by Thorsten Winkelmann, Chief Investment Officer—Europe and Global Growth, Marcus Morris-Eyton, Portfolio Manager—Europe and Global Growth, AllianceBernstein

Attractive growth companies are scattered across Europe’s otherwise lackluster market landscape. Here’s how to find them.

Europe is often seen as an inferior source of growth to US markets. Yet by deploying a coherent bottom-up process, equity investors can find high-quality stocks across Europe, backed by businesses with powerful and underappreciated long-term growth potential.

Europe’s stock markets have been overshadowed by the US for years. When the MSCI Europe Index advanced 15.8% in euro terms in 2023, the S&P 500 surged by 26.3% in US-dollar terms. The index performance gap reflected sluggish earnings growth in Europe, at a time when US markets have been turbocharged by a small group of mega-cap stocks seen as big beneficiaries from artificial intelligence.

The economic backdrop didn’t make it easier. Europe has been hampered by relatively slower GDP growth, and regional equity markets have a heavier contingent of cyclically sensitive stocks than the US. So why should investors focus on Europe as a distinct equity allocation or within a global portfolio?

For Some Industries and Businesses, the Economy Doesn’t Matter Much

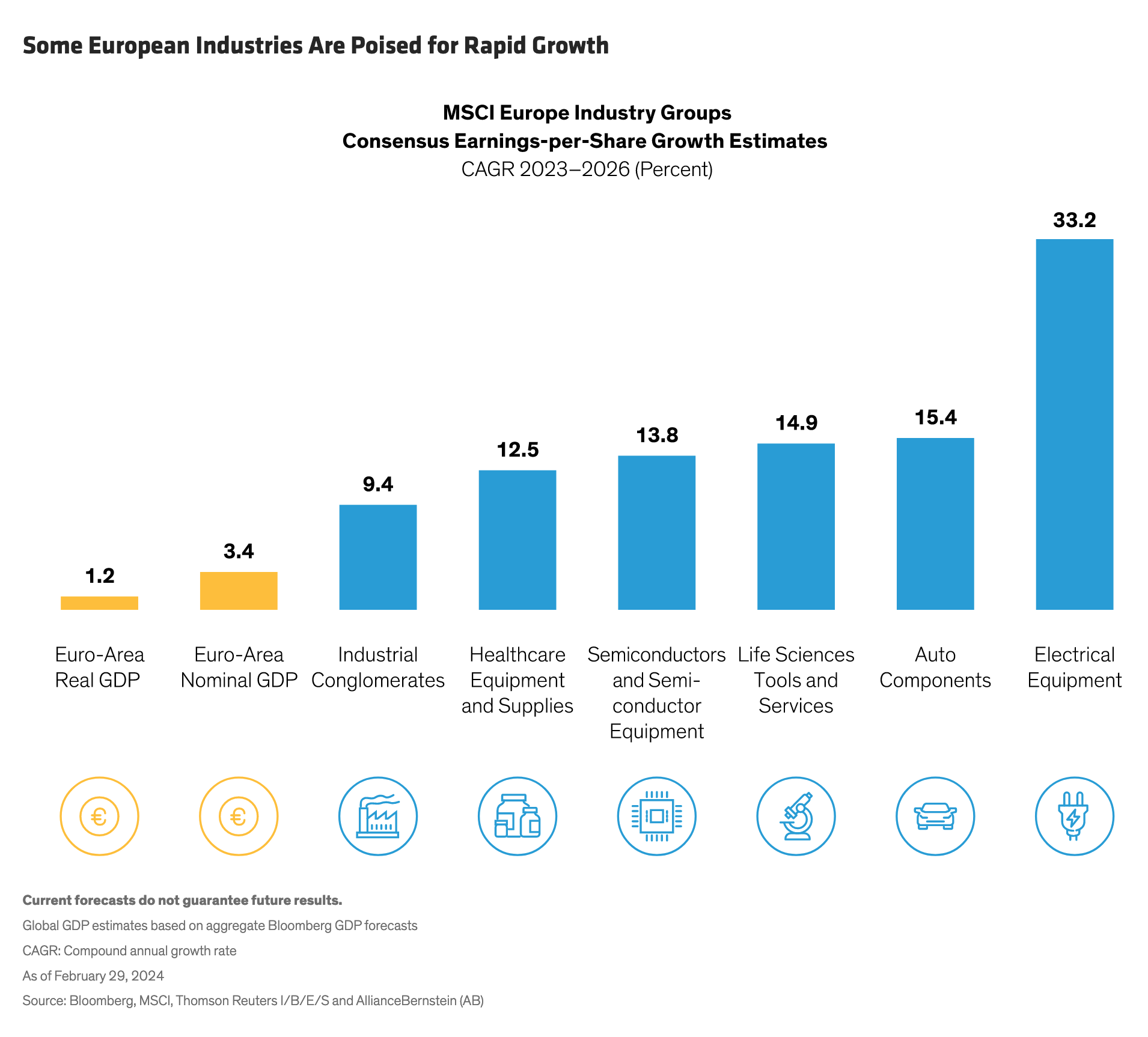

Europe, in fact, offers attractive pockets of growth for investors who know how to find them. Several European industries—including industrials, semiconductors and electrical equipment—are forecast to deliver robust earnings growth through 2026, according to consensus estimates (Display). These industries are poised to expand well above the region’s meager GDP growth forecasts.

