by Jeffrey Kleintop, CFA® Managing Director, Chief Global Investment Strategist, Charles Schwab & Co., Inc.

Changes in China's economic policy tend not be communicated prior to implementation. What can we expect from China's stock market in response to any shifts?

One of the big challenges for investors is policy changes, which tended to have a big impact on China's economy in recent years. Policies including zero-COVID rules, the crackdown on big tech companies, and restrictions on leverage at property developers have seemed to come with no warning and little clarity. Much of the recent pressure on China's stock market began in 2020, concurrent with a new government policy restriction on the property market to crackdown on the buildup of leverage in the industry and curb housing speculation. The result starved developers of capital.

Recent measures to revive the Chinese economy have been a slow drip of policies, that have been ineffective and seen by markets as reactive, uncoordinated, and targeted rather than prompt and broad. They have not been sufficient to support a sustainable turnaround in consumer confidence, which remains low due to weakness in their biggest asset: property.

China's consumer confidence remains pinned to lows

Source: Charles Schwab, Bloomberg data as of 3/21/2024.

China's stocks valuation at low end of range

Source: Charles Schwab, MSCI, FactSet data as of 3/21/2024.

The price–earnings ratio, also known as P/E ratio, is the ratio of a company's share price to the company's earnings per share and is a measure of valuation. NTM indicates earnings expectations over the next 12 months.

- A government guarantee of homebuyer deposits at troubled property developers could help boost economic growth by turning around consumer confidence from its recession-like lows. Homeowners who put down big deposits with developers to build a home are now worried about not receiving their home or not getting their money back from failing developers, which seems to have prompted them to pull back on their spending. Pent-up savings in China continue to grow and could be unleashed to the benefit of China's economy and businesses (particularly the banks and real estate companies) and to global consumer product makers with exposure to China, particularly European luxury goods producers.

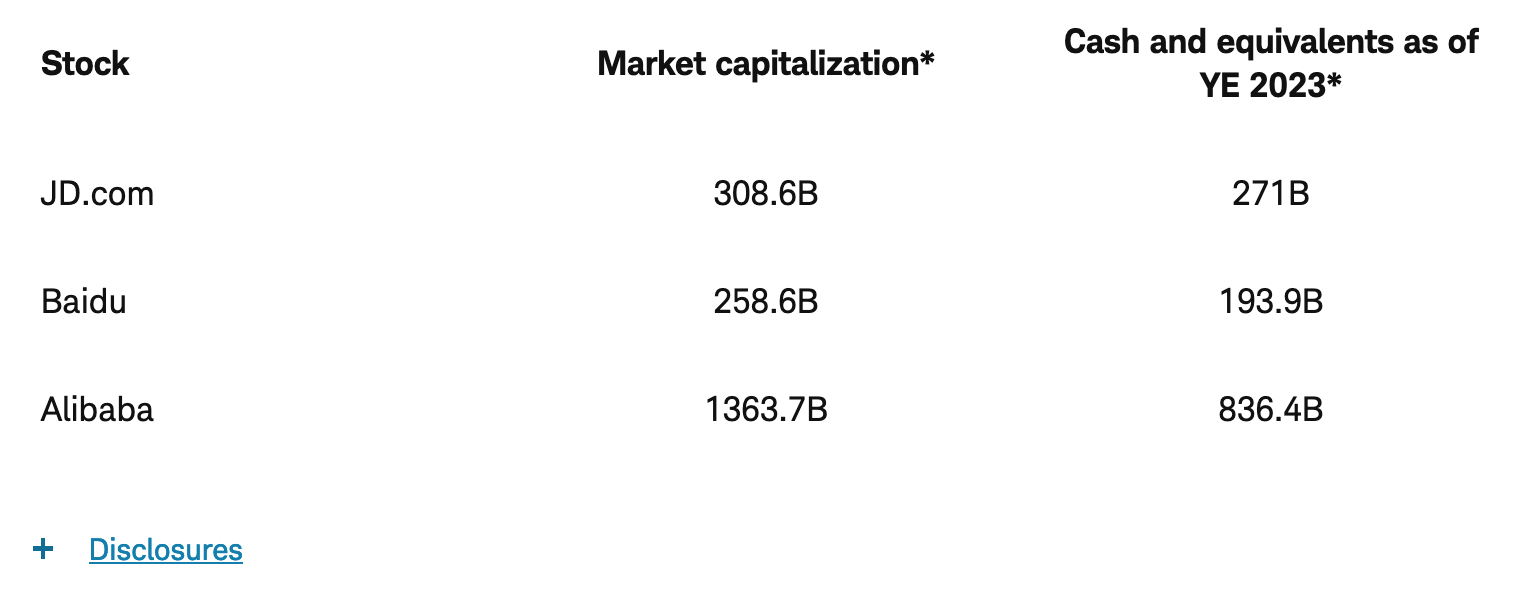

- Loosening capital controls could help boost stocks by easing the ability of cash rich companies to do share buybacks. China's strict rules regarding moving money in or out of the country make share buybacks challenging since most of the earnings of these companies are generated in mainland China, but the shares are listed in New York or Hong Kong. The stock market values of some giant Chinese companies, including those such as Alibaba, Baidu, and JD.com, are approaching the amounts of cash and equivalents on their balance sheets despite these being profitable and growing companies. That may be due to the perception that the Chinese government could announce a policy change at any time, imposing costly new fines, taxes, or regulations. Loosening capital controls could boost confidence by shareholders in the cash stockpiles held by many Chinese companies being distributed to them rather than risk being plundered by policy changes.

- Measures to reduce government regulations and encourage entrepreneurship could support business confidence. Years of abrupt policy changes with tough regulations imposed on educational tutoring, video game developers, businesses consultants, and mobile app creators, among others, may have left both established businesses and entrepreneurs in an unsupportive environment. The latest ruling from Beijing that requires all mobile app providers to submit their business details to the government is one example of policies that may stifle innovation. Reversing some of these regulations could be seen as fostering a more innovative environment. This effect was seen in the performance of video game developers in late December when a regulatory proposal was rescinded that would have required them to implement measures to cap user spending in games and ban "excessive" rewards. The original response to the proposal caused a plunge in China's gaming stocks. China's regulators have followed up by approving more new game titles each month since the shift in policy. NetEase, one of China's biggest gaming companies, rebounded 40% from its lows following the policy change.

There are no signs of any major imminent shift in policy in China. But it is worth keeping in mind that China's policymakers rarely signal such changes in advance. Any surprises could potentially trigger sharp rebounds in China's stock market, like in late 2022 when the zero-COVID restrictions were suddenly dropped. China's stocks shot up 60% over the subsequent three-month period.

China's stocks soared 60% following surprise end to zero-COVID policies

Source: Charles Schwab, Bloomberg data from 9/1/2022 through 3/31/2023 as of 3/23/2024.

Past performance is no guarantee of future results. Indexes are unmanaged, do not incur management fees, costs and expenses and cannot be invested in directly.

Copyright © Charles Schwab & Co., Inc.