by Kristina Hooper, Chief Global Market Strategist, Invesco

Key takeaways

Eyes on ChinaChina's National People's Congress convened this week and set a growth target of 5%. |

The “dot plot”There are rumors that the US Federal Reserve’s March dot plot will show expectations for an average of only two rate cuts in 2024. |

Bank of JapanBank of Japan (BOJ) officials have suggested the BOJ will be more patient in normalizing monetary policy. |

1. Disinflation is expected to continue

We are still on the “D” train. I’m confident that disinflationary progress will continue in March, albeit imperfectly. I was encouraged to see that the S&P Global flash US Purchasing Managers’ Index (PMI) output prices sub-index charged for goods and services clocked in at a relatively low 52.9 — the second-lowest reading since June 2020.1According to S&P Global, this reading is broadly indicative of consumer inflation running at a 2% level — which is, as we know, the US Federal Reserve’s (Fed) target.2

Recent data for the UK and eurozone indicate stickier inflation, but these economies are all moving in the right direction with regard to inflation. The flash estimate of euro area inflation for February was 2.6% year over year, down from 2.8% in January. The core rate, ex-food, energy, alcohol, and tobacco, was 3.1% for February, down from 3.3% in January.3

In the eurozone manufacturing PMI survey, both input costs and output charges continued to drop.4 One source of inflationary concern for much of the globe was the Houthi attacks on Red Sea shipping lanes, and even that appears to have subsided. Transpacific shipping rates fell 4.6% sequentially last week and are down 15% from their peak in early February.5

2. Japanese equities appear poised for continued strength

We’ve gotten recent messaging from Bank of Japan (BOJ) officials suggesting the BOJ will be more patient in normalizing monetary policy. While BOJ Board member Hajime Takata expressed the view that the BOJ must consider altering its ultra-loose monetary policy, including exiting negative interest rates and yield curve control, he later modified those comments suggesting he has not made up his mind about whether the BOJ should terminate negative rates in March.

More importantly, BOJ Governor Kazuo Ueda shared at last week’s G20 finance meeting, “We are not yet in a position to foresee the achievement of a sustainable and stable inflation target.”6 He said they would be looking to data going forward to confirm this. Most analysts expect the BOJ to end negative rates in April, although my read on this is that the BOJ is not date-dependent but data-dependent. That means they will be patient and thoughtful about tightening monetary policy. I believe this could be very supportive for Japanese equities.

3. What will China’s National People’s Congress do this week?

China’s National People’s Congress (NPC) convenes this week. This is an important annual meeting in which the government’s growth target is set for the year and high-level policy is often unveiled.

As we said in our 2024 outlook released late last year, policy stimulus will be an important factor in Chinese equity performance this year (and, of course, it will be important factor in economic growth as well). Thus far, I am encouraged. Last week, the Chinese Politburo released a statement indicating their intent to become more aggressive in stimulating the economy, noting that “proactive fiscal policy must be moderately strengthened and improved in quality and efficiency, while prudent monetary policy should be flexible, moderate, precise and effective.”7

At the State Council meeting on Jan. 22, we saw a pledge to stabilize capital markets and improve market confidence, which was followed up with a stream of targeted policy support, from rate cuts to tighter regulations on short-selling to funding support for residential property projects.8 That seems to have improved market confidence; from Feb. 5 through March 1, the Shanghai Composite Index has risen nearly 14%.9

At the NPC, China confirmed a 5% growth target for the year, and I expect to see them offer supportive policy for the economy and markets. I think that will further support China equities.

4. What will the Fed’s “dot plot” show?

The Fed meeting is happening later in March. While the Fed isn’t expected to hike rates, that doesn’t mean it won’t be an important meeting. The March meeting is one of four in which the Fed releases a new “dot plot” — a Summary of Economic Projections that includes expectations for where the fed funds rate will be at the end of 2024.

There are rumours (or perhaps just articulated fears) that the March dot plot will show expectations for an average of only two rate cuts in 2024. This would certainly dampen the current market enthusiasm we are seeing, which perhaps isn’t a bad thing given that it seems time for US stocks to take a breather, albeit briefly.