How are these industries enjoying such rapid growth in a tepid economy? Some are exposed to structural growth drivers that aren’t tied to macroeconomic growth, such as technological trends, healthcare innovation, industrial automation and the energy transition.

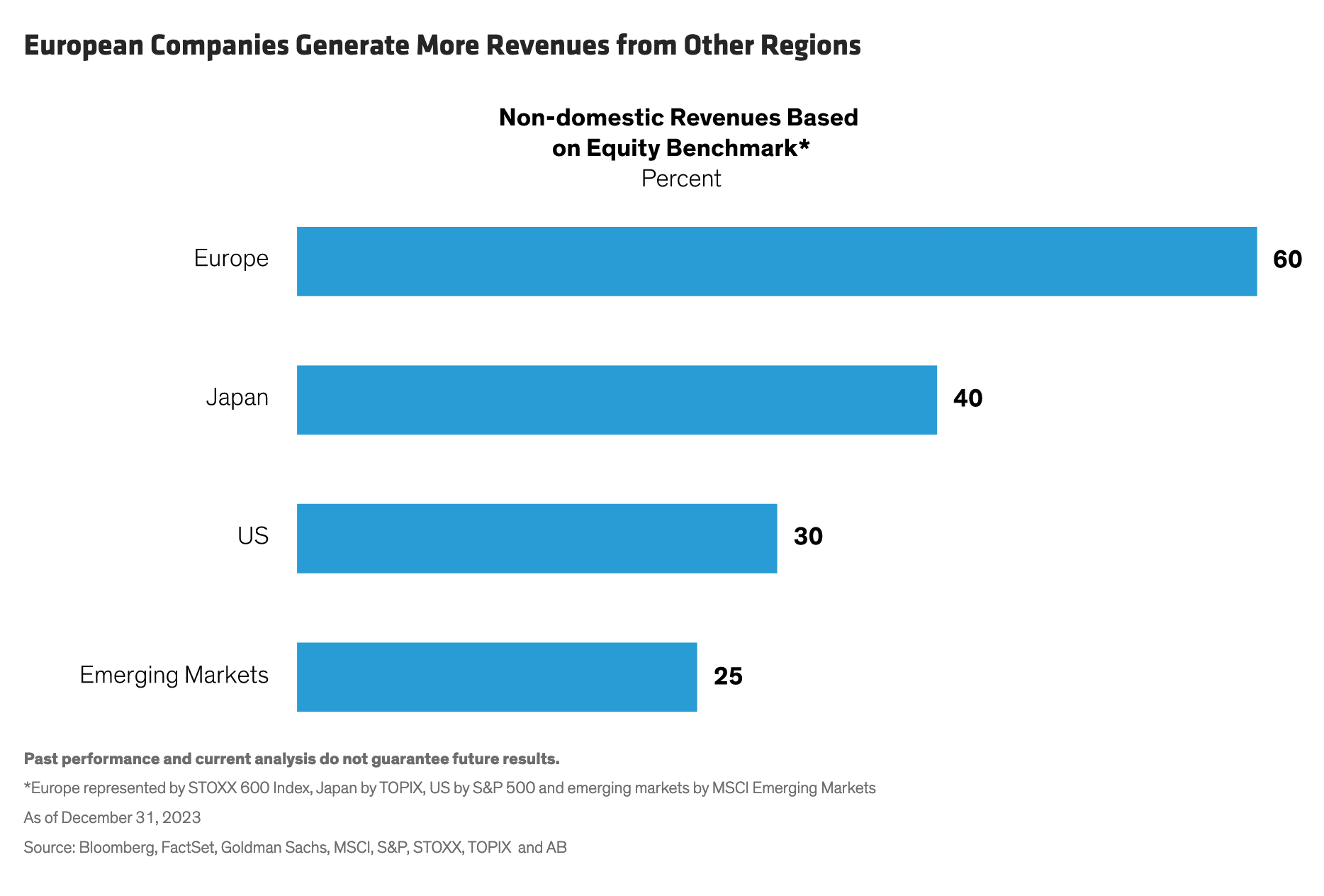

What’s more, many businesses in these industries are global, so they don’t rely on domestic European markets for sales. Companies in the MSCI Europe universe derived 60% of their revenues from outside the region in 2023—a much higher proportion of non-domestic sales than those of companies in the US, Japan or emerging markets (Display). As a result, their fortunes don’t really depend on Europe’s macroeconomic outlook.

