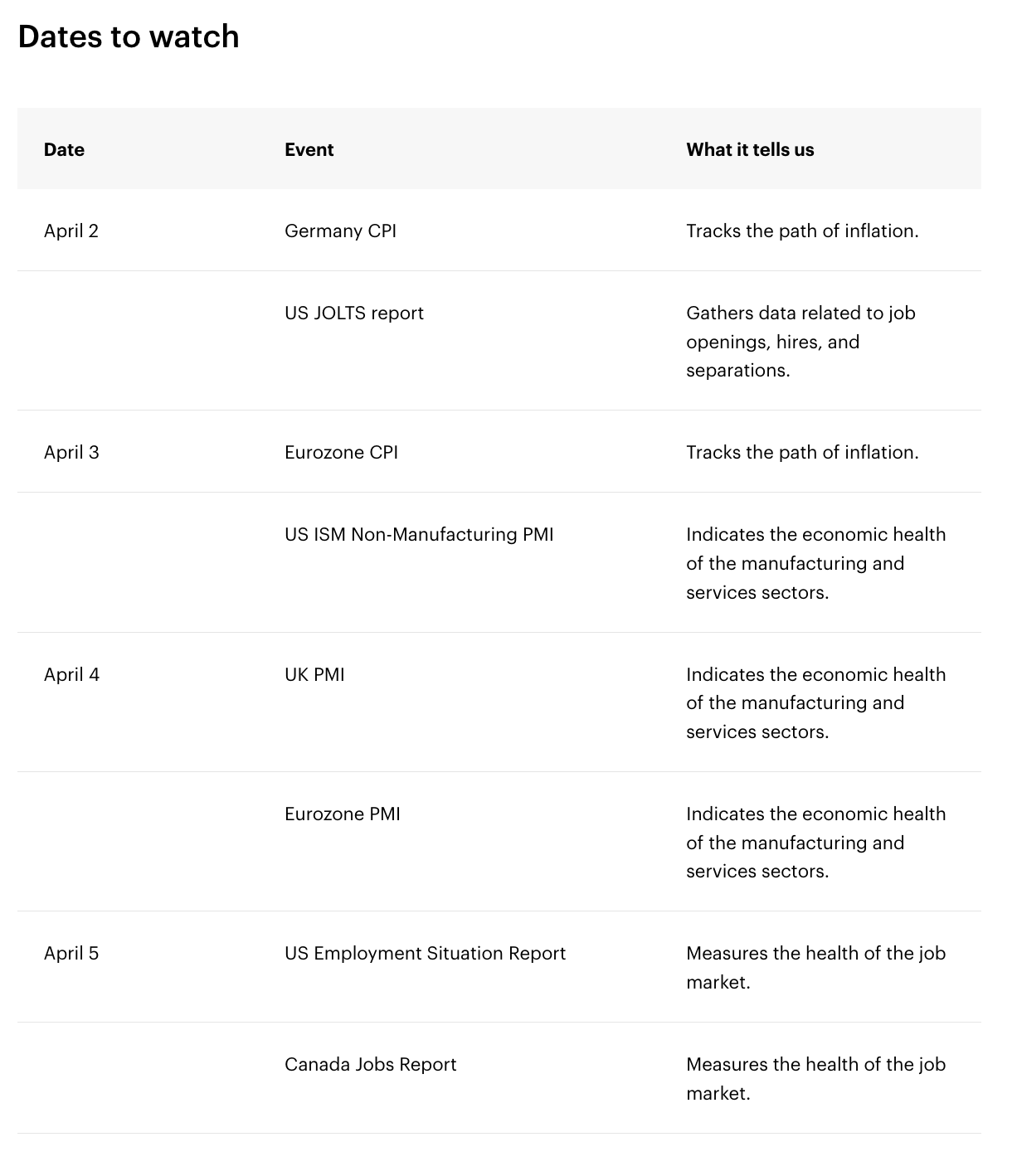

The US jobs report will of course be important this week. I’ll be laser-focused on average hourly earnings because I don’t think the Fed will care if non-farm payrolls are higher than expected; the Fed’s focus is going to be on wage growth because of its direct impact on inflation. Also important this week will be eurozone Consumer Price Index (CPI), and also the Job Openings and Labor Turnover Survey (JOLTS report) to get a sense of whether the US labour market is continuing to ease (it’s not necessary for the Fed to begin rate cuts, but it would be helpful to see a reduction in job openings).

Also important this week will be the minutes from the most recent European Central Bank meeting. I will be combing through this account for greater confirmation on when rate cuts may start (the current expectation is for June) and for more illumination on the expected pace of rate cuts.

Footnotes

1 Equity market performance sourced from Bloomberg and MSCI, referencing the MSCI Japan Index, MSCI Europe ex-UK Index, MSCI UK Index, MSCI Emerging Markets Index, MSCI China Index, and S&P 500 Index from Jan. 1, 2024, through March 31, 2024.

2 Fixed income market performance sourced from Refinitiv Datastream, referencing the Bank of America Merrill Lynch Global Bond Index, Bloomberg US Aggregate Bond Index, Bloomberg Global Aggregate Credit Index, and Bloomberg Emerging Markets Bond Index from Jan. 1, 2024, through March 31, 2024.

3 Source: Bloomberg, as of March 29, 2024

4 Alternatives market performance sourced from Refinitiv Datastream, referencing the FTSE Global REIT Index, S&P GSCI Commodity Index, S&P GSCI Energy Index, S&P GSCI Industrial Metals Index, S&P GSCI Precious Metals Index, and S&P GSCI Agricultural Goods Index.

5 Source: US Bureau of Economic Analysis, as of March 29, 2024

6 Source: Reuters, “New US inflation data 'along the lines' of what Fed wants, Powell says,” March 29, 2024

7 Source: PBS NewsHour, “Powell says the Federal Reserve wants to see ‘more good inflation readings’ before it can cut rates,” March 29, 2024

8 Source: UK Office for National Statistics, March 20, 2024

9 Source: University of Michigan Survey of Consumers, March 29, 2024

10 Source: Bank of England/Ipsos Attitudes Survey, March 15, 2024

11 Source: Citi/Yougov Survey, March 28, 2024

12 Source: Tankan Survey, April 1, 2024

Copyright © Invesco