However, I can’t help but remind that in December 2021, the Fed issued a dot plot showing expectations that the average fed funds rate at the end of 2022 would be 90 basis points.10They were only slightly off (sarcasm intended) as the actual fed funds rate at the end of 2022 was 433 basis points.11

5. A glimmer of hope in the midst of hawkish “Fedspeak”

They say that March comes in like a lion and goes out like a lamb. Maybe that will be the case for the Fed. We’ve been getting a lot of hawkish “Fedspeak” lately, but we got a glimmer of hope the other day that I think foreshadows what’s to come.

Chicago Fed President Austan Goolsbee said he thinks the fed funds rate at this level is very restrictive, while Dallas Fed President Lorie Logan said she thinks it’s appropriate to ease the level of quantitative tightening. As I wrote last week, I think most Fed participants will continue to talk hawkishly — but I am optimistic they will positively surprise, and likely in May.

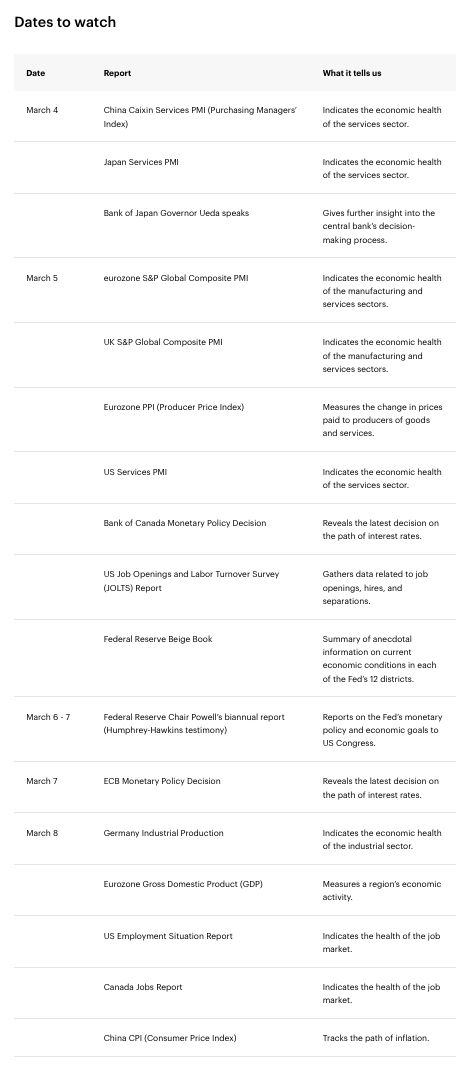

The week ahead

Since earnings season is practically over, I expect market movement to be driven even more by factors impacting monetary policy expectations — specifically data and central bank speak, as well as several central bank meetings next week. That means we’ll be paying close attention to all of that — especially US average hourly earnings in Friday’s jobs report — plus China’s NPC and the UK Budget.

We also can’t overlook two major central banks will be meeting this week: the Bank of Canada and the European Central Bank (ECB). While most will be focused on the ECB, I’ll be paying close attention to the Bank of Canada, which has often been at the vanguard of monetary policy decisions in recent years — and so we will want to pay close attention to what they are thinking and doing.

In memoriam

I couldn’t let this week’s column go by without a note to remember my friend and colleague Mark Giuliano, who passed away suddenly over the weekend. Mark was a great man who served his country in the FBI for 28 years before joining Invesco, where he was Chief Administrative Officer and part of our Executive Leadership Team. He was an important part of the Invesco family and an intelligent, thoughtful leader. He will be sorely missed. My condolences to his family, whom I know he was devoted to.

Footnotes

1 Source: S&P Global, Feb. 23, 2024

2 Source: US inflation descent outpacing that of Europe according to flash PMIs, S&P Global, Feb. 24, 2024

3 Source: Eurostat, March 1, 2024

4 Source: S&P Global/HCOB, March 1, 2024

5 Source: Bloomberg quoting Drewry, as of Feb. 28, 2024

6 Source: BOJ’s Ueda Keeps Market Players Guessing Over Rate Hike Timing, Bloomberg, Feb. 29, 2024

7 Source: ‘Two sessions’ 2024: China signals more fiscal pump-priming as economic doubts linger, South Morning Post, Feb. 29, 2024

8 Source: Xinhua, Jan. 22, 2024

9 Source: Bloomberg, as of March 1, 2024

10 Source: Board of Governors of the Federal Reserve System, as of Dec. 15, 2021

11 Source: Board of Governors of the Federal Reserve System, as of Dec. 31, 2022

Copyright © Invesco