Quality Businesses Make the Difference

However, identifying appealing industry dynamics isn’t enough for equity investors. To discover European companies with attractive long-term potential, we believe investors must look within structurally growing industries for high-quality businesses that can sustain consistent earnings growth over time. Select companies with the right attributes often offer investors higher, and equally important, more sustainable long-term growth rates than their broader industry groups. We believe these features augment the compounding power of holding these businesses for at least five years.

Businesses that have clear competitive advantages in industries with high barriers to entry are well positioned to maintain growth through good and bad times. Management skill and capital discipline are essential features for delivering growth through changing conditions. Strong fundamental metrics, such as return on equity and return on invested capital, point to business models with staying power and a good moat. Taken together, we believe these characteristics help bolster high cash flows that can fuel strong earnings growth over time—particularly within industries that have explicit structural growth drivers.

Semiconductors are a good example. Demand for increasingly sophisticated semiconductors comes from many directions, including the commercialization of AI, migration to the cloud and the massive growth of data centers. These trends are likely to persist through diverse macroeconomic conditions.

Manufacturing semiconductors requires highly specialized equipment, such as extreme ultraviolet lithography scanners, known as EUVs. Netherlands-based ASML, the only global manufacturer of EUVs, has developed the technology over 25 years with billions of dollars of research and development. Since EUVs have more than 100,000 parts, many of which are custom made, we believe the technology is hard for competitors to replicate, providing ASML with formidable competitive advantages in a market with multiple catalysts for growth.

Industrial Efficiencies: Unseen Sources of Tangible Growth

Industrial companies might not register on investors’ radars as high-growth businesses. Yet companies that help customers generate real efficiencies for their customers, through distinctive and innovative products, technologies or services command powerful sources of cash flows. These firms may not be household names, but their products often help machines, vehicles and buildings perform better and reduce costs.

Consider Spirax Sarco, a UK-based maker of steam-management products. The company offers more than 40,000 products used in an array of industries, from food production to pharmaceuticals, for critical manufacturing processes. Most of Spirax’s revenue comes from customers’ operating budgets, which are less vulnerable to cyclical swings in earnings than capital expenditure. Spirax’s direct sales model in key markets is differentiated from peers and integrates the company closely with its customers, in our view. Meanwhile, we believe the company’s steam and thermal solutions business is likely to enjoy structural demand from global efforts to decarbonize industrial processes.

Cut Through the European Cloud Cover

Quality companies in Europe might lack the star power of the US mega-caps. But that means investors can find European companies with impressive growth rates at relatively attractive valuations. In our view, buying durable growth at attractive share valuations adds to the compounding power of these businesses for equity investors with long time horizons. Select companies in Europe have generated highly competitive returns in a global perspective that transcend the regional market environment.

In investing as in life, stereotypes often lead to self-defeating biases. Europe’s broad equity markets may suffer from a regional malaise that has tainted investor sentiment and suppressed market returns, yet investors who cut through the cloud cover with clearly defined research objectives will find that select European companies with compelling long-term return potential are hidden in plain sight.

The MSCI data may not be further redistributed or used as a basis for other indices or any securities or financial products. This report is not approved, reviewed or produced by MSCI.

About the Authors

Thorsten Winkelmann

Thorsten Winkelmann

Thorsten Winkelmann is Chief Investment Officer of Europe and Global Growth. Prior to joining AB in 2024, he spent more than 20 years at Allianz Global Investors, where he was CIO of the Global Growth team and a portfolio manager for the Global Equity Growth and Europe Equity Growth strategies. Previously, he was a portfolio manager within the European Equity Core and Multi-Asset teams. Winkelmann holds an MA in economics from the University of Bonn. Location: Frankfurt

Marcus Morris-Eyton

Marcus Morris-Eyton

Marcus Morris-Eyton is a Portfolio Manager for Europe and Global Growth. Prior to joining AB in 2024, he was a portfolio manager at Allianz Global Investors, which he joined in 2011. Morris-Eyton also worked as a discretionary sales manager at Allianz Global Investors in London, and in equity research at Credit Suisse. He was named one of the Top 40 Under 40 Rising Stars in Asset Management by Financial News in 2015. Morris-Eyton holds a BA with first class honours in English and philosophy from the University of Leeds. He is a CFA charterholder. Location: London

Copyright © AllianceBernstein